Gov. Doug Burgum is asking President Donald Trump for a major disaster declaration for North Dakota counties affected by severe drought conditions that now cover most of the state.

If approved, the declaration would activate the Individual Assistance Program and make direct federal assistance available to 33 counties and one tribal nation, including Williams, Divide, Mountrail, Divide, Dunn, McKenzie and Billings County.

Other counties on Burgum’s list include Adams, Bottineau, Billings, Bowman, Burke, Burleigh, Dickey, Emmons, Golden Valley, Grant, Hettinger, Kidder, Lamoure, Logan, Mchenry, McIntosh, McLean, Mercer, Morton, Oliver, Pierce, Renville, Sioux and the Standing Rock Sioux Nation, Slope, Stark, Stutsman, Ward, and Wells counties.

Wednesday, August 9, 2017

North Dakota Drought -- Governor Asks Federal Government To Declare Major Disaster -- August 9, 2017

From The Williston Herald:

Wishin' And Hopin' -- Theme Song For Mainstream Media -- August 9, 2017

In today's "fake news" department, "early season storms one indicator of an active hurricane season." Algore and mainstream media are wishin' and hopin' --

Wishin' and Hopin', Dusty Springfield

This is absolutely one of my favorite songs -- depending on the moment, it may be my favorite song -- I prefer other singers, but how appropriate to have this one show up randomly tonight. Funny how things happen.

If You Go Away, Glen Campbell

******************************

This is absolutely one of my favorite songs -- depending on the moment, it may be my favorite song -- I prefer other singers, but how appropriate to have this one show up randomly tonight. Funny how things happen.

One New Permit; Four DUCs Completed -- August 9, 2017

Active rigs:

One new permit:

| $49.61 | 8/9/2017 | 08/09/2016 | 08/09/2015 | 08/09/2014 | 08/09/2013 |

|---|---|---|---|---|---|

| Active Rigs | 57 | 33 | 73 | 193 | 183 |

One new permit:

- Operator: Abraxas

- Field: North Fork (McKenzie)

- Comments:

- 30347, 1,250, CLR, Holstein Federal 9-25H1, Elm Tree, t7/17; cum --

- 32750, 573, Enerplus, Everest 148-95-12D-01H, Eagle Nest, t7/17; cum --

- 32751, 417, Enerplus, Denali 148-95-12D-01H-TF, Eagle Nest, t7/17; cum -- (#17975)

- 33169, 2,067, Enerplus, Elbert 148-95-12D-01H-TF, Eagle Nest, t7/17; cum --

OMG! Stocks Sink! Investors Seek Safety In Gold, Bonds -- The Market And Energy Page -- T+201, August 9, 2017

Yes, that was the banner over at Yahoo!Finance, at the market close: "Stocks sink, as investors seek safety in gold and bonds."

Here's a screen shot of the headline after the close, screen shot taken at 3:09 p.m. Central Time, US markets closed.

So, how bad was the bloodbath?

Maybe the anti-Trumpers were talking about the best gauge of the market, the S&P:

Wow, this "fake news" really does get tiresome?

It is expected that the US becomes a net exporter of natural gas this year. Something tells me the anti-Trumpers business sites won't make a big deal out of this. Just a few years ago, the US was "frantically" building natgas import terminals: the EIA was forecasting a huge natgas deficit for the US. Now, the US is turning those import terminals into export terminals.

Two days ago it was noted that the Cove Point LNG export facility in Maryland was nearing completion and would begin export operations by the end of the year (2018).

The US will export about 80 million metric tons of LNG annually by 2020; Cove Point will provide about 5.25 million metric tons.

Here are the others:

A nice historical perspective can be found at this post based on an RBN Energy LNG export analysis, October 12, 2016.

Here's a screen shot of the headline after the close, screen shot taken at 3:09 p.m. Central Time, US markets closed.

So, how bad was the bloodbath?

- Dow 30: down 0.17%. On a $1,000-investment across the entire Dow 30, one lost $1.70.

- Nasdaq: down 0.28%. On a $1,000-investment across the entire Nasdaq, one lost $2.80.

Maybe the anti-Trumpers were talking about the best gauge of the market, the S&P:

- S&P 500: down 0.04%. On a $1,000-investment across the entire S&P 500, one lost 40 cents.

Wow, this "fake news" really does get tiresome?

****************************

US Natural Gas Exports

It is expected that the US becomes a net exporter of natural gas this year. Something tells me the anti-Trumpers business sites won't make a big deal out of this. Just a few years ago, the US was "frantically" building natgas import terminals: the EIA was forecasting a huge natgas deficit for the US. Now, the US is turning those import terminals into export terminals.

Two days ago it was noted that the Cove Point LNG export facility in Maryland was nearing completion and would begin export operations by the end of the year (2018).

The US will export about 80 million metric tons of LNG annually by 2020; Cove Point will provide about 5.25 million metric tons.

Here are the others:

A nice historical perspective can be found at this post based on an RBN Energy LNG export analysis, October 12, 2016.

Another Huge Draw: US Commercial Crude Oil Inventories Decreased By 6.5 Million Bbls -- August 9, 2017

From the EIA's weekly petroleum report:

My calculations (parameters previously described) suggest that at the average rate of decline over the past 15 weeks, it will take 35 weeks to "re-balance":

Other highlights:

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 6.5 million barrels from the previous week. At 475.4 million barrels, U.S. crude oil inventories are in the upper half of the average range for this time of year.

Total motor gasoline inventories increased by 3.4 million barrels last week, and are in the upper half of the average range. Both finished gasoline inventories and blending components inventories increased last week.

Distillate fuel inventories decreased by 1.7 million barrels last week but are in the upper half of the average range for this time of year. Propane/propylene inventories remained unchanged last week and are in the lower half of the average range. Total commercial petroleum inventories decreased by 4.6 million barrels last week.

My calculations (parameters previously described) suggest that at the average rate of decline over the past 15 weeks, it will take 35 weeks to "re-balance":

Week

|

Date

|

Drawdown

|

Storage

|

Weeks to RB

|

Week 0

|

Apr 26, 2017

|

529.0

|

180

|

|

Week 1

|

May 3, 2017

|

0.9

|

528.0

|

198

|

Week 2

|

May 10, 2017

|

6

|

522.0

|

50

|

Week 3

|

May 17, 2017

|

1.8

|

520.2

|

59

|

Week 4

|

May 24, 2017

|

4.4

|

515.8

|

51

|

Week 5

|

May 31, 2017

|

6.4

|

509.9

|

41

|

Week 6

|

June 7, 2017

|

-3.3

|

513.2

|

60

|

Week 7

|

June 14, 2017

|

1.7

|

511.5

|

57

|

Week 8

|

June 21, 2017

|

2.5

|

509.0

|

62

|

Week 9

|

June 28, 2017

|

-0.2

|

509.2

|

71

|

Week 10

|

July 6, 2017

|

6.3

|

502.9

|

58

|

Week 11

|

July 12, 2017

|

7.6

|

495.3

|

47

|

Week 12

|

July 19, 2017

|

4.7

|

490.6

|

43

|

Week 13

|

July 26, 2017

|

7.2

|

483.4

|

38

|

Week 14

|

August 2, 2017

|

1.5

|

481.9

|

37

|

Week 15

|

August 9, 2017

|

6.5

|

475.4

|

35

|

Other highlights:

- US refinery throughput hit a record: 17.6 million b/d; an increase of 166,000 b/d compared with the prior week

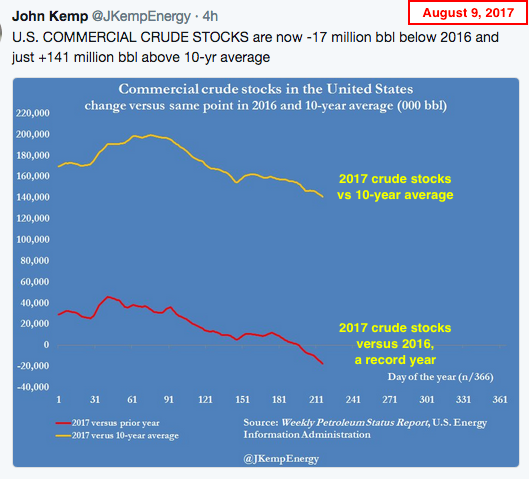

- US commercial crude stocks fell 6.5 million bbls to 475 million bbls; much faster than normal for this time of year

- US commercial crude stocks exhibiting largest summer seasonal draw since 2014

- US gasoline stocks now 5 million bbls below 2016 (a record year); the previous week the number was 11 million bbls below 2016

- John Kemp works hard at putting the Reuters spin on all this. From Kemp, via Twitter: US gasoline supplied averaged 9.8 million b/d last week which was just 28,000 b/d higher than 2016 (fails to mention that 2016 was a record year overall)

The Political Page, T+201 -- GE, The Darling Of The Obama Administration, Immelt, Obama's "Jobs" Czar; GE: Moving A Rochester, NY, Plant To China -- August 9, 2017

I can't make this stuff up. They must have finally gotten tired of:

Meager as their defense budget may be (previously posted), Canada will use soldiers, not for security, but for reception, housing, processing of Haitian refugees streaming across the US border.

Of course, this will only encourage the stream.

Hopefully.

From a contributor over at SeekingAlpha, data points:

Comments: 72. Worth the read.

- the weather;

- the snow;

- the taxes;

- Cuomo;

- the Kardashians; and,

- President Trump

General Electric Corp. (GE) announced that it is closing its plant in Rochester next year and moving operations to China.

The production of the electronic boards that are assembled at the plant will be taken over by Florida-based Jabil Inc. (JBL) in China.I'm going to boycott GE and JBL. LOL.

**************************

Canadian Defense Dollars Spent On Refugees From USA

Meager as their defense budget may be (previously posted), Canada will use soldiers, not for security, but for reception, housing, processing of Haitian refugees streaming across the US border.

Of course, this will only encourage the stream.

Hopefully.

***************************

Tesla's Q2 10-Q

From a contributor over at SeekingAlpha, data points:

- cash is down to $3 billion

- global new vehicle revenues decreased in every country reported

- inventories set new highs; finished goods inventory now stands at $1.5 billion

- Q&A: delayed for fifteen minutes due to microphone problems

- net reservations stood at 455,000 -- not 500,000+

- Tesla delayed spending in 2Q; kicked the "spending can" down the road

- Tesla blew though $1 billion in 2Q

- quarterly loss: $401 million (forecast: if Tesla reported a loss over $400 million, it would be the largest quarterly loss in their short history

- the order book for Model S and X is not longer "important enough" to warrant an answer form Musk Melon

- Friday night news dump: Tesla released its quarterly 10-Q filing to the SEC

- Tesla did not break out sales by model; no one knew why -- now we know why: the biggest drop was in the flagship Model S where US sales are projected to have fallen b over 1,000 units in Q2 from Q1, down from 6,100 to 5,095

- Tesla recently announced a $3,000 price reduction on the Model X

- no company on this planet lowers prices when demand is rising

- more "options" are not becoming standard equipment; customer referrals can reinstate free lifetime Supercharging use

- the real shocker for this contributor: Tesla has slipped 0.9%, 72-month financing into the order pages for both Model S and X on Tesla.com; loan money from Alliance will cost Tesla at least 2.49%; Tesla is stuck with the different; big players use this routinely to move slow inventory; if Tesla is doing so well with sales, why are they now subsidizing financing of new vehicles?

- assumption: the $1.5 billion in bond money will be used to finance new car sales

- completely erases any doubts that Tesla is now demand constrained

- Q2: increased sales activity probably was in used cars, Supercharger fees, and recording revenues form software sales

- bottom line: new vehicle sales fell worldwide in Q2

- revenues increased 157% from a year earlier; costs rose 249%

- no doubt, the largest costs are the disposition of used cars

Comments: 72. Worth the read.

The Market And Energy Page, T+201; Ford Has Pricing Power To Increase Prices On Its Top-Selling Vehicle -- Compare With Tesla -- August 9, 2017

Ford, apparently has the pricing power to raise prices --

significantly -- on its top-selling vehicle, despite intense pressure

from RAM, Toyota, GMC (and they will all raise prices, too) and, yet,

Tesla lowered their prices on the Model X -- a crossover vehicle. That

speaks volumes.

I found it

"ludicrous" that the media seemed to buy into Musk Melon's story that he

could lower prices on the Model X because margins were increasing due

to better efficiencies. LOL. Whatever.

But what irony: Ford is able to increase prices on its huge gas guzzler while Tesla lowers prices on its Model X just when it needs cash most.

From a contributor over at SeekingAlpha:

From investorvillage:

But what irony: Ford is able to increase prices on its huge gas guzzler while Tesla lowers prices on its Model X just when it needs cash most.

From a contributor over at SeekingAlpha:

The shift from cars to SUVs and trucks is a continued positive trend for Ford largely due to the success of the F-Series trucks and increasing popularity of SUVs—Edge, Flex and Explorer.

They are continuing to sell the right mix of vehicles in the U.S. which further pushed up average transaction price up 2.4% compared to the industry average of only 1.7%.

This shows that Ford isn’t just taking advantage of cars being loaded with more safety features and connectivity options, but they are perfectly positioned to take advantage of the consumer shift away from cars to larger vehicles.

The largest contributor to this was the Ford F-Series Super Duty pickup which represented 53% of the mix and contributed a $55,000 per truck price tag, which was a $4,600 increase from July 2016. Additionally, the Ford Explorer and Escape continued to fuel a year-to-date through July record for the Ford brand SUV segment.To repeat: Ford is perfectly positioned to take advantage of the consumer shift away from cars to larger vehicles. And Tesla is positioning itself to take the lead in low-margin (probably loss-leading) sedans.

********************************

Plains All American Shares "Tank"

From investorvillage:

Investors in master limited partnerships don't like distribution cuts.

Case in point: With profits evaporating in its "supply and logistics" business, Plains All American Pipeline (PAA) lowered its forward guidance and indicated it would reduce its distribution.

The shares were down about $4, or 16%, to $21.20 as of 1 p.m. ET Tuesday.

Its general partner, Plains GP Holdings (PAGP), was down a similar amount. While the company didn't cut its payout, it indicated it is changing the way it calculates distributions since one division is drastically underperforming.

Stifel analyst Selman Akyol has changed his model to reflect a $1.80 annual distribution, down from $2.20, an 18% cut. the shares currently yield over 10%, which would be expected to drop to 8.4% if the cut is as big as Akyol expects.A yield of 10% going to 8.4% -- two comments:

- who actually thought a 10% payout could be sustained in this environment; and,

- the reaction of shareholders seems to be a bit overdone.

Understanding Terms Used In Oil And Gas Sector -- Bakken 101 -- August 9, 2017

From the EIA to help understand terms in the oil and gas sector:

The Mancos Shale In New Mexico

BP reports a gusher: the Mancos play in New Mexico; from Bloomberg via Rigzone --

For a look at the Mancos in New Mexico, see this link, which will take you to a PDF:

For an extraordinary story on the Mancos -- but this in Colorado -- see this post. The Colorado Mancos is linked at the sidebar at the right. For reminders, from that post:

"The Sleeping Giant" -- X-Strata.

Another natural gas formation in North Dakota.

While other natural gas drillers are paying a premium for acreage in prized U.S. shale formations across Texas and Pennsylvania, BP Plc may have just found a gem in a largely ignored corner of New Mexico.

The London-based oil giant started producing from a gas well in New Mexico’s Mancos shale that could turn out to be a “significant new source of U.S. natural gas supply,” according to a statement Monday. The well averaged 12.9 million cubic feet a day in its first month, the highest output achieved in the San Juan Basin in 14 years.Data points to follow.

For a look at the Mancos in New Mexico, see this link, which will take you to a PDF:

- "The Upper Mancos Shale in the San Juan Basin: Three plays, Conventional and Unconventional," Ronald F. Broadhead

******************************

The Colorado Mancos

For an extraordinary story on the Mancos -- but this in Colorado -- see this post. The Colorado Mancos is linked at the sidebar at the right. For reminders, from that post:

USGS Estimates 66 Trillion Cubic Feet of Natural Gas in Colorado’s Mancos Shale Formation.

The headline fails to note that the previous USGS assessment was less than 2 trillion cubic feet of natural gas.

The report begins: This is the second-largest assessment of potential shale & tight gas resources that the USGS has ever conducted. [Natural gas: Marcellus was probably the largest?]

Then this bombshell:

The Mancos Shale in the Piceance Basin of Colorado contains an estimated mean of 66 trillion cubic feet of shale natural gas, 74 million barrels of shale oil and 45 million barrels of natural gas liquids, according to an updated assessment by the U.S. Geological Survey.This estimate is for undiscovered, technically recoverable resources.The previous USGS assessment of the Mancos Shale in the Piceance Basin was completed in 2003 as part of a comprehensive assessment of the greater Uinta-Piceance Province, and estimated 1.6 trillion cubic feet of shale natural gas.This is extraordinary by any standard. Natural gas:

- In 2003, the USGS estimated the Piceance to hold 1.6 trillion cubic feet of natural gas.

This is extraordinary by any standard. Oil:

- Now, in 2016, the USGS revises that estimate to 66 trillion cubic feet of natural gas.

- If I'm reading this correctly, this is not original natural gas-in-place but what is considered technically recoverable.

- Seventy-four million bbls of shale oil doesn't seem to be trivial either.

- Original oil in place (OOIP) in the Bakken is estimated to be around 500 billion bbls of oil. At 5% primary recovery rate, that works out to 25 billion bbls of oil.

So, 75 million bbls of recoverable oil in this basin seems to be a pretty big story.

******************************

North Dakota Perspective

"The Sleeping Giant" -- X-Strata.

Another natural gas formation in North Dakota.

BP Hits A NatGas Gusher; Petrobras: Off-Shore Oil Can Be Produced For $8/Bbl -- Peak Oil? What Peak Oil? -- August 9, 2017

Updates

Later, 7:02 p.m. Central Time: see comments below.

A reader very knowledgeable in US natural gas takes issue with two EIA prognostications. First: he disagrees that US natural gas demand will be less this year than last year. He argues that the last two winters have been unseasonably warm; this winter is forecast to be much closer to the norm, i.e., colder. If colder has predicted, then natural gas usage will increase for the 2017 - 2018 winter.

If natural gas usage increases this winter, it is very likely, the reader argues, then increased natural gas imports from Canada could offset the exports of natural gas from the southern states which might delay the US being a net exporter of natural gas later this year.

To see the reader's argument and his links to support his arguments, see the comments.

Original Post

BP reports a gusher: the Mancos play; from Bloomberg via Rigzone --

While other natural gas drillers are paying a premium for acreage in prized U.S. shale formations across Texas and Pennsylvania, BP Plc may have just found a gem in a largely ignored corner of New Mexico.

The London-based oil giant started producing from a gas well in New Mexico’s Mancos shale that could turn out to be a “significant new source of U.S. natural gas supply,” according to a statement Monday. The well averaged 12.9 million cubic feet a day in its first month, the highest output achieved in the San Juan Basin in 14 years.Active rigs:

| $49.47↓ | 8/9/2017 | 08/09/2016 | 08/09/2015 | 08/09/2014 | 08/09/2013 |

|---|---|---|---|---|---|

| Active Rigs | 56 | 33 | 73 | 193 | 183 |

RBN Energy: new US cracker demand, exports will strain ethane supply, part 2.

OPEC: apparently OPEC expects laggards to comply more fully with oil cut pact.

Natural gas: US natural gas output will be up in 2017; still below the 2015 record -- EIA.

Petrobras: Brazil's promising pre-salt offshore wells costs about $8 per bbls.

*******************************

Brazil -- On-Shore Shale Oil And Gas

A Long Way Off -- If Ever

Warning: this link will down a PDF from the EIA on your desktop -- https://www.eia.gov/analysis/studies/worldshalegas/pdf/Brazil_2013.pdf.

EIA assessment of Brazil, 2015, beginning on page 9 of the 29-page document at the link:

- most of Brazil's most prolific petroleum basins lie offshore

- Brazil has 18 mostly undeveloped and lightly explored sedimentary basins onshort

- three of these 18 bases have produced significant conventional oil and gas from demonstrated source rock systems

- the main target is the Devonian (Frasnian) marine black shale which is extensively developed in the three structurally simple basins but has relatively modest TOC (2 - 2.5%)

- several other basins in Brazil may have shale gas and oil potential but lack proven source rock systems, are thermally immature, and/or lack sufficient public data for assessment

- Brazil's risked, technically recoverable shale gas and shale oil resources in the three main basins have an estimated 245 Tcf and 5.4 billion bbls

- risked, in-place shale resources are estimated to be 1,279 Tcf of shale gas and 134 billion bbls of shale oil

- no shale-focused exploration leasing of drilling has been announced to date in Brazil

Subscribe to:

Posts (Atom)