Focus on fracking: link here --

- natural gas price: 14-year high

- US oil exports at a record high

- US oil supplies (SPR + commercial): at an 18.5 year low

- DUCs: at a record low

US oil data from the US Energy Information Administration:

For the week ending August 12th indicated that after a record jump in our oil exports, we had to pull oil out of our stored commercial crude supplies for the 5th time in 9 weeks, and for the 22nd time in the past 38 weeks, despite another big withdrawal of crude from the SPR, and despite a big jump in oil supplies that could not be accounted for....Our imports of crude oil fell by an average of 39,000 barrels per day to average 6,132,000 barrels per day, after falling by 1,171,000 barrels per day during the prior week, while our exports of crude oil jumped by a record 2,890,000 barrels per day to average a record 5,000,000 barrels per day, which meant that our trade in oil worked out to a net import average of 1.132,000 barrels of oil per day during the week ending August 12th, 2,929,000 fewer barrels per day than the net of our imports minus our exports during the prior week.Over the same period, production of crude from US wells was reportedly 100,000 barrels per day lower at 12,100,000 barrels per day, and hence our daily supply of oil from the net of our international trade in oil and from domestic well production appears to have totaled an average of 13,232,000 barrels per day during the August 12th reporting week… With our oil exports at a record high, we'll include a historical graph of them below, where you can see that prior to the end of 2014, US oil exports, except for those allowed under NAFTA, had been negligible because they had been banned 40 years earlier, in the wake of the Arab oil embargo. The ban on US oil exports was lifted in a spending bill that Congress passed during the last week of 2015, part of a compromise that Obama agreed to in order to avoid a government shutdown...

... as you can see, this week’s spike clearly beat previous oil export highs by a large margin...

Meanwhile, US oil refineries reported they were processing an average of 16,423,000 barrels of crude per day during the week ending August 12th, an average of 158,000 fewer barrels per day than the amount of oil than our refineries processed during the prior week, while over the same period the EIA’s surveys indicated that a net average of 1,494,000 barrels of oil per day were being pulled out of the supplies of oil stored in the US.

So, based on that reported & estimated data, the crude oil figures from the EIA for the week ending August 12th appear to indicate that our total working supply of oil from net imports, from oilfield production, and from storage was 1,697,000 barrels per day less than what our oil refineries reported they used during the week.

To account for that disparity between the apparent supply of oil and the apparent disposition of it, the EIA just inserted a (+1,697,000) barrel per day figure onto line 13 of the weekly U.S. Petroleum Balance Sheet in order to make the reported data for the daily supply of oil and for the consumption of it balance out, a fudge factor that they label in their footnotes as “unaccounted for crude oil”, thus suggesting there must have been an omission or error of that magnitude in this week’s oil supply and demand figures that we have just transcribed....

... moreover, since last week’s EIA fudge factor was at (+343,000) barrels per day, that means there was a 1,354,000 barrel per day difference between this week's balance sheet error and the EIA's crude oil balance sheet error from a week ago, and hence the week over week supply and demand changes indicated by this week's report are worthless...

... however, since most everyone treats these weekly EIA reports as gospel, and since these figures often drive oil pricing, and hence decisions to drill or complete oil wells, we’ll continue to report this data just as it's published, and just as it's watched & believed to be reasonably accurate by most everyone in the industry...(for more on how this weekly oil data is gathered, and the possible reasons for that “unaccounted for” oil, see this EIA explainer)….

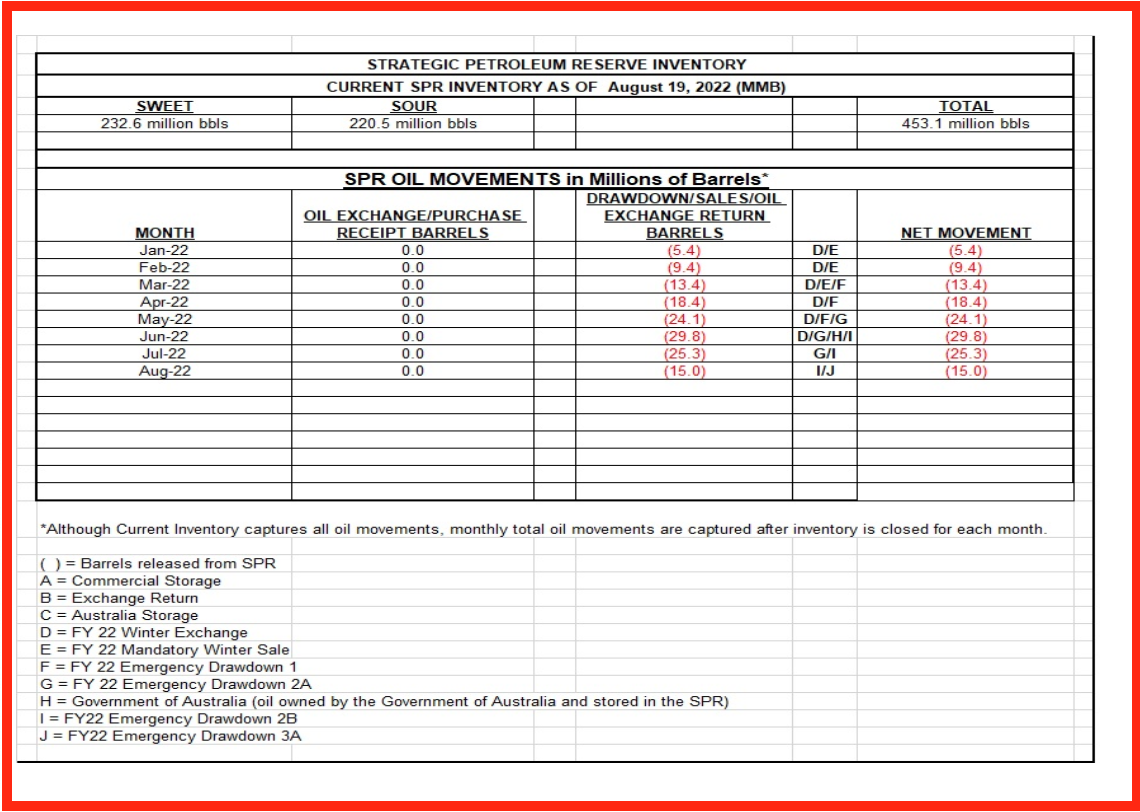

This week's 1,494,000 barrel per day decrease in our overall crude oil inventories left our oil supplies at 886,110,000 barrels at the end of the week, which is our lowest total oil inventory level since September 19th, 2003, and therefore at a new 18 1/2 year low (see graph below)….our oil inventories decreased this week as 1,008,000 barrels per day were being pulled out of our commercially available stocks of crude oil and 486,000 barrels per day of oil were being pulled out of our Strategic Petroleum Reserve.

The draw on the SPR was part of the emergency withdrawal under Biden's "Plan to Respond to Putin’s Price Hike at the Pump" (sic), that was expected to supply 1,000,000 barrels of oil per day to commercial interests over a six month period up to the midterm elections in November, in the hope of keeping gasoline and diesel fuel prices from rising further, at least up until that time.

The administration's previous 30,000,000 million barrel release from the SPR to address Russian supply related shortfalls wrapped up in June, and his earlier release of 50 million barrels from the SPR to incentivize US gasoline consumption was completed in May...

Including those, and other withdrawals from the Strategic Petroleum Reserve under recent release programs, a total of 194,993,000 barrels of oil have now been removed from the Strategic Petroleum Reserve over the past 25 months, and as a result the 461,156,000 barrels of oil still remaining in our Strategic Petroleum Reserve is now the lowest since March 22nd, 1985, or at a new 37 year low, as repeated tapping of our emergency supplies for non-emergencies or to pay for other programs had already drained those supplies considerably over the past dozen years, even before the Biden administration's SPR releases. Now the total 180,000,000 barrel drawdown expected during the current six month release program to November will remove almost a third of what remained in the SPR when the program started, and leave us with what would be less than a 20 day supply of oil at today's consumption rate...

By the way, it will be announced this week, perhaps as early as today, August 22, 2022, that another 20 million bbls of oil will be released from the SPR.