LA curfew: ordered by LA mayor on the evening of June 10, 2025; just hours before she and the governor both downplayed the "mostly peaceful" riots and protests. When government / elected officials start declaring curfews that is not a sign that things are getting better. As best I can tell, the area of Los Angeles circumscribed in red is the area of curfew for the evening-night-early morning (8:00 p.m. to 6:00 a.m.), Tuesday, June 10, 2025, to Wednesday, June 11, 2025:

California troop deployment: Federal judge denies Newsom request to shut it down.

Trumps tariffs: can remain in effect while process in lower courts play itself out. Links everywhere.

Terry Moran: ABC contract not renewed.

Tesla robotaxi rides to commence: tentatively, June 22, 2025, Austin, TX.

Meta's Zuckerberg frustrated at pace of his company's AI initiatives. Link here.

Disney: Bob Iger may have found the secret sauce -- keep both -- linear TV as well as streaming "network."

Trump has receipts to show he called Newsom -- a phone call which Newsom denied. Liar, liar, pants on fire. For some, literally.

Indicted for allegedly obstructing Homeland Security agents: Rep. LaMonica McIver (D-NJ) hit with federal indictment by US Attorney Alina Habba. Three-count indictment; felony; if guilty could include prison sentence.

“No

sane project developer is going to start producing hydrogen without

having a buyer for it, and no sane banker is going to lend money to a

project developer without reasonable confidence that someone’s going to

buy the hydrogen,” BNEF analyst Martin Tengler notes.

“It’s no different than any other energy development at scale. Natural gas pipelines didn’t get built without customers,” says Laura Luce, chief executive officer of Hy Stor Energy.

Meanwhile, Trump’s “Big, Beautiful Bill” could have dire consequences

for the hydrogen sector if it becomes law. The sweeping policy bill

will do away with billions in tax credits provided by Biden’s Inflation

Reduction Act (IRA), with Section 45V tax credit considered a major boon

for low-carbon hydrogen and ammonia projects across the country. Losing

45V tax credits may seriously erode the economic viability of dozens of

companies including Plug Power (NASDAQ:PLUG), Air Products & Chemicals (NYSE:APD), CF Industries (NYSE:CF), Bia Energy, Clean Hydrogen Works and Monarch Energy.

SPR refill: all that nonsense chatter (today) about refilling the Strategic Petroleum Reserve is simply that. Nonsense. This works in Trump's favor, of course, with goal to keep oil prices / gasoline prices low.

ABC won't renew Terry Moran's contract. Wow.

MIT: finding a solution to a problem that doesn't exist; and producing a product "no one" wants. Producing hydrogen from aluminum cans and seawater.

California: it's beyond me how a state with a $9 trillion industry (Silicon Valley) can be broke.

********************************* Back to the Bakken

WTI: $64.76.

Active rigs: 32.

Seven new permits, #41983 - #41990, inclusive:

Operators: Devon Energy (5); Murfin Drilling (2)

Fields: Tobacco Garden (McKenzie); St Anthony (Dunn County)

Comments:

Murfin Drilling has permits for two LC Rambousek wells, SESE 9-141-97,

to be sited 370 FSL and 365 / 335 FEL;

Devon Energy has permits for five Drovdal wells, lot 4, section 5-150-99,

to be sited 679 / 681 FNL ad 1222 / 1342 FWL; four Drovdal wells will be 1280-acre spacing, sections 5 and 8; one will be 2560-acre spacing, sections 4 / 5 / 8 / 9.

Six permits renewed:

XTO (4): four Twin State Federal permits, Sand Creek, McKenzie County;

Formentera Operations (2): one Bervik permit (Skjermo, Divide County) and one LAR1 permit (Larson, Burke County);

Five permits canceled:

CLR (3): three Chloe permits, Williams County;

Phoenix Operating (2): two TJ E Federal permits, Mountrail County.

Wow, wow, wow! Look at the EIA's forecast for a significant increase in the rate of growth in electricity demand, especially in areas of high AI demand, notably TEXAS and the NORTHEAST:

Last month, EIA forecast electricity demand would increase by 2% each year (year-over-year) for both years 2025 and 2026.

Today, one month later, EIA forecasts:

growth for 2025: 3% (a fifty percent increase in the rate of growth)

growth for 2026: 5% (a more than doubling the increase in the rate of growth next year and that's on top the increased rate of growth this year

Tickers: the oil tickers on the CNBC crawler are absolutely stunning.

CVX: up $4.00; up 2.8%;

PSX: up $3.50 up. 3%;

XOM: up $2.60; up 2.4%;

COP: up $3.40; up 4%;

OXY: up $1.26; up 3%;

HES: up $3.60; up 2.65;

FANG: up $4.57; up 3.2%

XLE (energy select sector SPDR Fund: up $1.60; up 2% today.

and that's why I think there are better ways than investing in ETFs, but ....

The reason is obvious. Let's see if that becomes obvious over the next six weeks or so. Actually two reasons:

China

Iran

Is money moving from tech to oil? Not really, but perhaps to some extent. The story remains geo-political, specifically Ukraine-Russia, but even more so, US-Iran nuclear talks.

NVDA: flat; flat;

TSM: up $4.70; up 2.3%;

AMD: up $1.60; up 1.3%;

INTC: up 1.10; up 5.5%;

AMZN: down 70 cents; down 0.3%;

AAPL: up 41 cents; up 0.2%;:

PLTR: down 55 cents; dow 0.4%;

AVGO: up 48 cents; up 0.2%;

QCOM: up $3.50; up 2.3%;

China EVs: a race to the bottom. CNBC.

cutting prices to the bone means no margins; no profits

"Zero mileage used cars": jargon; google zero mileage used cars;

A growing controversy has emerged in China’s automotive sector over

so-called “zero-kilometre used cars”—vehicles that have been registered

but never driven, now flooding the second-hand market. Industry voices

like Great Wall Motor Chairman

Wei Jianjun are speaking out, and this practice is drawing criticism

for distorting sales data, misleading consumers and undermining

long-term market stability.

inflate sales numbers

price war leads nowhere

Chinese state media calls for crackdown on "zero-mileage used cars"; link to Reuters;

time to get out the popcorn

Mark Fields remains bullish on EVs.

AAPL: something different this time following the WWDC?

Apple's (AAPL) iPad is getting some major enhancements that should make

it a far more useful laptop replacement.

the improvements are part of the company's iPadOS 26, which Apple

announced during its WWDC 2025 conference on Monday. They include

upgraded multitasking capabilities that will allow people to use the

iPad more like a Mac and less like an iPhone.

very, very interesting: many (most?) of the websites I visit seem optimized to mobile devices;

fail on my laptops/desktops; websites have optimized for mobile devices

we're now seeing that in Apple's "response" to the iPad

Reminder:

CNBC producer puts together general agenda two weeks prior to airing; needs time to schedule talking heads for interviews, background, etc

one week before: starts to review agenda, scheduling one week out

two days before: reviews footage; schedule of talking heads; puts out last minute fires (problems, disputes)

day of airing: already two weeks behind; we're seeing that again today

Oil price jump today: CNBC -- if discussed at all, won't be discussed until tomorrow or two weeks from now. Interestingly, ChatGPT not particularly helpful ... at the moment.

What's going on over at x?

first driverless Teslas are now appearing on the roads in Austin; see video at this link;

this explains why Tesla is up over 10% today;

a bigger story: unlike Waymos in Los Angeles, these Teslas are not being set on fire;

recession odds fade;

Duke Energy proposed 1.4-GW gas-fired plant in South Carolina --

remember, AI is an energy story; AI runs on natural gas; nuclear will take time;

"gold miners" are up 35% YTD

Nvidia: after China? What's next? Britain.

Shay: did small-cap summer just kick off? NVTS, ASTS, ACHR, EOSE, RDW.

Bloomberg: White House says this story is false -- "Treasury Secretary Scott Bessent has emerged as a contender to be the next Chair of the Federal Reserve." Probably true.

JPow's term is up May, 2026

nothing on my feed -- nothing -- regarding ICE riots in LA

META to pay $15 billion for 49% stake in ScaleAI; links everywhere; here's The Verge

the start-up's CEO is 28 years old; revenge of the nerds

Apple and AI: what's going on? Tag: AAPL, OpenAI, ChatGPT, choices, options:

tea leaves suggest huge difference of opinion at the top, in the C-suite; three options

pay the dollars to OpenAI and partner with OpenAI, OR,

buy an AI startup and have Apple-owned AI, OR,

start from scratch -- or build on Siri -- and develop AppleAI in-house at great expense, and still come up a dollar short and a day late:

"A dollar short and a day late" is an American idiom meaning that someone has not only missed an opportunity due to tardiness but also because they lack sufficient resources or effort.It implies that their attempt to achieve something is inadequate and too little, too late

Apple really has only one choice --

ChatGPT now and on-device AI as goal --> develop, for security purposes for those folks who are concerned about being tracked.

Siri could remain the on-device AI option for Apple; best of both worlds.

ChatGPT suggests four options:

OpenAI, most likely, ChatGPT

Google, Gemini -- as an alternative or complementary provider

Apple, internal models, for privacy and on-device AI

Anthropic: unconfirmed; less likely currently

***************************** Not On My Radar Scope Either, At Least For Today But We're Still Waiting For The Judge To Respond

When I see this, I come back often to one of my-go-to memes: there's a lot of mom-and-pop retail investors who are afraid of getting really, really rich.

Read the disclaimer.

TSM / TSMC: the big story today. Huge jump in revenue. But a lot of this was the pull-forward effect caused by tariff talk.

Shay, link here, posted for the "ad" effect and social medial replies.

*****************************************

Disclaimer Brief Reminder

Briefly:

I

am inappropriately exuberant about the Bakken and I am often well out

front of my headlights. I am often appropriately accused of hyperbole

when it comes to the Bakken.

I am inappropriately exuberant about the US economy and the US market.

I am also inappropriately exuberant about all things Apple.

See disclaimer. This is not an investment site.

Disclaimer:

this is not an investment site. Do not make any investment, financial,

job, career, travel, or relationship decisions based on what you read

here or think you may have read here. All my posts are done quickly:

there will be content and typographical errors. If something appears

wrong, it probably is. Feel free to fact check everything.

If

anything on any of my posts is important to you, go to the source.

If/when I find typographical / content errors, I will correct them.

Reminder: I am inappropriately exuberant about the Bakken, US economy, and the US market.

I am also inappropriately exuberant about all things Apple.

And

now, Nvidia, also. I am also inappropriately exuberant about all things

Nvidia. Nvidia is a metonym for AI and/or the sixth industrial

revolution.

I've now added Broadcom to the disclaimer. I am also inappropriately exuberant about all things Broadcom.

I've now added Oracle to the disclaimer. I am also inappropriately exuberant about all things Oracle.

June 12, 2025: cash burn search today revealed this --

Original Post

GDPNow: 3.8%, unchanged from previous estimate.

TSM / TSMC: the big story today. Huge jump in revenue. But a lot of this was the pull-forward effect caused by tariff talk.

Germany: Nvidia and HPE to build new supercomputer in Germany. Link here.

Blue Lion supercomputer

to be online in early 2027

will use Nvidia's "Vera Rubin" chips

Narrative from previous link:

The announcement, made at a supercomputing

conference in Hamburg, Germany, follows Nvidia's announcement that the

Lawrence Berkeley National Lab in the United States also plans to build a

system using the chips next year.

Separately,

Nvidia also said that Jupiter, another supercomputer using its chips at

German national research institute Forschungszentrum Julich, has

officially become Europe's fastest system.

The

deals represent European institutions aiming to stay competitive

against the U.S. in supercomputers used for scientific fields from

biotechnology to climate research.

There’s been a surge in E&P interest in the Utica Shale’s volatile

oil window the past couple of years, and EOG Resources has been

particularly optimistic about its potential for producing large volumes

of condensate, the lightest of superlight crude oils. A few days ago,

EOG — known for growing its business organically, not via M&A —

announced one of the largest acquisitions of the year so far: the

planned purchase of Encino Acquisition Partners (EAP), the Utica’s #1

condensate producer by far, for $5.6 billion, including the assumption

of EAP’s debt. As we discuss in today’s RBN blog, the deal will give EOG

its third “foundational” focus area (the others are the Eagle Ford and

the Permian's Delaware Basin) and supports the view that the Utica

really is an up-and-comer.

And then there's this, link here, be sure to listen to the back-up vocalist:

California: best news so far today. Unless you're looking for it, there are not headlines on ICE-riots in California. Speaks volumes.

****************************** More At The Bakken

WTI: $65.57.

New wells:

Wednesday, June 11, 2025: 38 for the month, 191 for the quarter, 405 for the year,

41119, conf, Oasis, Sawtooth 5202 24-20 5B,

41011, conf, Oasis, Sawtooth 5202 24-20 4B,

40606, conf, Enerplus, Danielle 145-97-12-1-4H,

40605, conf, Enerplus, Danielle 145-97-12-1-5H,

Tuesday, June 10, 2025: 34 for the month, 187 for the quarter, 401 for the year,

41118, conf, Oasis, Sawtooth 5202 24-20 3B,

41178, conf, CLR, Helen 5-8H,

Enerplus Danielle wells: tracked here. Too early for much new data.

Marcellus/Utica natural gas production grew by leaps and bounds in the

2010s, but the pace of growth has slowed dramatically in recent years,

mostly due to takeaway constraints. Finally, the prospects for renewed

growth are improving. New pipeline capacity out of Appalachia is coming

online — especially to the booming Southeast, and maybe the Gulf Coast

too. New LNG export capacity is about to be commercialized. And a lot of

new gas-fired generating capacity — much of it tied to planned data

centers — is under development within (or very near) the Marcellus/Utica

region. In today’s RBN blog, we examine the three big gas-demand

drivers behind the shale play’s impending renewal.

As we said in Part 1,

the Marcellus/Utica is by far the most prolific gas production area in

the U.S., accounting for about one-third of the nation’s daily output.

The shale play’s gas production soared from less than 2 Bcf/d to more

than 33 Bcf/d over that decade, but its output through the first half of

the 2020s has stayed close to flat, averaging about 35 Bcf/d over that

period — ~24 Bcf/d from the NGL-rich “wet Marcellus/Utica” in

southwestern Pennsylvania, northern West Virginia and eastern Ohio and

~11 Bcf/d from the “dry Marcellus” in northeastern Pennsylvania.

The primary hurdle to further growth has been takeaway capacity;

there hasn’t been enough space on pipelines out of Appalachia to move

more of the shale play’s gas to demand centers hundreds of miles away.

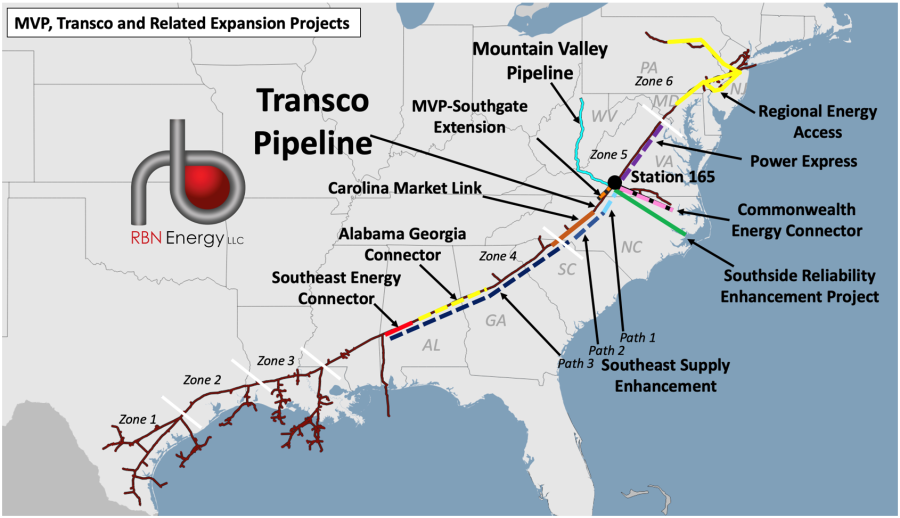

That’s been changing, however, mostly due to the June 2024 startup of

the 2-Bcf/d Mountain Valley Pipeline (MVP; aqua line in Figure 1 below)

from northern West Virginia to Transco Station 165 in south-central

Virginia and the advancement of several capacity-expansion projects on

or near Transco itself. A few of these projects (Regional Energy Access,

Southside Reliability Enhancement Project, Carolina Market Link, and

Southeast Energy Connector) came online over the past 18 months, and

others (Commonwealth Energy Connector, MVP Southgate, Southeast Supply

Enhancement, and Alabama Georgia Connector) will follow later this year

and in 2027-28. (See Part 1 for details.)

Figure 1. MVP, Transco and Related Expansion Projects. Source: RBN