Locator: 50467EPICFURY.

Several points need to be made:

First, without question, this is a huge win for everyone.

This --> Operation EPIC FURY. No one got everything they wanted, but everyone got something. Even Iran. They get a chance to rebuild.

Two, Trump got his needed "off-ramp."

Mainstream media keeps using the phrase "Trump was desperately looking for an off-ramp." He wasn't desperate at all; the Iranians were desperate and running out of time, finally settled for a two-week-cease-fire and a 10-point plan of their own that won't go anywhere. [Typo: that two-cease-fire should read "two-week cease fire."]

Agreeing to a two-week-cease-fire and a 10-point plan is standard negotiating procedure by the IRGC to save face, re-arm, and tweak their plan.

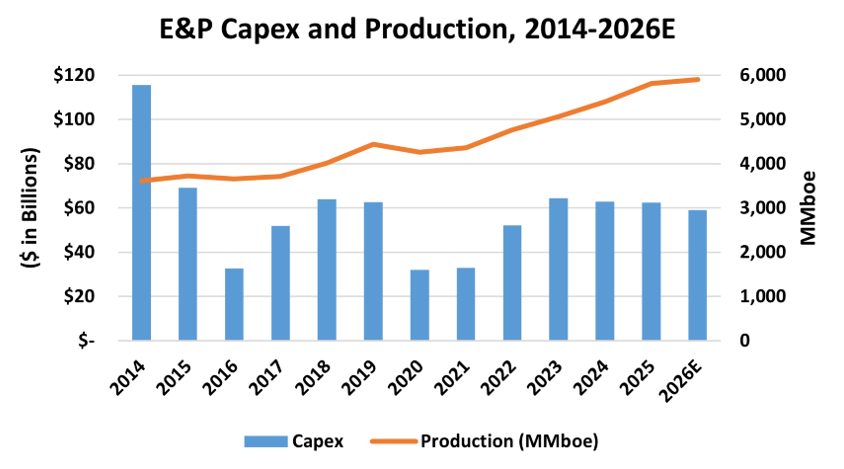

Three, "we" may have just avoided a global recession.

Four, if one is able to think strategically, Trump's actions will be described as "TECTONIC" by historians in 2040. Trump will be treated like Churchill after WWII. Exception: the Israelis will know and will be forever grateful.

Five: for the military, lessons learned.

No other country is getting the wartime experience that the US is getting. The Maduro extraction and the highly successful search-and-rescue of two downed US airmen were EPIC.

Six: the US has the best intel agencies in the world. Much could be said. Much more cannot.

Seven: Artemis II is getting more attention than the ceasefire -- four astronauts flying around the moon and coming home with an album full of "I Love Me" photos; other highlights: "Outlook" failing almost immediately after launch, as well as the toilet.

And to think we're going to Mars any time soon? With regard to flying around the moon and back:

- four Corgis could have replaced the astronauts on this mission and they would have been cuter and more lively;

- we did the same thing -- multiple times -- fifty years ago and landed men on the moon safely and back again six times -- Apollos 11 - 17 inclusive except #13 -- and they did the same thing these four astronauts did with a lot more excitement, nerve, and heroism -- and four Corgis could not have done what the following did, Apollo 13:

- Commander James A. Lovell, Jr.

- Commander Module Pilot John L. "Jack" Swigert, Jr.

- Lunar Module Pilot Fred W. Haise, Jr.; and

- Flight Director for getting them safely home, Gene Kranz (no, not "Jr.")

Eight: the US learns who its allies really are.

I'm thinking, maybe Israel is one of the few. Certainly not the UK, France, or the others that Trump himself named. Now we're getting stories NATO countries were actually helping secretly and behind the scenes. Oh, give me a break. It gets tedious.

Nine: the US military-industrial complex will rebuild the arsenal and work to make sure this never happens again (a shortage of bombs, and missile, and drones, and ....). The US drone industry is going to exceed all expectations.

President Trump has submitted a record-setting DOD budget to Congress.

Ten: for the time being, the Persian Gulf becomes Trump's Lake. No one will complain: not China, and that may be the most important country on that "list." Along with the GCC, of course.

Eleven: the US is now the supplier of oil and natural gas of last resort -- Saudi Arabia can no longer be seen as the "swing producer" and certainly Qatar has lost its reputation of the most reliable provider of liquid natural gas. Iran can cut them off any time it chooses.

The US oil and gas sector, all of a sudden, become really, really important. Solar and wind energy didn't help at all in this war.

Exhibit A: Hungary will buy more oil from the US going forward. Link here.

Exhibit A: India, Venezuela. It's not as if Venezuela doesn't exist. Link here.

Twelve: coal is dead. Long live coal.

Thirteen: a sorry state of affairs, to be sure -- the US Congress and the mainstream media.

Fourteen: say what you want, but it's now pax Americana in the Mideast, the Persian Gulf is Trump's Lake, and the new normal: the US is in charge.

Fifteen: the firing of US Army Chief of Staff, four-star general Randy George was exactly the right thing to do. Exactly the right thing to do.

The US Secretary of War is not there to make The New York Times editors happy; he's there, among other things, to support the men and women in the trenches and those in helicopters flying into, literally, the jaws of death. What our helicopter crews did in rescuing those airmen was incredible. You don't show your respect for those crews by suspending their fellow airmen for an inconsequential action. Randy might still have his job had he said, at the right time, "enough is enough."

Some questions:

- why did the Houthis not get involved?

- why did North Korea not take advantage of the situation?

- even more so, why did China not take advantage of the situation? This may be the most interesting question to consider going forward when the Taiwan question comes up (again, and again, and again).

- to what extent will the GCC re-build / enlarge / modernize their own bases to accommodate the US?

- talk about lack of statesmen in the GCC. Quick: did Prince MBS ever say anything to the American public? That's really not a question, just an observation.