Locator: 50553FORD.

Meanwhile, last month's sales:

Locator: 50551AI.

Notes on this book are kept here.

If you can read at college level, which generally means the ability to read at some level of the average high school junior, you should be able to slog your way through Anil Aanthasway's book even if you know no mathematics beyond your middle school years.

The narrative was excellent. Very, very easy to read, though as one gets deeper and deeper into the book, the jargon becomes as difficult as the math.

Even so, one can learn much about AI, certainly more than where you started. It's very similar to putting up a Christmas tree, and gradually adding ornaments. Or, similarly, putting up scaffolding to build a complex structure, like, say, the Egyptian pyramids.

Keeping with the Christmas tree ornaments analogy, which is a much better analogy than the pyramid scaffolding, you can keep adding ornaments as you read additional newspaper articles, magazine essays, and books on the subject. Without question, the best ornaments will be added after you spend evening dinners and/or cocktail hours with AI engineers at any level. The jargon alone is worth the price of admission.

And Ananthaswamy's book is a great introduction to AI jargon.

The math was way beyond anything I could follow. But one can scan through those pages. I don't think you want to literally skip any page with math on it because in between the formulas there is likely to be some jargon, some explanation, some context.

Names of pioneers in this field and the universities and countries from which they come were some of the best Christmas tree ornaments. You could, for example, put Geoffrey Hinton at the top of the tree. A lot of those pioneers at age 17 a few years ago are now CEOs or chief engineers at famous AI corporations and making more money than I ever made and will have more impact on humanity than I ever will.

What we now know about what we don't know about AI is absolutely fascinating. Some say scary. Luddites will ban AI from their homes.

The anecdotes about what AI engineers are learning is absolutely fascinating. The best analogy is our discovery and/or [lack of] understanding of quantum theory with the "breakthrough" in 1925 - 1926. One needs to read Richard Feynman's supposed quote on one's understanding of quantum mechanics. But despite that, researchers pressed on. It was a dual track: theorists thinking while smoking pipes and laboratory physicists screwing clamps to their laboratory desks. We are the same spot with regard to AI.

There are two schools of thought: some feel the theory must be worked out before we press on with AI (that won't happen). Others feel that regardless of the theories, we must keep pressing on. Obviously, we will do both.

At the end of the book, I can say this is best I've read on the subject so far. It is a great jumping off point for me. It becomes a reference book to re-read.

Locator: 50550SAFARI.

Like night and day.

My old M1 MacBook Air was released in 2020 and works perfectly.

I've only switched to Safari recently; prior I was almost solely invested in Firefox. But, wow, Safari now seems two, maybe three times faster than Firefox, and very, very "smooth," compared to the relative slowness and "chunkiness" of the Firefox browser.

Not sure what's going on but it's very, very noticeable.

AI prompt:

MacBook Air M1. Have used it since 2000. Almost 100% with Firefox Browser but recently I've noticed Safari browser so much faster and so much smoother. It is my imagination or has Apple's Safari browser gotten significantly faster? My M1 now feels as fast as my wife's M4.

Wow, wow, wow. Look at this.

AI reply:

I think I will blog all night just to experience the new feeling.

My hunch: when Google Gemini is fully integrated into Apple's Siri it's simply going to be amazing.

Locator: 50549APPLEMACNEO.

Locator: 50547BLUESKY.

********************

The Food Product Page

*************************

The Restaurant Page

The AI prompt: Perry's Steakhouse. Dallas North Texas Grapevine.

I was quite negatively impressed when I ordered seared scallops over pasta, the main course, for lunch today. There were three scallops in the dish and each scallop was barely a quarter in diameter, literally the smallest I've seen in any such restaurant. Has Perry's always served such few and so small scallops in that dish?

Chatbot reply:

As an aside, my wife, without any prompting noted that I finished less than half the pasta before turning it back. She stated she noted that on all the other scallop dishes ordered by others, were also less than half finished.

But yes, the signature Perry's pork chop was huge and looked incredible. I just wanted to try something different, so I tried the scallops. Simply an observation.

*******************************

The Music Page

Locator: 50546CHEVRON.

This oil company may be the biggest winner in the war with Iran, but clearly the country that is the biggest winner in this war? The United States.

Locator: 50545B.

Global coal tanking:

NASDAQ: longest winning streak since 2009.

****************************

Back to the Bakken

WTI: $94.69. Whoo-hoo! CVX was up almost 2% today. PSX, same. COP, up almost 3%.

Active rigs: estimate -- 19.

No new permits today. Two older permits with sites modified:

Twelve permits renewed:

One permit cancelled:

Locator: 50544B.

US markets: pull back slightly after S&P 500 hits all-time record yesterday.

Mideast: it still boggles my mind that folks who should know better --

Iran peace deal: won't give up (on) Hezbollah. See previous bullets (no pun intended).

*******************************

Back to the Bakken

WTI: $93.04. Oil traders must have been spooked by DOD's press conference this morning.

New wells reporting:

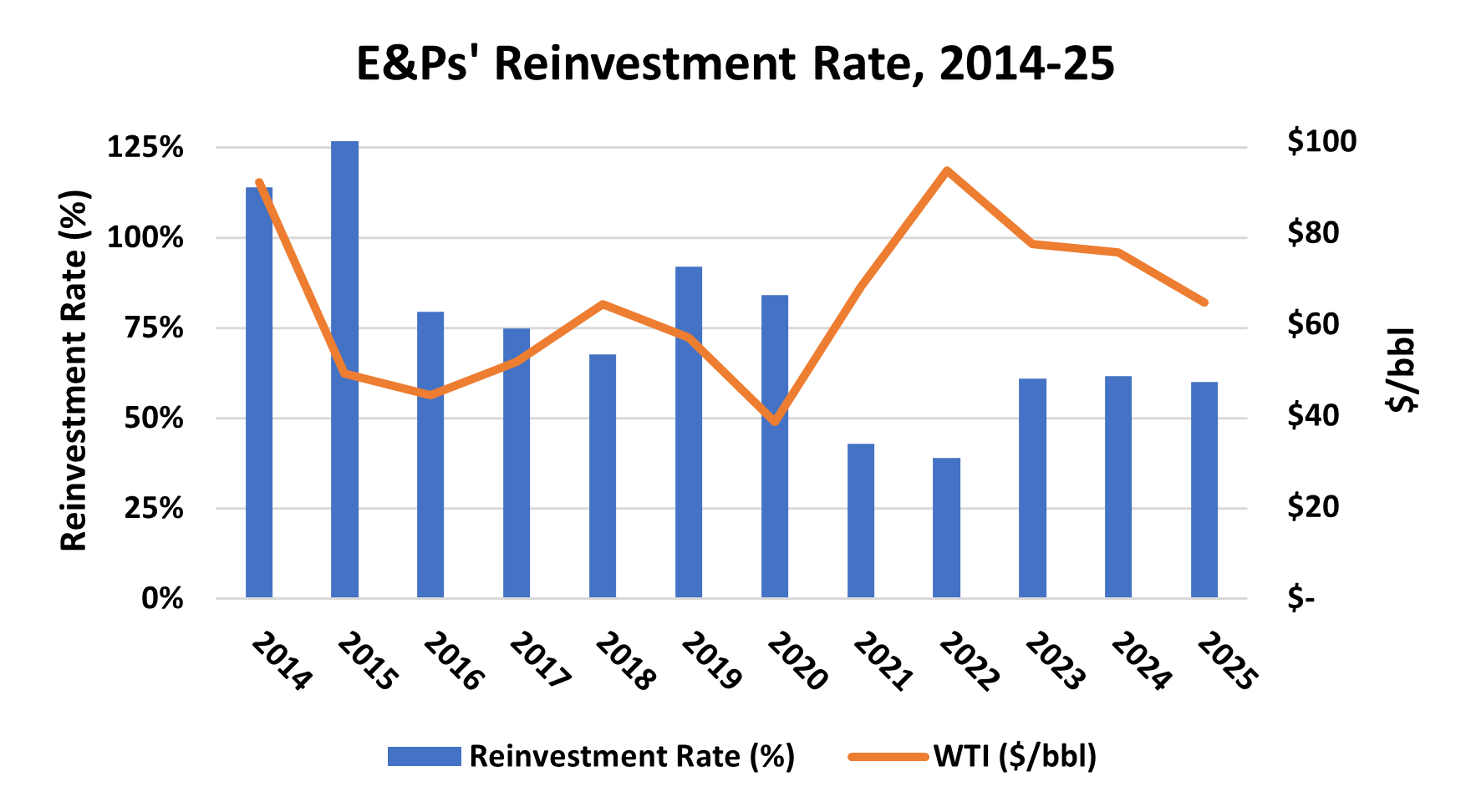

RBN Energy: Will Surging Cash Flows Tempt Still-Disciplined E&Ps to Ramp up Spending? Link here. RBN Energy. Archived.

Weak Q4 2025 results provided a timely check-in on how upstream E&Ps were allocating capital in a lower-price environment — just before a sudden commodity price tailwind in 2026 from the onset of Middle East hostilities. Managements have said they would stick to the capital discipline that won back the hearts and wallets of investors; however, surging oil and gas prices this year are putting more cash back into E&P coffers. In today’s RBN blog, we analyze the Q4 2025 cash allocation of U.S. E&Ps and address the question: Will discipline hold, or will temptation take over?

Across our universe of 35 companies, cash flow from operating activities (CFOA) declined 12% in Q4 2025 from the previous quarter to $24.7 billion, reflecting weaker oil prices. Despite that pressure, capital allocation priorities remained largely intact. Capital spending fell modestly to $15.3 billion, or approximately 62% of cash flow, preserving a reinvestment framework that has become increasingly embedded across the sector over the past several years.

The resulting $9.4 billion of free cash flow (FCF) — while down from the prior quarter — continued to be deployed in a balanced manner. Companies shifted toward net asset sales, generating $1.8 billion of net proceeds, while also resuming debt-reduction efforts with $2.2 billion of net repayments. Shareholder returns remained a core priority, with dividends and share repurchases accounting for 11% and 15% of CFOA, respectively, underscoring the durability of return-of-capital frameworks even in a softer pricing environment. These trends were broadly consistent across our Oil-Weighted, Diversified and Gas-Weighted peer groups, highlighting just how ingrained this capital discipline has become.

Taken together, Q4 2025 reinforced a broader structural shift in the industry — away from growth-at-all-costs and toward a more measured, cash-return-focused model. That evolution is illustrated clearly in Figure 1 below, which shows how reinvestment rates (blue bars and left axis) have converged over time to a rough 60% of cash flow, with the balance directed toward debt reduction, shareholder returns and opportunistic transactions. Even as commodity prices softened in recent years, companies resisted the urge to chase volumes, instead scaling back capital spending to preserve this framework.

Figure 1. E&Ps’ Reinvestment Rate, 2014-25.

Source: Oil & Gas Financial Analytics LLC