Locator: 50915LNG.

SRE and Costa Azul: link here. Production has begun. Next: shipping LNG to Asia. This is Mexico's first west coast export termial, Ensenada in Mexicot's Baja California. Partnered with TotalEnergies SE and Japanese trading firm Mitsui & Co. LTD. Links everywhere. Followed frequently on the blog. This may be the best, link here.

*******************************

Back to the Bakken

EOR: Alex Kimani over at Oilprice, link here. North Dakota chases a second Bakken boom thorugh enhanced recovery.

WTI: $92.41.

New wells reporting:

- Sunday, June 7, 2026: 6 for the month, 162 for the quarter, 319 for the year,

- 42170, conf, Formentera Operations, Maverick 22-10-BND N618H,

- 42006, conf, Slawson, Cannonball Federal 4-27-34H,

- Saturday, June 6, 2026: 4 for the month, 160 for the quarter, 317 for the year,

- 42005, conf, Slawson, Sauger Federal 5-22UH,

- Friday, June 5, 2026: 3 for the month, 159 for the quarter, 316 for the year,

- 42004, conf, Slawson, Cannonball Federal 5-27-34H,

RBN Energy: Commonwealth, Delfin LG add to wave of US projects; are still more on the way? Link here. Archived.

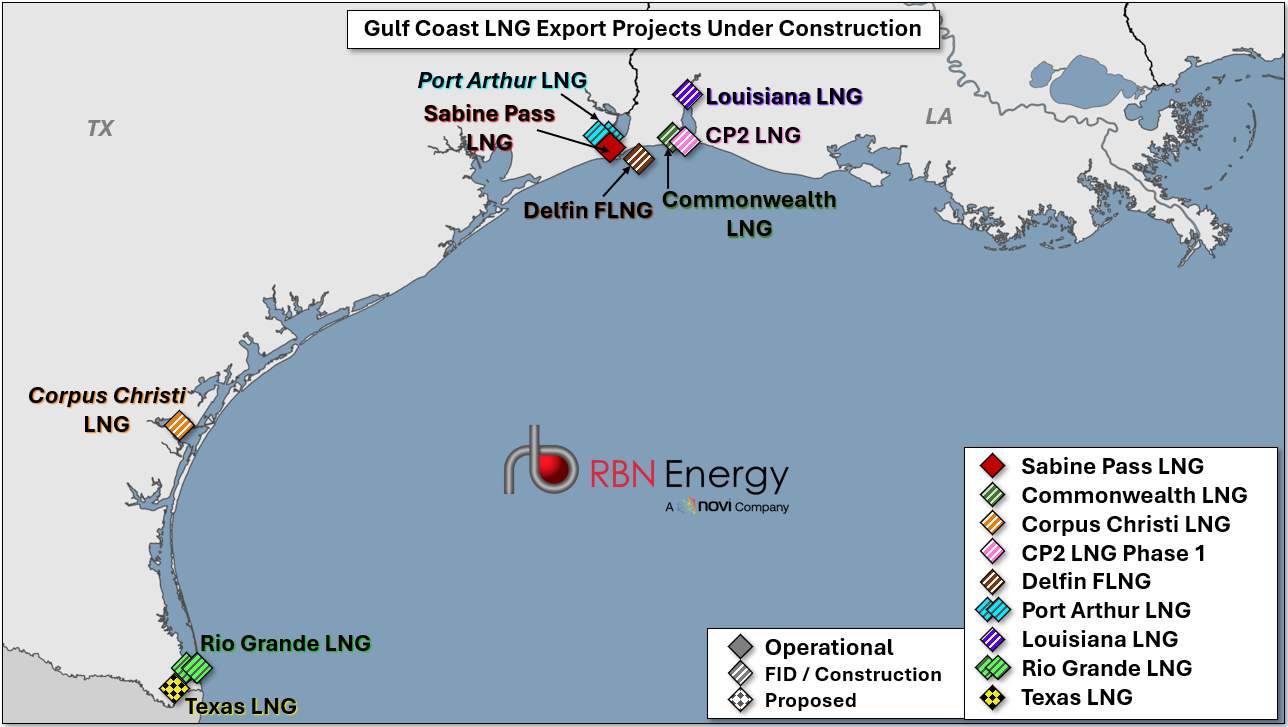

The U.S. is at the tail end of an incredible wave of LNG expansion that has so far seen nine new projects across seven terminals reach a final investment decision (FID) in a little over a year. The two latest projects, Commonwealth LNG and Delfin FLNG, had been approaching the developmental finish line for some time. Commonwealth’s greenlight should come as no surprise, while Delfin’s was somewhat more unexpected. But more important than the individual projects, the overall scale of the buildout coming in the back half of this decade and into early next decade is staggering. The U.S. can export around 16.1 Bcf/d of LNG today, with another 1.2 Bcf/d of capacity ramping online, but capacity will be around 33 Bcf/d by early next decade given the number of projects that have reached FID or are under construction. For reference, that’s less than 3 Bcf/d shy of total U.S. gas demand for power in 2025. In today’s RBN blog, we take a closer look at this incredible wave of investment, the Commonwealth LNG project and what comes next for U.S. LNG development.

This latest round of commitments to U.S. LNG started out with a surprise. In late April 2025, Australia’s Woodside Energy announced that it was moving forward with the 16.5 million tons per annum (MMtpa; 2.2 Bcf/d) Louisiana LNG (purple-and-white striped diamond in Figure 1 below) despite having almost no long-term sales for the project — seeI’m Back (Back in the LNG Groove). Woodside decided to stick with the method it had used to develop its Australian projects, where it sold ownership interest to de-risk its investment, rather than conform to the typical development approach of U.S. builders, which relies heavily on long-term sales to underpin a project. That was soon followed by a Cheniere Energy FID on a small Corpus Christi expansion project (orange-and-white striped diamond) in June and then Venture Global’s FID of CP2 Phase 1 (pink-and-white striped diamond) in July. Then, last fall, Sempra greenlit two additional trains at the under-construction Port Arthur LNG (aqua-and-gray striped diamonds), and NextDecade also added two trains (Train 4 in September and Train 5 in November) to Rio Grande LNG (bright-green-and-gray striped diamonds) in South Texas.

Figure 1. Gulf Coast LNG Export Projects Under Construction. Source: LNG Voyager