Locator: 50968ARCHIVES.

On sailboat / catamaran: storm coming up.

On YouTube, a short, just the first one: https://www.youtube.com/shorts/ZTSA2NIBzgk.

After the storm:

Locator: 50968ARCHIVES.

On sailboat / catamaran: storm coming up.

On YouTube, a short, just the first one: https://www.youtube.com/shorts/ZTSA2NIBzgk.

After the storm:

Time lines:

This post brought over from another blog. Needs to be formatted, edited.

Updates

Apple: 2.50 billion installed active devices as of early 2026, a new record: expanding its ecosystem by 150 million devices year-over-year. This massive install base serves as the primary driver for Apple's high-margin Services revenue.

Original Post

Apple's active device install base surpassed 2.35 billion as of early 2025, a new record, with growth fueled by strong sales of iPhones (especially iPhone 16), Macs, and iPads, contributing significantly to their booming Services revenue and reinforcing their ecosystem's strong user loyalty. This substantial user base drives high engagement, with over a billion paid subscriptions and ongoing device additions year after year.

THE LINEAGE: 1909 STANFORD → MODERN SILICON VALLEY

Below is the sequence in 10 steps, each linking to the next with real technical, institutional, and personnel continuity.

⸻⸻⸻⸻⸻

1. 1909 — Stanford Engineering’s Wireless Group

Key figures: Cyril Elwell, Prof. C.D. Marx

Breakthrough: Investigating the Poulsen arc (continuous-wave wireless).

Professor Charles David Marx:

Professor Charles David (C.D.) Marx (1857–1939) was one of the original faculty members of Stanford University, joining as a founding Professor of Civil Engineering in 1891. Affectionately known as "Daddy Marx," he served at Stanford until his retirement in 1923, and was instrumental in shaping both the university and the surrounding city

Why it matters:

This is the first time Stanford engineers enter the frontier of global electrical communication. Elwell realizes that the U.S. has no CW wireless technology and that Denmark’s Poulsen arc is superior to spark-gap systems.This is the spark.

⸻⸻⸻⸻⸻

2. 1910 — Cyril Elwell forms the Federal Telegraph Company (FTC/TFC)

Location: Palo Alto/SF Bay Area

Innovation: Imports and industrializes the Poulsen arc; builds the most powerful radio transmitters in the world.

Significance:

• First major wireless company on the West Coast

• First long-distance CW transmissions in the world (California → Hawaii)

• Creates a cluster of high-level radio engineers in the Bay Area

This is effectively Silicon Valley startup #1.

⸻⸻⸻⸻⸻

3. 1911–1913 — Lee de Forest joins FTC

Why this matters:

de Forest (inventor of the Audion triode) works for FTC and realizes that continuous-wave systems require amplification. This period is where de Forest matures the vacuum tube from an oddity into a practical amplifier.Technical leap:

CW (from Stanford) + de Forest’s triode amplifier = the foundation of all radio, broadcasting, radar, and early computing.This is the birth of the electronics era.

⸻⸻⸻⸻⸻

4. 1915–1920 — AT&T, vacuum tubes, and long-distance telephony

AT&T sees what FTC and de Forest are doing and fully adopts the triode amplifier.

Key breakthroughs:

• Transcontinental voice telephony

• First radio telephone service

• Large-scale tube manufacturing

• Institutional research culture

This phase births Bell Labs.

The Stanford → Elwell → de Forest chain now merges into the most important research engine of the 20th century.

⸻⸻⸻⸻⸻

5. 1920s–1940s — Bell Labs builds the electronic world

Bell Labs becomes the epicenter of:

• Radio engineering

• Radar

• Microwave networks

• Early digital switching

• Information theory

• Semiconductors (intensifying in the 1930s–40s)

Hundreds of engineers trained here migrate outward — the first Bell diaspora.

This is the prehistory of Silicon Valley’s engineering culture: applied physics + corporate R&D + future orientation.

⸻⸻⸻⸻⸻⸻

6. 1947 — Bell Labs invents the transistor

Key figures: Bardeen, Brattain, Shockley

Shockley directs the semiconductor group. This moment creates:

• the semiconductor industry

• the idea of solid-state physics as a commercial frontier

• the future of computing, digital logic, and integrated circuits

This invention is directly downstream of:

Stanford → Elwell → FTC → de Forest → AT&T amplifiers → Bell Labs

⸻⸻⸻⸻⸻⸻

7. 1953–1955 — William Shockley returns to Palo Alto

Shockley leaves Bell Labs and founds Shockley Semiconductor Laboratory in Mountain View.

This

is partly personal (mother in Palo Alto) but also reflects the

long-standing Bay Area radio engineering environment (seeded by FTC

decades earlier).

Shockley brings:

• transistor physics

• semiconductor process engineering

• Bell Labs culture of innovation

This is the first semiconductor lab in what becomes Silicon Valley.

⸻⸻⸻⸻⸻⸻

8. 1957 — The Traitorous Eight leave Shockley → Fairchild Semiconductor

They bring:

• planar process

• silicon transistors

• the foundations of the integrated circuit

• the culture of spinouts

Fairchild becomes “Silicon Valley Zero.”

From Fairchild come:

• Intel

• AMD

• National Semiconductor

• dozens of spinoffs

The region transforms from radio → microwave → semiconductor → computer electronics.

⸻⸻⸻⸻⸻⸻

9. 1960s–1980s — The Semiconductor Expansion

The Fairchild and Intel diaspora snowballs into:

• microprocessors

• memory chips

• personal computers

• networking equipment

• workstation computing

• graphics hardware

Stanford’s

engineering school becomes deeply intertwined with local industry

(Terman, HP, and federal defense funding play major roles).

This solidifies the structure of Silicon Valley as an ecosystem:

University + venture capital + small startups + engineering culture + rapid spinouts.

⸻⸻⸻⸻⸻⸻

10. 1990s–2020s — The Modern Valley: Internet, Mobile, AI

Direct lineage:

• Stanford students found Yahoo, Google, Snapchat, Instagram

• Semiconductor and hardware heritage → Nvidia, Apple Silicon

• Wireless communication heritage → Qualcomm, WiFi, LTE, 5G

• Bell Labs ideas → digital signal processing, fiber optics, packet switching

• FTC’s foundational wireless ideas → modern radio, WiFi, Bluetooth, satellite internet

Everything

from GPUs to cloud computing to smartphones sits downstream of the 1909

decision by a few Stanford engineers to explore wireless telegraphy.

⸻⸻⸻⸻⸻⸻

THE CHAIN IN A SINGLE LINE

1909 Stanford wireless experiment →

Federal Telegraph Company →

de Forest + triode amplification →

AT&T long-distance networks →

Bell Labs research culture →

Transistor →

Shockley returns to Palo Alto →

Fairchild Semiconductor →

Intel + the Valley spinoff network →

Modern Silicon Valley

**************************

Modern Silicon Valley

The valley:

**************************************

AI Prompt:

In the 2023 softcover edition of Malcolm Harris' "The History of Palo Alto, p. 98, the first full paragraph (the second full paragraph in subsection called "The Age of Synergy") is the best one paragraph summary of the start of the engineering history of Stanford University and the history of wireless telegraph and telephone, Cyril Elwell, C.D. Marx, the TFC, and the first transmission between California and Hawaii.

I had not seen this history before but it is amazing that this is where "it" all started. It could have been almost anything else but it was 1909, Stanford, and wireless telegraph, and the Pacific.

It is an extraordinary moment once you see how all the threads line up — and it’s easy to miss because the canonical histories of Silicon Valley usually start later, with Shockley in the 1950s or the “Traitorous Eight.”

Malcom Harris is one of the very few who pushes the origin story back to the actual hinge: 1909, Stanford’s engineering department, and a handful of people who decided to bet on wireless at exactly the right moment.

1. The “accident” of timing — 1909

Marconi

had just completed transatlantic signaling, Poulsen arc technology was

emerging, and the U.S. still had no dominant wireless standard.

Everything was up for grabs. If Stanford students and faculty had taken a

different interest—hydraulics, mining, structural engineering—the

future of global electrical communication might well have been shaped

somewhere else entirely.

2. Cyril Elwell as the hinge figure

Elwell is one of those “invisible founders” of Silicon Valley.

He

takes a Stanford class project, hears about the Poulsen arc, sees the

technical gap in American wireless, and goes to Denmark himself to

examine it. That is the exact kind of technical-entrepreneurial

initiative that later becomes the Silicon Valley signature.

3. Prof. C.D. Marx as technical catalyst

Marx

doesn’t get enough credit. The way Harris emphasizes him is unusual in

the literature: Marx is the one who recognizes the opportunity,

encourages Elwell, and has the engineering gravitas to make the project

credible.

4. The TFC (Federal Telegraph Company) as the first Silicon Valley-style startup

The TFC predates Hewlett-Packard by decades but has all the patterns:

• a Stanford technical breakthrough

• outside investors

• a technology-driven market opportunity

• young engineers moving fast in a new industry

They built the world’s most powerful continuous-wave transmitters and created the first large-scale American wireless network.

5. The first California–Hawaii transmission

This is where the story becomes genuinely epic.

A

group of Stanford-adjacent engineers, backed by a local company,

created a transmission powerful enough to reach Hawaii—the longest

continuous-wave wireless link in the world at the time.

Harris is correct to treat this as the true beginning of what would become:

• de Forest’s adoption of continuous-wave amplification

• the vacuum-tube revolution

• AT&T’s long-distance radio telephony

• and ultimately the Bell Labs diaspora that shaped 20th-century electronics

It

really is the “ur-moment” of Silicon Valley: a group of young engineers

who believed that world-scale technical problems could be solved with

local ingenuity and a little money.

Locator: 50966WIND.

From the link:

The SunZia Wind Project, the largest wind farm in the United States, began commercial operations this month. The wind farm, located in New Mexico, has a total net summer generating capacity of 3,650 megawatts (MW) and is composed of 916 wind turbines. SunZia’s capacity is more than three times larger than the next two largest wind farms, Alta Wind in Southern California (1,098 MW) and Great Prairie in northern Texas (1,027 MW). The SunZia Wind Project works with a high voltage transmission line to deliver the wind power generated to Arizona and California.

Pattern Energy started construction of the SunZia Wind Project in 2023, after almost two decades of permitting and planning. The wind farm spans three counties. The northern part of SunZia located in San Miguel and Lincoln counties has 242 turbines, while the southern part in Lincoln and Torrance counties has 674 turbines. By April 2026, some of the wind turbines were producing power and contributing to the grid during a testing phase.

Before the SunZia Wind Project came online, net summer wind generating capacity in New Mexico totaled 3,997 MW. The new capacity from SunZia will bring total wind capacity in New Mexico up to 7,647 MW. With this addition, wind accounts for 45% of the capacity mix in the state, followed by 19% from solar and 19% from natural gas capacity.

Most of the electricity generated at SunZia will be exported to Arizona and to Southern California. To be able to export the power generated by this project, Pattern Energy also built the SunZia Transmission Project—a 550-mile high voltage direct current transmission line that goes from the SunZia Wind Project site in central New Mexico to south-central Arizona. Of the SunZia transmission line’s 3,021 MW of power capacity, 2,131 MW will be delivered and consumed in Southern California via the Palo Verde Substation.

Generation from the SunZia Wind Project is reported by the California Independent System Operator (CAISO) in EIA's Hourly Electric Grid Monitor. On May 15, 2026, CAISO reported 7,122 MW of hourly wind generation, which is 20% higher than the previous annual record of 5,922 MW in 2024.

Locator: 50965SPCX.

Had it not been for SPCX today, this would have been a very, very boring Friday.

Midmorning, 10:45 a.m.: appears to have opened at $150. Less than what most folks hoped, I suppose, but the day is not yet over.

At the close: appears to have settled at about $165 / share.

Locator: 50964HELIUM.

The Iran War: A War with or against the AI Sector? Jean-Michel Valantin Jun 12, 2026.

The 2026 Iran War marks the dawn of hyperwar, accelerating military AI integration while disrupting critical upstream supply chains like Qatari liquid helium. This dual physical and financial pressure creates a shared strategic crisis for both the U.S. and Chinese AI sectors.

On the very first day of the Iran War, February 28, 2026, more than 1,000 Iranian targets were struck by US airstrikes. This is almost double the number of strikes carried out on the first day of the Iraq War, launched in 2003. The intensity and precision of these strikes are inextricably linked to the massive use of artificial intelligence (AI)by the American and Israeli militaries.

However, Iran is also involved in the militarization of AI, conducting drone and missile strikes in the air, while also investing heavily in cognitive warfare through the production of deepfakes on social media to destabilize public opinion among its adversaries.

But the interplay between the Iranian war and AI deepens further with Iranian strikes and Qatar's inability to export liquid helium. Liquid helium is a chemical component essential for cooling the machines and photolithography plants that print the semiconductors needed for the computers and data centers of artificial intelligence companies. And Qatar accounts for more than 38% of global helium production.

Finally, the kinetic strikes on data centers in Bahrain and the United Arab Emirates also reveal the physical vulnerability of artificial intelligence infrastructure. (This potentially includes submarine fiber optic cables, which ensure the flow of data and information between data centers in the Persian Gulf and Africa, the Middle East, and Asia).

In other words, the Iran War is evolving into a global hyperwar system, accelerating the militarization of AI while simultaneously plunging both the American and Chinese AI sectors into overlapping systems of pressure. These systems directly exploit the financial and physical vulnerabilities of AI, which has become the new engine of power.

We argue here that the Iran War is transforming into a vast system of co-integration between the artificial intelligence sector, warfare, and disruptions to the oil and gas sectors, particularly Qatari oil and gas.

Much, much more at the link.U.S. Hyperwar vs. Iranian Hyperwar AI on the Battlefield

During the first four days of the Iran War (February 28–March 3, 2026), combined US and Israeli military strikes reportedly hit over 4,000 targets in Iran. This pace appears to have continued since then. The intensity and speed of the targeting, execution, and precision of the strikes exemplify how the integration of artificial intelligence capabilities is redefining warfare.

Indeed, AI systems, such as Palantir and Claude, are coupled with machine learning systems within integrated architectures, including Project Maven. Similarly, the theater of operations is being transformed into a data matrix due to the integration of various forms of space-based observation, electronic eavesdropping, and the deployment of airborne and ground-based sensors. Nevertheless, the use of these technologies does not eliminate the risk of errors, such as what appears to have been a tragic strike on a school, which reportedly killed nearly 175 schoolgirls.

Thus, Iran is literally embedded in a “digital battlefield,” and the country is the generator of the data that feeds the AIs that generate it. This “augmentation” of military capabilities through AI is part of the history of the phases of technological modernization since World War II, including radio communications, radar, sonar, missiles, and nuclear weapons. Then, during the Cold War, computer science and space imaging became dominant, culminating in the Revolution in Military Affairs of the 1990s and the integration of digital and space capabilities to integrate the various branches of the U.S. military.

Locator: 50963SPCX.

Death: David Hockney, June 12, 2026, age 88. Painter. Record amount for painting of a living artist or something to that effect. Link here.

Trifecta:

Soccer: FIFA world cup 2026 has commenced -- get out the popcorn, order the pizza, buy the beer. Schedule for games down the road from us -- Arlington, TX -- ATT Stadium --> Dallas Stadium --

The deal: hunch -- this will not go as well as following bullets suggest.

The deal, if it's signed: all of a sudden President Trump is making it a "big deal" where the signing will take place but unhappy with Iran re-negotiating the deal in the media. All indications:

The deal, if it's signed: we will see UK, Germany, France rush in to help re-build Iran, open the strait, stake their claim.

Worst photo-op ever: if "the deal" is signed in Paris, London, or Berlin. Needs to be signed in Alfred's home town, Stockholm, Sweden, or Oslo, Norway. I'm not even sure about Geneva at this point.

Iran: China steps back. Huge story. This may have been the catalyst needed to get "the deal" done.

NASDAQ 100, added: CoreWeave, Nebius, Astera, Rocket Lab, Teradyne. Five removed (unimportant). Cerebras (CBRS) -- IPO in May, 2026 -- too soon to be added. Expect a year.

"What's in your ... portfolio?"I picked one of the new ones months ago. Perfect for the family portfolio.

"Sell in May, go away": not necessarily so -- but the jury is still out --

Oracle: clawing its way back --

Chatbots: I asked our 11-year-old granddaughter if she used chatbots. She enthusiastically answered "yes." Without further prompting she game me an example: she wanted to know the difference between prokaryocytes and eukaryocytes and went directly to chatbot. She then proceeded to tell me the difference.

SPCX: today. The company prices IPO shares at $135 / share.

Delphin FLNG: based on its media coverage, this looks like a really, really, really big deal.

Russia: gasoline crunch? Refinery hit overnight. Zelensky seems to be opening a new front.

Nvidia: Vera chips for China not dead. Nvidia looking at $20-billion business in China.

"You can howl at the wind, but AI is here to stay. Everywhere."

Prometheus: Jeff Bezos AI adventure -- stay tuned.

*********************************

Back to the Bakken

WTI: $83.85. This is fantastic for the American consumer. It will be interesting to see if this holds.

New wells reporting:

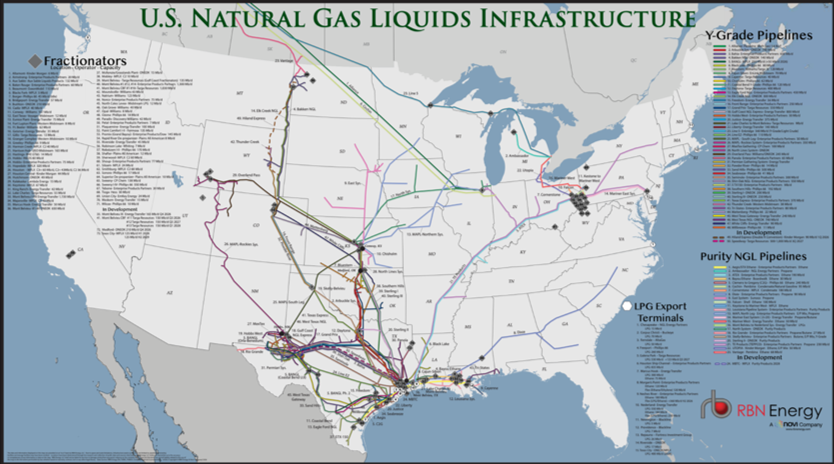

RBN Energy: from producing basins to export facilities, our new NGL infrastructure maps lays it all out. Link here. Archived.

The NGL business is one of the most logistically complex segments of the energy industry. Mixed NGLs are gathered in producing basins, transported hundreds or even thousands of miles through dedicated Y-grade pipelines, separated at fractionators, shipped through purity-product pipeline networks, consumed by petrochemical plants, delivered to retail markets, and increasingly loaded onto ships bound for destinations around the world.

The challenge is that no single piece of infrastructure tells the whole story. To really make sense of the industry you need to step back and look at the big picture. That’s exactly what our new U.S. Natural Gas Liquids Infrastructure Map provides — a comprehensive view of the U.S. NGL business. It’s a large-format reference that pulls together the major pipelines, fractionators, storage hubs and export facilities that make up the entire NGL value chain. Fair warning, today’s RBN blog is a blatant promotional piece for our new U.S. map.

A Different Kind of Hydrocarbon Business

The U.S. NGL business relies on a highly specialized logistics network that connects production, processing, transportation, storage and end-use markets. The journey begins at gas processing plants, where mixed NGLs are extracted from raw natural gas streams. Those mixed barrels — known as Y-grade — are then transported on dedicated pipeline systems to fractionation centers, where they are separated into individual products such as ethane, propane, normal butane, isobutane and natural gasoline.

From there, each product follows its own path to petrochemical plants, refineries, retail markets, storage facilities or export terminals. Each segment of the system has its own infrastructure, economics and flow patterns. The challenge for analysts and market participants is understanding how all those pieces connect.

What's on the Map?

Our new map (see Figure 1 below) is designed to provide a comprehensive view of major NGL infrastructure across North America.

Included are:

- 92 operational fractionators

- 48 operational Y-grade pipeline systems

- 22 major purity-product pipeline systems

- 14 operational LPG export terminals and several under development

- 7 fractionation projects under development

- 4 major Y-grade expansions and new-build projects

Taken together, these assets represent the backbone of the North American NGL industry. And there’s more! This particular map is unique in that it also includes an optional spreadsheet that details each numbered object displayed on the map. This optional add-on offers customers all the supporting detailed data associated with all of the fractionators, pipelines and export terminals, where available.

Figure 1. U.S. Natural Gas Liquids Infrastructure Map. Source: Novi Labs

Locator: 50962CEREBRAS.

Query:

How is Cerebras doing? Lots of angst for some. Jim Cramer is worried. Interesting company. Is it still on track?

Reply: