Locator: 48754TECH.

Poolside: not much blogging today. Book for the day: Red Brick Black Mountain White Clay, Christopher Benfey, c. 2012 / Penguin 2013.

Not on my radar scope: oil down and pre-market way up.

AMD; at open, up 10%.

Boeing Dreamliner 787 crash in India. Three YouTube videos suggesting the immediate cause. On what we know, the "theory" makes sense. Search most recent Garybpilot and Captain Steeeve (sic). Tea leaves: authorities already know what happened, just not how or why. We know it wasn’t a mechanical issue / design flaw.

**************************************

Back to the Bakken

WTI: $71.54. Down significantly overnight.

New wells:

Tuesday, June 17, 202: 46 for the month, 199 for the quarter, 413 for the year,

Monday, June 16, 2025: 46 for the month, 199 for the quarter, 413 for the year,

- 41285, conf, CLR, Chloe 66-20H,

Sunday, June 15, 2025: 45 for the month, 198 for the quarter, 412 for the year,

- 40603, conf, Enerplus Resources, Danielle 145-97-12-1-8H,

Saturday, June 14, 2025: 44 for the month, 197 for the quarter, 411 for the year,

RBN Energy: EU's efforts to end reliance on Russian natural gas could boost US LNG exports.

The European Union (EU) has had to rethink and reconfigure major

elements of its policies around natural gas since Russia’s invasion of

Ukraine in February 2022. Prior to the war, Russian volumes accounted

for 45% of the EU’s imports of natural gas, nearly double the supply

from second-place Norway, but Russian gas supplies have dropped

considerably since then, impacting the global LNG market. In today’s RBN

blog, we look at the EU’s continued efforts to reduce its reliance on

Russia, how it’s trading supply risk for price risk, and what the

changes could mean for U.S. LNG exporters.

Just

a few years ago, Russia was annually exporting 150 billion cubic meters

(Bcm; 14.5 Bcf/d) of natural gas to Europe, including pipeline gas and

LNG. But volumes have declined sharply, first due to the damage

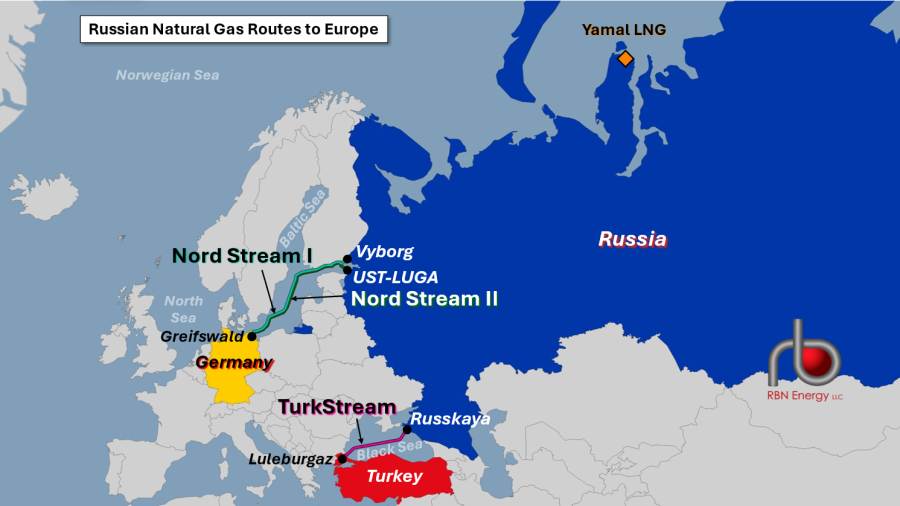

inflicted on the offshore Nord Stream pipelines (twin green lines in

Figure 1 below) that connect Russia and Germany and second from the

termination (at the end of 2024) of the last agreement to move Russian

gas through Ukraine via pipeline to other parts of Europe. (Most of the

Nord Stream system under the Baltic Sea was destroyed in a September

2022 explosion. Nord Stream 1 began service in 2011; Nord Stream 2 was

completed in 2021 but never entered service.) Russian pipeline gas

supplies to Europe are now limited to volumes imported via the

TurkStream gas pipeline (pink line), which runs under the Black Sea and

connects in Turkey, which delivered 16.7 Bcm (1.6 Bcf/d) to European

customers in 2024, notably to Hungary (7.6 Bcm; 0.7 Bcf/d).

Figure 1. Russian Natural Gas Routes to Europe. Source: RBN

In contrast, Russian LNG derived from Novatek’s Yamal project (orange

diamond at top of Figure 1) and three small facilities located in the

Baltic Sea has not been as heavily impacted by political events. EU

imports of Russian LNG rose by 18% from 2023 to 24.2 Bcm (2.3 Bcf/d) in

2024. This occurred despite the EU having previously imposed 16

different sets of sanctions on Russian energy supplies. (More on the

impact of the 17th in a bit.) The cost of this gas was 21.9 billion

euros ($24.9 billion), which exceeded the 18.7 billion euros ($21.2

billion) in financial aid the EU sent to Ukraine in the same year. By

purchasing Russian gas, the EU has essentially been helping Russia

finance its war with Ukraine.