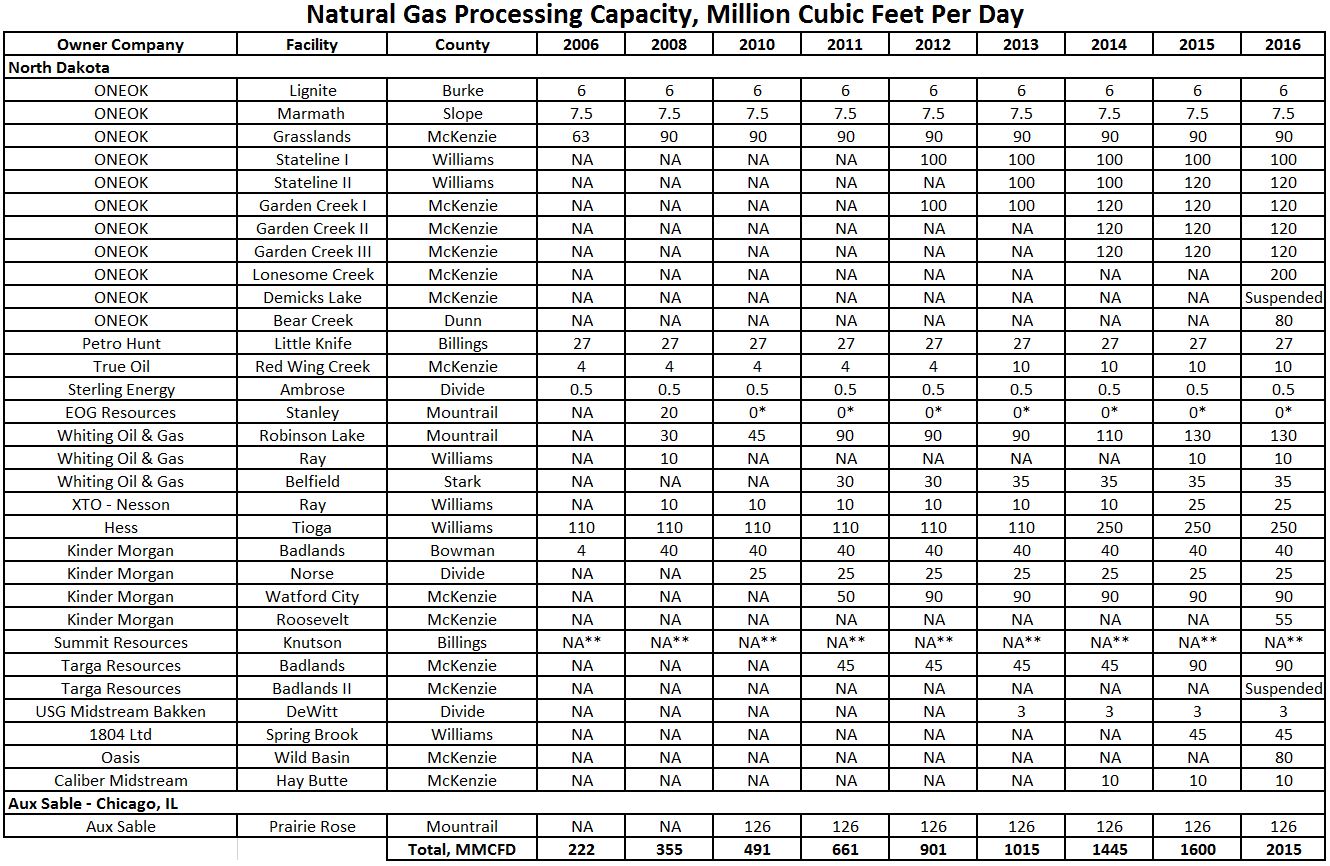

First, here's the link from which I'm operating, an interactive UND-EERC map at http://www.undeerc.org/bakken/dss/. The data apparently is current as of 2012 -- only six years old. LOL.

I then looked at two fields, the Charleson and the Antelope, two very good fields in the Bakken, and fairly underdeveloped back in 2012.

It's hard to say how many wells are actually draining each field, but suffice it to say there are about 40 wells in the Charleson field, and no more than 40 wells in the Antelope field, but for "ease," I will consider 40 wells in each field. The two fields almost touch each other: Charleson, smaller, is to the northwest of the larger Antelope field. I would assume the original oil in place (OOIP) is about the same on a "per-mineral-acre" basis.

Original oil in place (OOIP) in each field (source of data not stated):

- Charleson field: 136,552, 938 bbls of oil

- Antelope field: 805,670,835 bbls of oil

Some are opining that primary recovery might eventually get to 20% in the near term and some suggest as high as 50% in the long term. Don't quote me on any of this; it's just my perception and what I seem to recall. My "recall" is often very, very poor.

With regard to EURs, early in the boom, in this area, EURs were probably estimated at about 500,000 bbls. Since then, EURs have greatly increased.

But for argument's sake, we will suggest that EURs in this area were 500,000 bbls/well back in 2012. By the way, at this time, 2012, most of the wells in the Charleson were Three Forks well (blue in the graphic); in the Antelope, almost all of the wells were middle Bakken wells (red in the graphic).

So, let's run some numbers.

I think one can get any number one wants, but this is what I did.

Charleson:

- 40 wells

- 40 * 500,000 = 20 million bbls EUR

- 20 million / 136,552,938 = 15% primary production (estimate)

- 40 wells

- 40*500,000 - 20 million bbls EUR

- 20 million / 805,670,835 = 2.5% primary production (estimate)

- primary production estimate in Antelope is based on 40 wells; it appears there are clearly less than 40 wells in the Antelope at this time (in other words,that 2.5% primary production might actually be less)

- there's no way that two fields right next to each other should have such disparate primary production estimates

- obviously a lot more wells are going to go in than just the current 40

- I'm misreading something (most likely possibility)

- 15% primary production seems about double what we were being told back in the early boom

- 2.5% (and possibly lower) primary production is ridiculously low, especially considering these were mostly middle Bakken wells

- the estimated OOIPs are ridiculously low (that's my hunch)

I can't wait to see the results of the 2020 USGS survey. I personally think the 2020 USGS survey will, at a minimum, double the reserves estimated in the 2013 USGS survey. We could possibly see a tripling of the reserves. Much of the outcome will depend on the price of oil when they accomplish the survey. The lower benches of the Three Forks were not considered in the 2013 USGS survey.

{kind=link}