Locator: 48419IRAN.

Iran's biggest worry right now: what if the Houthis actually hit an American a/c carrier?

The bigger question: will Trump - Vance - Hegseth let that happen?

Locator: 48419IRAN.

Iran's biggest worry right now: what if the Houthis actually hit an American a/c carrier?

The bigger question: will Trump - Vance - Hegseth let that happen?

Locator: 48418B.

WTI: $67.98.Down 5.2% since new tariff policy announced.

New wells:

RBN Energy: E&Ps continue caution on CAPEX, but gas producers appear ready to ease off the brakes.

President Trump’s inauguration has pushed a flurry of policy changes, including exhortations to the E&P industry to boost U.S. oil and gas output dramatically. However, in their year-end earnings calls, the major domestic producers struck a more cautious and calmer tone, sticking to the same themes they adopted to recover financial stability and win back investors after the pandemic. Total 2025 capital spending by the 37 major U.S. E&Ps we cover is forecast to drift slightly lower from 2024 levels as they continue to eschew growth in favor of maximizing cash flows and shareholder returns.

In today’s RBN blog, we review 2025 investment plans by company and peer group, highlighting trends and reviewing their impact on production, and explain why any additional increases are likely to come from producers with significant gas assets.

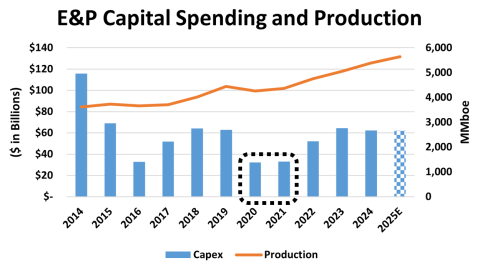

The commodity-price collapse at the onset of the pandemic threatened the financial stability of a chronically overspending E&P industry that had lost the confidence of the investment community. The response, as shown in Figure 1 below, involved drastic cuts to capital spending in 2020 and 2021 (see dashed black box), as producers strategically transitioned their investment focus to maximize shareholder returns over reserve and production growth. As we reviewed in Take It Easy, sustained high commodity prices allowed producers to increase drilling to offset steep shale decline rates, leading to substantial quarterly increases in investment that resulted in total 2022 capex of $52.7 billion, up 51% from the previous year and the largest growth rate in more than a decade. Inflation, as well as increased organic capital outlays related to acquisition activity, led to another 24% increase in 2023 investment to $64.3 billion, similar to amounts spent pre-pandemic in 2018-19. The restored investment over two years resulted in a 14% production gain (orange line and right axis).

Figure 1. E&P Capital Spending and Production, 2014-25E.

Source: Oil & Gas Financial Analytics, LLCHowever, declining cash flows from lower commodity prices in the latter half of 2023 brought the industry to another inflection point. Producers couldn’t fund continued capex increases and sustain dividends and share buybacks without resuming the deficit spending that had rocked its financial stability a decade before. Their decisions about 2024 capital spending couldn’t have been clearer — maximizing free cash flow was the top priority. Total 2024 investment fell 3% to $62.4 billion. One of the drivers of the slowdown in capex was a reduction in the percentage allocated to exploration of unproven acreage. Although the Trump administration is touting the opening of vast new U.S. regions to leasing and permitting, E&Ps have been reducing exploration funding. As shown in Figure 2 below, 2024 exploration spending represented just 8% of total capex (gray line and right axis), down from 13%-14% in 2021-22, as exploration costs (blue bars and left axis) and exploration and development (E&D) spending (orange bars) moved lower.