Locator: 51036B.

Micron Technology (MU): will report its fiscal third-quarter results for 2026 on Wednesday, June 24, after the market closes. Management has provided preliminary guidance of record revenue around $33.5 billion and adjusted earnings of $19.15 per share, with the company's high-bandwidth memory (HBM) supply for the year completely sold out.

Micron Technology (MU): BofA raises MU price target to $1,500 vs $950. Wow, from $950 to. $1,500 is not trivial.

IBM bucks today's trend: up 4.4% pre-market; much of rest of tech falls significantly.

***************************

Back to the Bakken

WTI: $73.51. Lowest level in past three months. Best gasoline price in local area (north Texas, DFW, $3.04 at local Walmart).

New wells reporting:

- Wednesday, June 24, 2026: 28 for the month, 184 for the quarter, 341 for the year,

- 41607, conf, Hess, BL-Mortenson-156-95-2234H-5,

- Tuesday, June 23, 2026: 27 for the month, 183 for the quarter, 340 for the year,

- 41682, conf, Devon Energy, Johnson 27-34 8H,

RBN Energy: plans to move more Marcellus / Utica gas to the midwest, mid-south, and deep south. Link here. Archived.

Midwestern states like Ohio, Indiana, Illinois and Michigan are important markets for natural gas producers in the Marcellus/Utica, as are states in the Mid-South like Kentucky and Tennessee and states in the Deep South. But expanding gas sales in those markets will require a lot more pipeline capacity, and that’s exactly what’s in the works. In today’s RBN blog, we continue our look at the pipeline projects being planned to move more Appalachia-sourced gas within — and out of — the U.S.’s largest gas production region.

This is Part 5 of our blog series on gas market dynamics in the Northeast. In Part 1, we said the Appalachia market has been quietly evolving in ways that will not only shift flow patterns within the region but also affect flows to the Southeast, Midwest and Gulf Coast. Part 2 focused on gas demand within the Northeast, which is getting a big boost from the power-generation sector as coal retirements continue and data center development proliferates. In Part 3, we started a review of the pipeline projects planned to enable more gas to flow through and out of the Marcellus/Utica, focusing on projects in New England and New York. Part 4 continued that review with a look at projects within Pennsylvania; regionwide enhancements like TC Energy’s Appalachian Supply Project; and projects involving or tied to either the Mountain Valley Pipeline or Williams’s Transco system.

Today, we wrap up the pipeline projects part of our series with an analysis of (1) projects that will provide expanded capacity to eastern Ohio and beyond and (2) projects that are more distant but still related to the Marcellus/Utica.

Expanded capacity to Ohio and beyond

There already are several major pipelines that transport Appalachian gas west. These include the bidirectional, Tallgrass Energy-operated Rockies Express (REX), which can move up to 2.6 Bcf/d westward; Enbridge’s sprawling Texas Eastern Transmission Co. (TETCO), and TC Energy’s ANR Pipeline system. (The ANR system is being expanded to support new data centers and related power projects in the Upper Midwest — more on that later) and two big greenfield pipelines that started up in 2018: Energy Transfer and Ares Management’s 3.425-Bcf/d Rover Pipeline and Enbridge’s 1.4-Bcf/d NEXUS Pipeline.

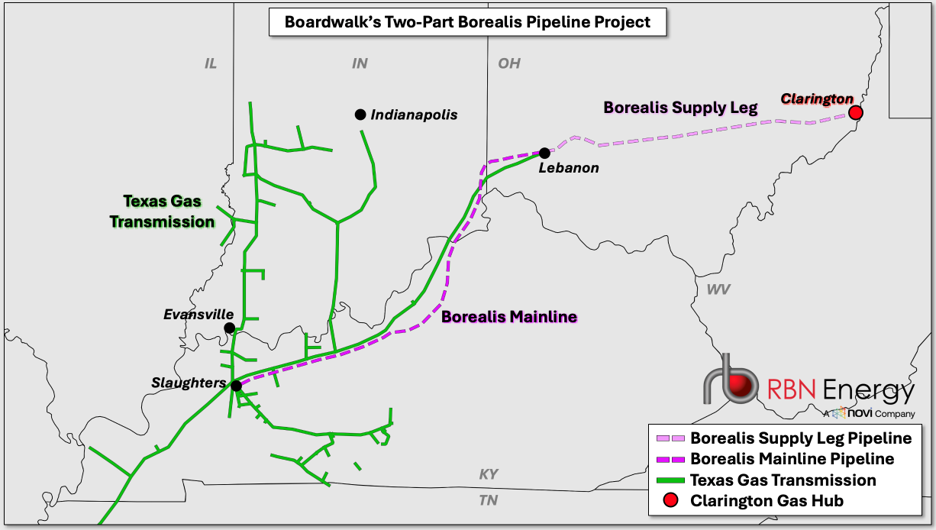

As massive as these pipelines may be, rising gas demand means that still more westbound capacity into, through and out of Ohio will be needed over the next few years. Among the largest development efforts is Boardwalk Pipelines’ two-part Borealis Pipeline Project, which will enable an incremental 2 Bcf/d to be transported west across Ohio and an incremental 1.75 Bcf/d to move into southeastern Indiana and northern and western Kentucky. (Boardwalk is a subsidiary of Loews Corp.)

Figure 1. Boardwalk’s Two-Part Borealis Pipeline Project. Source: Novi Labs