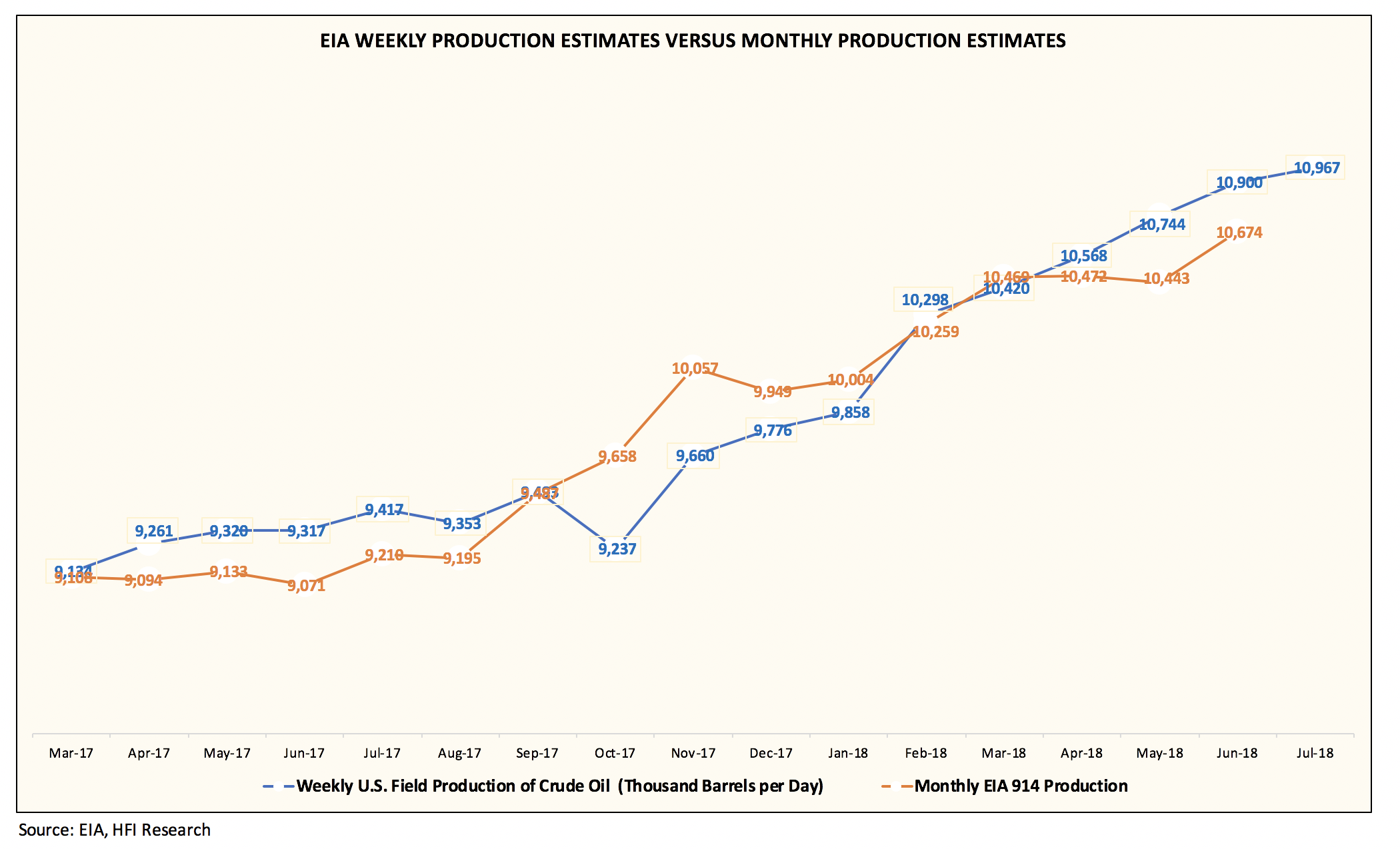

Now, back to the natural gas story.

Updates

September 4, 2018: so much for CO2 and global warming. The Brits are going to use a lot of coal this winter. Natural gas getting too expensive; coal is cheap. Link at Platts (beware: lots of jargon):

Bullish NBP spot and winter contract gas prices have focused the power market's attention on the UK's coal-fired power plants, which have recently become more economical to run in the summer as well as in the winter.

The gap between prompt NBP gas and the coal switching channel indicates that, if and when needed, thermal generation is going to be predominantly coal-fired this winter, with higher gas prices opening the way for increased coal-fired generation, despite a strong hike in carbon prices.

Data show 35% efficient coal-fired plants are competing with 45% gas-fired plants.

The UK month-ahead coal-switching price for 45% efficiency was 68.43 pence/therm on Monday, slightly lower than the NBP day-ahead contract assessment of 69.70 p/th.

However, UK month-ahead CSP for 50% efficiency was 78.19 p/th. Platts CSPI is the theoretical threshold at which gas is more competitive than coal in power generation.

When the gas price is higher than the CSPI, CCGTs are more expensive to run than coal-fired plants.

"Despite the gains in carbon over recent months, coal generation has been supported this week by particular strength in the gas market," according to S&P Global Platts Analytics.

"We forecast gas to lose ground this winter too, with the Q1-19 Clean Dark Spread above the Clean Spark Spread. As a result we expect coal generation to be stable year-on-year this winter, despite the closure of 2GW of capacity, while gas generation is forecast to fall more than 3 GW vs Winter-17."

Original Post

This may be a good evening to re-read this post: Natural Gas Inventories "Dangerously Low."

August 26, 2018: Europe's natural gas prices surge to record for summer season.Natural gas is going to get a bit more expensive "across the pond." Numerous sources are reporting unexpected natural gas production outages in Norwegian gas fields which will cut supplies for up to four weeks.

Europe’s natural gas market is the most bullish it has been in years, as higher-than-expected summer demand and a tighter market drive natural gas price futures to levels last seen during this past winter’s supply crunch and to the highest for a summer season.Natural gas prices are expected to stay strong and may still have room to rally, ahead of the next winter heating season in Europe that begins in October.Contrary to the typical summer lull in Europe’s gas prices, this year the front-month gas price in the UK—Europe’s biggest gas market—for example, is nearing the winter price from December 2017 when a deadly explosion in Austria’s gas hub at Baumgarten squeezed supplies throughout Europe. Immediately after the explosion, the price of gas for immediate delivery in the UK reached its highest level since 2013.

Two more links of interest:

- UK's energy production fell for the 11th straight year, 2013: link here.

- UK energy production production falls again, 1Q18: link here. A lot of interesting statistics.

*********************************

A Play-Doh Afternoon

I couldn't decide which one to post. Photos by Sophia's grandmother.

***********************************

The Book Page

River: One Man's Journey Down the Colorado, Source to Sea, Colin Fletcher, 1997.

The author has reached mile marker 931, at the Utah/Arizona state line, and has just re-entered the Colorado River south of the Glen Canyon Dam. The story continues:

Today, Lee's Ferry is the put-in point for Grand Canyon river-runners. (Fifty-mile-long Marble Canyon, immediately belw Lee's Ferry, is sometimes regarded as part of the Grand Canyon, sometimes not. It now lies within Grand Canyon National Par, but at the time of my 1963 foot trip the park ended at Nankoweap Creek, where Marble melds into Grand, so I tend to award Marble Canyon autonomy.)

At Lee's Ferry Ranger Station the National Park Service checks all river-running permits. There's a heavy demand for permits and the Park Service has to ration them, then control entry tightly. People who want to make a noncommercial river-run through the Canyon normally go on a waiting list and it may take years for their names to come up. I managed to short-circuit the procedure -- but one condition of my permit was that I explain why I got special treatment.

So you are hereby advised that because I had in 1963 become the first man known to have walked the entire Canyon in a single journey, and because my book about it was still in print, the Park Service felt I'd shown I could both take care of myself and also produce something worthwhile, and that they could therefore bestow on me an immediate permit for "literary research."

I was and am truly grateful for this NPS dispensation. But I must explain that phrase "literary research." It will surely provoke somebody into saying "Ah! So he went down the river just to write a book about it!" I did not. On the other hand, I knew I'd write a book if the journey generated one -- which not every long wilderness journey I'd undertaken had done.

Things have to be right.

{kind=link}

{kind=link}