Locator: 50905B.

Bull run: now, nine weeks long -- since March, 1950, this bull run of 9 weeks ranks #16 -- CNBC. Only #16?

NBA: game 1 tonight.

Elizabeth Warren: missed the AI revolution.

15 minutes of fame: Scott Pelley fired by CBS. I don't think I've watched 60 Minutes in the last decade but apparently Scott Pelley is the Big Man on Campus over at CBS News.

Pageviews: since the beginning -- June 3, 2026, 7:36 a.m.: 59,949,501. By the end of the month, we should have 60 million pageviews total since the blog began. Now, June 5, 2026, 5:00 a.m.: 60, 073,897:

- delta: 124,306 over almost exactly two days

- per day: 62,153

- this seems somewhat impossible; I will have to check some additional calculations later.

Later, 4:23 a.m. Saturday, June 6, not quite 24 hours later, pageviews:

- right now: 60,132,667

- not quite 24 hours ago, June 5, 2026, 5:00 a.m., yesterday: 60,073,897

- in that 24-hour period: 58,770 page views.

This site is not monetized -- none of my blog sites are monetize.

With regard to page views (pageviews), google gemini has incorrect information. I provided google gemini with the correct information and gemini confirmed it with data from mineralrightsforum.com. Thank you. I didn't check that link; I have no idea if it works from this end. I do believe this site is the only site dedicated to the Bakken that requires no password, no subscription, no e-mail requirement, and is not monetized.

*******************************************

Back to the Bakken

WTI: $95.66. Up $1.90; up 2%.

New wells reporting:

Thursday, June 4, 2026: 2 for the month, 158 for the quarter, 315 for the year,

42003, conf, Slawson, Cannonball Federal 6-27-34H,

Wednesday, June 3, 2026: 1 for the month, 157 for the quarter, 314 for the year,

None.

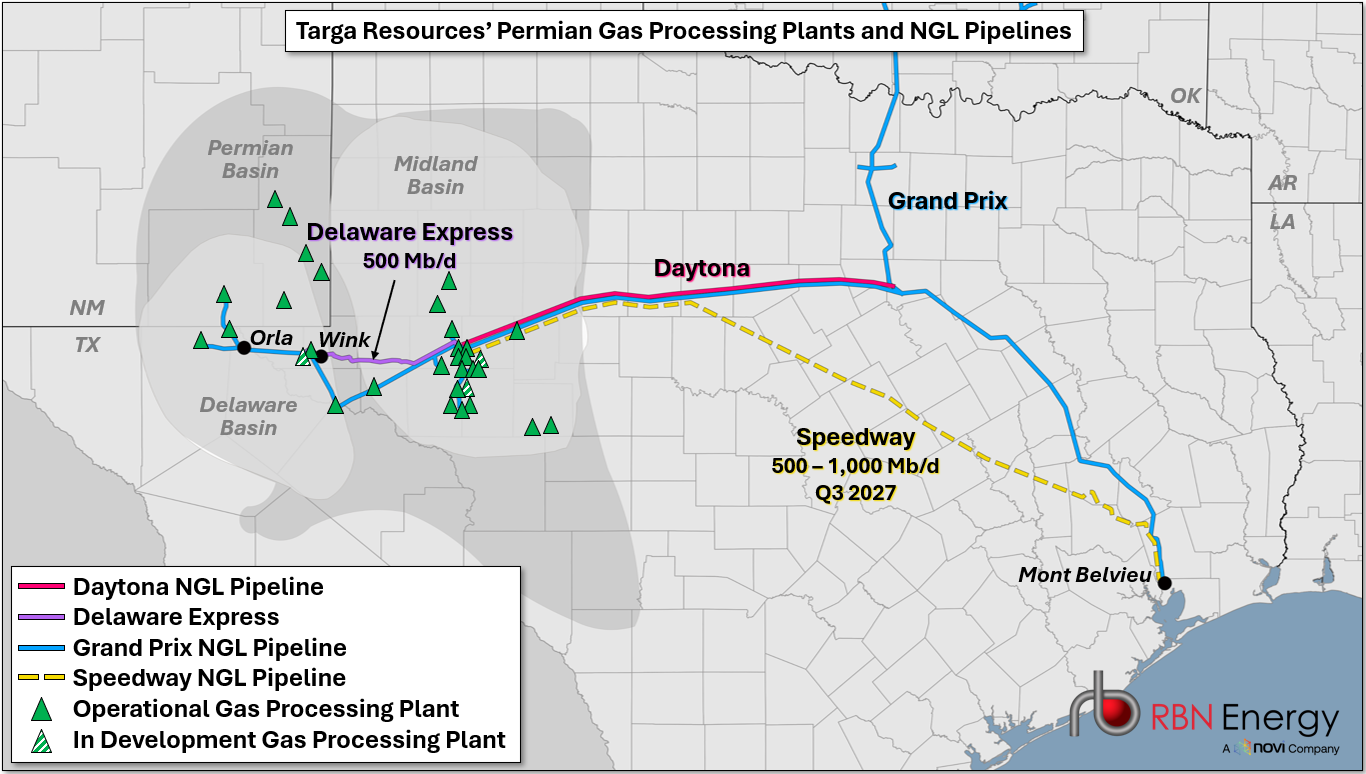

RBN Energy: Permian's rising NGL output spurs another round of "wellhead-to-water projects. Link here. Archived.

The

rapid buildout of Permian gas processing plants and other NGL-related

infrastructure in Texas and southeastern New Mexico isn’t just

continuing, it’s accelerating. Not just processing, but also new and

expanded NGL pipelines, new fractionators in Mont Belvieu (and near

Corpus Christi), and new ethane and LPG export capacity. Funny thing is,

all that growth and investment is happening as crude oil-focused

production in the Permian has remained flat as a pancake. In today’s RBN

blog, we discuss the latest project announcements and why associated

gas and NGL production in the Permian are still rising.

Crude

oil prices have been elevated for three months now thanks to the Iran

war, but Permian producers have resisted the temptation to ratchet up

their drilling-and-completion activity. In fact, the Permian rig count

is virtually unchanged from the end of last year (247 then vs. 246 as of

mid-May) and so is basin oil production, at 6.6 MMb/d, according to our

weekly Crude Oil Permian

report. That extraordinary discipline during an extended period of WTI

prices north of $90/bbl raises an important, two-part question for folks

who focus on the NGL side of things: If Permian crude oil production

isn’t rising in this price environment, has oil output there pretty much

peaked and, if so, what does that mean for the basin’s production of

associated gas and NGLs?

Spoiler alert: Even if

Permian crude oil production stays flat — heck, even if it were to sag

by a few hundred thousand barrels a day — the basin’s output of

associated gas and NGLs will continue to increase, and at a pretty good

clip. (And that’s impacting the market for NGL purity products like

propane — see our recent Wind of Change blog.) As we explained a few months ago in Hold On ... I’m Coming,

the mix of crude, natural gas and NGLs emerging from Permian wells has

been evolving for many years now, with the general trends being (1) more

gas per barrel of oil (that is, a higher gas-to-oil ratio, or GOR) and

(2) more NGLs per thousand cubic feet of gas (that is, a higher

gallons-per-Mcf, or GPM).

The shift toward gassier,

more-NGL-packed production in the Permian has been significant. By our

estimate, the overall basin’s GOR has increased from 3.4:1 in 2014 to

4.4:1 in 2025, a gain of almost 30%, and the Permian’s GPM has risen

from about 4.5 to 5.2. And from everything we’ve seen and heard about

where producers are drilling and what’s emerging from their newer wells,

this ramp-up in GORs and GPMs has been accelerating — and that’s what

we’ve got in our models.

This suggests that, even

under a flat oil production scenario, the Permian’s associated gas and

NGL output will keep climbing into the 2030s. RBN’s mid-case scenario

for the basin, which envisions a gradual rise in crude oil production

into the 2030s and sees dry gas output increasing to 28 Bcf/d in 2030

and NGL output climbing to 4.8 MMb/d. The same analysis predicts that by

2035, Permian dry gas production will rise to 32 Bcf/d and NGL output

will top 5.5 MMb/d, or about 50% of the U.S. total for NGLs.

We

have blogged extensively about the new and expanded natural gas

pipelines out of the Permian (mostly toward the Gulf Coast but also to

the Desert Southwest and maybe the Midcon). But it’s been a while since

we did a roundup on planned additions to the interconnected set of

“wellhead-to-water” assets that process, transport, fractionate, store

and export NGLs. There’s a lot going on, so to keep things simple, we’ll

tackle this company by company, starting with Targa Resources and

Enterprise Products Partners.

Targa Resources is

one of a select few midstream companies with a complete range of

NGL-related assets, everything from gas gathering pipelines and

processing plants in the Permian to NGL takeaway pipelines,

fractionators and NGL storage at Mont Belvieu and NGL export facilities.

Targa has 8.7 Bcf/d of gas processing capacity in the Permian, split

about evenly between the Midland Basin (4.4 Bcf/d) and the Delaware

Basin (4.3 Bcf/d). (Eighteen of its 21 Midland plants are actually owned

by a Targa/ExxonMobil joint venture in which Targa holds a 72.8%

stake.)

During its Q1 2026 earnings call on May 7,

Targa said that it recently started operation of its two newest

processing plants: the 275-MMcf/d Falcon II facility in the Delaware (in

February) and the 275-MMcf/d East Pembrook plant in the Midland (in

late March). Four additional plants, each with a capacity of 275 MMcf/d,

are scheduled to come online by the end of 2027, including the East

Driver plant in the Midland in Q3 2026 and — all in the Delaware —

Copperhead (Q1 2027), Yeti (Q3 2027) and Yeti II (Q4 2027). The

midstreamer also announced two more Delaware processing plants during

its recent call. The 265-MMcf/d Roadrunner II facility and the

275-MMcf/d Copperhead II plant will both start operating in Q1 2028.