Locator: 50582MUSK.

Colossus 2 is tracked here.

Supercomputers are tracked here.

Locator: 50582AAPL.

This is not an investment site: (see blog's disclaimer).

Market cap:

PEG: MU -- to compare -- MU, April, 2026, MU's PEG is thought to be between 0.04 and 0.12 as of April 2026, indicating the stock is significantly undervalued relative to its explosive AI-driven earnings growth. This low ratio suggests that despite a higher P/E, projected earnings growth is so high that the stock is considered "cheap

Is this what Apple's new CEO, John Ternes, is walking into? Did Dell get it right? Did Apple get it wrong (initially)? Can Apple right the ship? The AI decisions below were CEO-level decisions. A lot of this depends on how important this subject is to end users and how Dell and Apple market their products.

AI query: AI. This is interesting. For the last couple of years, Apple has been coming under a lot of criticism for its stumbling wiith regard to AI (Siri) but what AI is Dell using?

Reply:

Locator: 50581BRK.

Investing as a hobby (see blog's disclaimer):

Locator: 50580B.

WTI: $90.03.

Active rigs: 22.

Three new permits, #42852 - #42854, inclusive:

Ten permits renewed:

Two permits canceled:

Locator: 50578APPLE.

Tim Cook is really leaving John Ternus with a nice stable of integrated workstations, laptops, iPhones, watches, etc. Interestingly, Ternus has a huge experience with VR. I've always felt Americans were not ready for VR as marketed by META or Apple. It will be interesting if Ternus can change that. It's not that the technology is not good -- it's probably way better than needed -- it (VR) is simply something for which Americans have not found a need.

While the emphasis has been on LLM and AI and chatbots and .... and .... Apple has pretty much managed to widen the gap between itself and the competition.

In addition to the hardware and software, it appears Tim Cook will leave an incredibly good blueprint for AI going forward. The Google - Apple partnership was brilliant. Somewhere along the line, Tim Cook reviewed the concept of "core competencies" (raise your hand if you recall "core competencies").

AI prompt: Apple's MR chip's Neural Engine is capable of 38 trillion operations per second. How does that compare with TPUs (or similar) in typical Dell laptop?

Reply:

********************************

The MacBook Veo

AI prompt: MacBook Veo, what chip? The M4?

Reply:

******************************

Core Competencies

AI prompt: What year and which companies for strategic planning took the lead in advocating for and following "core competencies"? In other words, for US publicly traded corporations, when was the concept of "core competencies" a thing and which companies address their core competencies when laying out a strategic plan?

Reply:

So, Apple pulled the plug on POV/FSD (as far as I know) early on -- one of the best things it ever did -- making that decision. Whether under new leadership ....

Likewise, Apple appears to have pulled the plug on their all-in-house chatbot (Siri) and gone with a hybrid -- Siri plus partnering with Google (Gemini) That was brilliant. They learned a lot in the process but their decision to partner with Google -- very, very smart. Hopefully that's all behind them now and John Ternus can move on to bigger, better and newer things.

Locator: 50577CALIFORNIA.

AI prompt: RBN Energy posted a textbook long (hyperbole; it was only a page or so) analysis of transportation fuel issue in California. Takes forever to read and impossible to really get feel for what's going on in California, except that it's bad Succinctly, how is California doing with current oil situation and the Mideast War?

Reply:

Me: the transportation costs in California are out of control. Not only are prices per gallon high, commute distances are insane. And in southern California, even if the distance is not that long in miles, the traffic makes a one-hour commute (each way) seem normal and acceptable. In Los Angeles County, not unusual to drive two hours from the valley into work.

The amazing thing: this has been going on for decades. It began during the OPEC crisis / embargo in 1973. I had just moved from the Dakotas to southern California where I was to spend the next decade of my life, and would still love to be there except for the taxes, the transportation issues, the politics (Pelosi, Newsom, Steyer and Kamala), and, The Los Angeles Times.

Locator: 50576B.Original Post

Random thought: considering how long the strait has been closed; sanctions on Russian oil and natural gas; relatively strong global economy; minimal recent investment in renewable energy / nuclear -- the world seems to be chugging along pretty well -- South Korea and US stock markets at all-time highs. Europe has major war in backyard with Russia for five years and not much change. Imagine how things would be going if we just all got along.

For the archives:

********************************

Back to the Bakken

WTI: $88.36

New wells reporting:

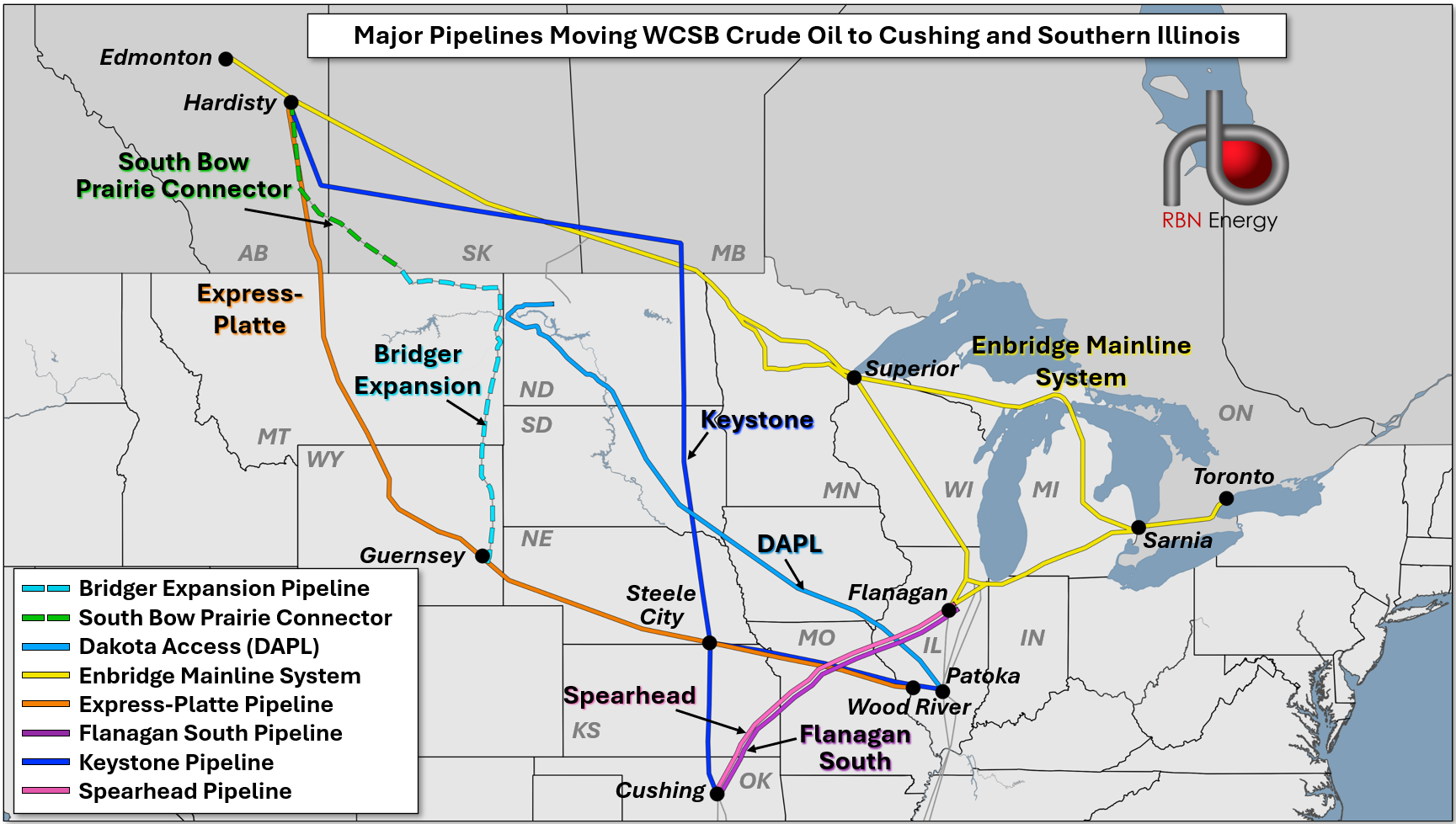

RBN Energy: will more pipeline capacity be needed to move Canadian barrels from the midcontinent to the Gulf Coast? Link here. Archived.

Crude oil production from the Western Canadian Sedimentary Basin (WCSB) continues to grow, and most of that growth is expected to be heavy crude oil, so pipeline companies are working on expanding capacity to move more of those barrels into the U.S. However, as most U.S. Midwest (PADD 2) refiners are already taking nearly as much WCSB heavy crude as they can, the incremental barrels coming into the U.S. will need to find their way to the Gulf Coast (PADD 3). A few projects are in the works that would move those barrels into PADD 2 waystation hubs such as Cushing, OK, and Patoka, IL, but will there be enough room on the four major pipelines — the Four Sticks noted in today’s title — that move barrels out of those two hubs to the Gulf Coast? That’s what we’ll look at in today’s RBN blog.

In Part 1 of our recent Turn Me Loose blog series we discussed the past drivers of WCSB crude oil production growth, which averaged about 170 Mb/d annually over the past 15 years, and grew by nearly 190 Mb/d last year, dwarfing WCSB demand growth that averaged 10-15 Mb/d annually. Our current forecasts are for a slower pace of production growth over the next five years — the major oil sands producers seem to be taking a wait-and-see approach while Canada’s federal and provincial governments negotiate new frameworks for greenhouse gas (GHG) emissions and abatements — but those plans will likely accelerate once policies have been clarified. The Alberta government wants the province’s oil production to double over time to around 8 MMb/d, and there’s plenty of resource to develop.

In Part 5, we looked at all the potential pipeline projects to move more barrels out of the WCSB, including about 980 Mb/d of new capacity into the U.S. that is either underway or proposed:

- Enbridge has defined plans to add about 430 Mb/d of capacity into the U.S. from its Mainline and Express systems and sees additional expansion potential.

- South Bow Corp. and Bridger Pipeline LLC have separate but apparently linked proposals for about 550 Mb/d of new capacity from Alberta to Guernsey, WY; from there, those barrels would need to move further downstream, to Cushing or elsewhere. (For more, see our 80+ page report Roundabout! Canada-To-Rockies Crude Flows Reshaping PADD 4 & Guernsey Market and subsequent webcast presentation.) [President Trump signs order authorizing Bridger Pipeline's proposed project from US-Canade border to Wyoming, April 30, 2026.]

Additionally, more pipeline capacity to British Columbia on Canada’s west coast is in the works. The Canadian government is looking to expand capacity of the Trans Mountain Pipeline System — which added a new 590-Mb/d pipeline, the Trans Mountain Expansion (TMX), in 2024 — by another 300 Mb/d. Plans are to expand TMX by about 90 Mb/d using drag-reducing agents (DRAs) and another 210 Mb/d by adding pumping capacity and 19 miles of new pipeline. The Alberta and Canadian governments are also working to encourage private companies to build a greenfield pipeline from Alberta to the west coast. Recent history with TMX has shown that building new pipeline to the BC coast can be extremely time-consuming and expensive.

Enbridge is moving forward on three WCSB egress projects that involve its Mainline (yellow line in Figure 1 below) and Express-Platte (orange line) systems: its Mainline Optimization 1 (MLO1) and Southern Illinois Connector projects were sanctioned late last year, while Enbridge hopes to sanction its second Mainline Optimization project (MLO2) by midyear. These projects would collectively add 430 Mb/d of pipeline capacity from the WCSB into the U.S. Enbridge has already disclosed plans to increase volumes into Cushing by about 170 Mb/d (+100 Mb/d via an expansion of Flanagan South, purple line; +70 Mb/d by utilization of spare capacity on Spearhead, pink line) and increase volumes into Patoka by about 30 Mb/d (Express-Platte expansion and 56-mile extension to Patoka), but we suspect the remaining 230 Mb/d would need to make its way south to the Gulf Coast.

Figure 1. Major Pipelines Moving WCSB Crude Oil to Cushing and Southern Illinois. Source. RBN

Locator: 50575AMAZON.

South Korean stock market surges to all-time high: headline.

Amazon: trending toward it's 52-week high.

Anthropic: only the most-talked about tech company right now.

Anticipation:

Ackman: link here. Some call this circular financing. Alternative: buy BRK.

Headline: