Monday -- Trump To Hegseth -- "Hold Your Fire" -- March 23, 2026

Locator: 50299B.

************************************** Back to the Bakken

WTI: $89.58 -- down almost 9% after Trump offers olive branch. Down $8.60.

New wells reporting:

Tuesday, March 24, 2026: 33 for the month, 137 for the quarter, 137 for the year,

41193, conf, Devon Energy, Eide 6-7 8H,

Monday, March 23, 2026: 32 for the month, 136 for the quarter, 136 for the year,

42241, conf, CLR, Addyson 6-14H,

41367, conf, Hunt Oil, State C 156-90-4-36H-2,

41366, conf, Hunt Oil, State A 156-90-9-16H-4,

20716, conf, Devon Energy, Marvin 27-34 1H,

Sunday, March 22, 2026: 28 for the month, 132 for the quarter, 132 for the year,

None.

Saturday, March 21, 2026: 28 for the month, 132 for the quarter, 132 for the year,

42248, conf, CLR, Olympia 6-27HSL,

42097, conf, BR, RollaKellog 61-ULW

RBN Energy: plans for Venezuelan revival might not include its long-eglected refining sector. Link here. Archived.

The

U.S. and Israeli military strikes against Iran and the unsettled

situation in the Middle East have pushed many topics to the background

for now. But the energy-related impacts from the U.S.’s decision to

remove Venezuelan President Nicolás Maduro from power early this year is

one topic that won’t stay in the shadows for long. Venezuela, estimated

to have the world’s largest crude oil reserves, was also a major

refiner that exported products across the Western Hemisphere before it

began a decadelong downturn. In today’s RBN blog, we look at the history

of Venezuela’s refining sector, where things stand today, and the

prospects for a turnaround.

We have written

extensively about the developments in Venezuela over the past several

weeks, with our analysis so far focused on crude oil production and

other upstream issues. In Take Me Money and Run Venezuela,

we began by detailing how the country was once a critical supplier of

heavy sour crude to U.S. Gulf Coast refineries, providing more than 1

MMb/d in the late 1990s and early 2000s before Venezuelan production

entered a long period of decline soon after Maduro’s predecessor, Hugo

Chávez, came into power in late 1999. Today, the country produces less

than 1 MMb/d of crude oil — barely one-quarter of the level it reached

in the late 1990s.

After

our initial blog, we looked more closely at the type of crude Venezuela

produces and the potential impact of more barrels hitting the global

market. In Orinoco Flow,

we said that most of Venezuela’s crude oil reserves are located within

the 21,000-square-mile Orinoco Belt, which produces a crude that is

extra-heavy (an API as low as 8-14 degrees), so thick that it’s

difficult to transport and refine. In When Love Comes to Town,

we looked at the differences in Venezuelan and Canadian heavy crudes,

including production methods, costs and quality, and how a revival in

Venezuelan production could impact the flows and prices of Canadian

barrels. (As noted in our weekly Crude Billboard report, the U.S. imported 423 Mb/d of Venezuelan crude in the week ended March 13, the highest since December 2024.) We capped that series with Round and Round,

where we detailed the concrete steps Venezuela could take to boost

crude production in the short, medium and long term. (That analysis was

included in our first Drill Down Report of 2026, which is available here.)

Today’s

blog begins a new series on Venezuela, this one focused on its refining

sector, export capabilities and turnaround potential. Just as we did in

our initial series, let’s start with some background.

Venezuela

built up the largest refining industry in Latin America during the

post-WW2 era and retained that position until Brazil (a country with

four times as much fuel demand) passed it in 1980, but it remained a

major regional product exporter in the Caribbean (including exports to

the U.S.) until well into the Chávez years. Venezuela is home to five

refineries — including the Paraguaná Refining Complex, what was once the

largest single-site refining facility in the world and remains the

second largest by rated capacity — all of which have operated far below

their full capacity in recent years.

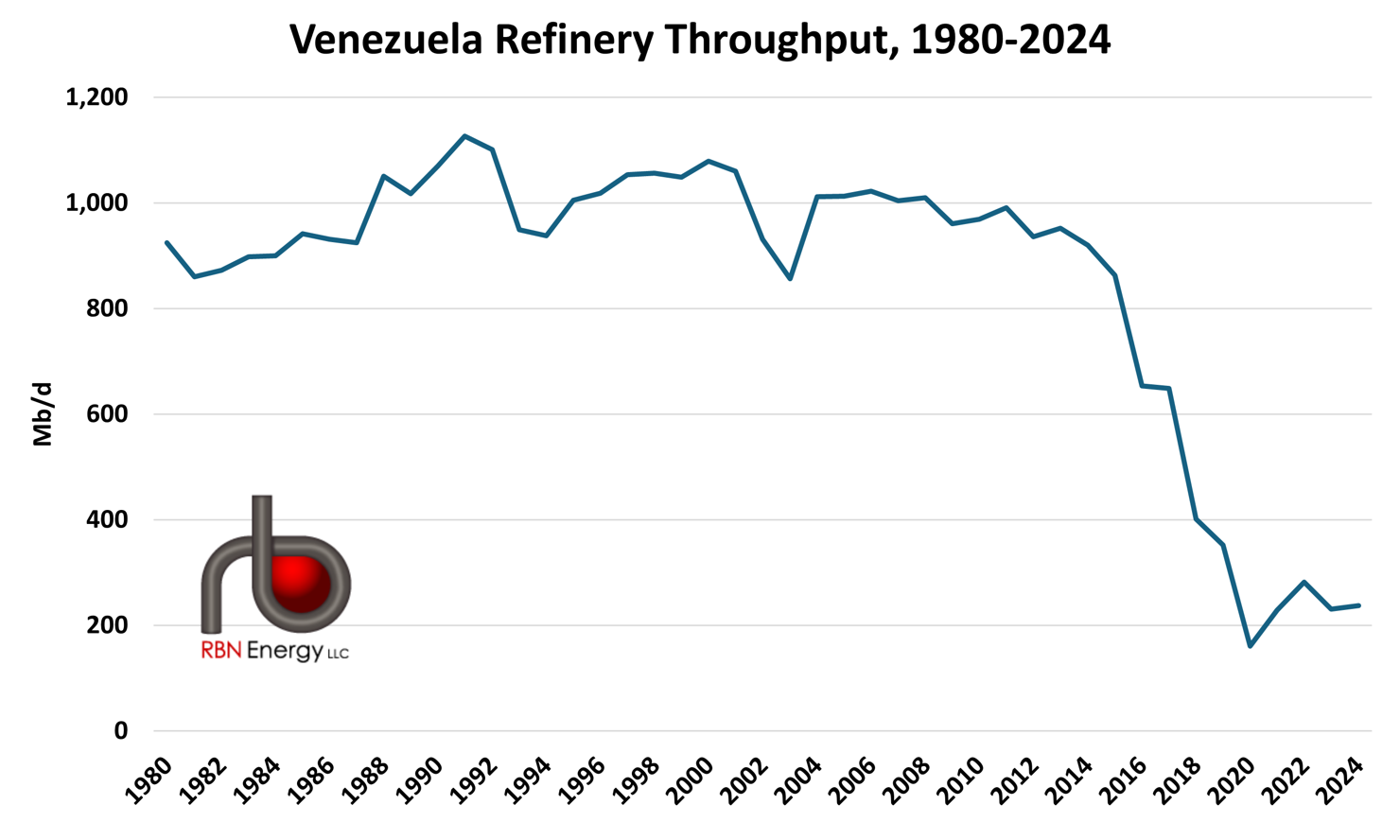

Back in the

sector’s heyday, before Chávez came to power, Venezuelan refinery

throughput (see Figure 1 below) was consistently around 1 MMb/d (with

utilization rates in the mid-1980s). With its refineries operating at

high rates, Venezuela emerged as a major source of refined products,

with the U.S. and other Western Hemisphere countries becoming consistent

importers of Venezuelan gasoline, middle distillates and other products

(particularly fuel oil and asphalt). The performance of Venezuela’s

refineries showed a noticeable dip in 2002 and 2003, around the time of a

major strike against state-run PDVSA, but throughput mostly held steady

until the early 2010s, when a sharp decline began.

Figure 1. Venezuela Refinery Throughput, 1980-2024. Source: 2025 Energy Institute Statistical Review of World Energy