Locator: 50670B.

Trump Lake: everything suggests CENTCOM will leave one a/c group in the Persian Gulf for a long, long time. The Dems will end that at their own peril. Is there any port in/near the Persian Gulf -- Kuwait, Oman, Qatar, UAE -- that could host an American a/c carrier?

Weekly unemployment figures: incredibly good. Trump won't get any mention. Expected: 213,000. Actual: 189,000. But the real story is how few -- in the big scheme of things -- actually file for unemployment (first time filing) -- with all the negative stories coming out of The NYT and Washington, DC.

LDC power: an excerpt from yesterday's RBN Energy blog -- link here, paywall; link here, blog; link here, archived; link here, Monarch; link here, Colossus.

Sites that opt for gas-fired generation have several paths they can pursue. Combined-cycle turbines can be the most efficient fit, especially at facilities that require high levels of steady power generation, but they can take years to secure thanks to high demand and well-understood supply-chain issues.

Single-cycle turbines appear to be the most popular short-term fix, while reciprocating engines can be easier to obtain and deploy, while also being purpose-built for AI workloads. They are a major part of Nscale’s strategy for the Monarch campus noted above. A combination of solutions may be the best path forward at some sites. Truck-mounted gas turbines from VoltaGrid and reciprocating engines were deployed by xAI to get its 100,000-GPU Colossus facility in Memphis, TN, up and running in just four months.

*********************************

Back to the Bakken

WTI: $104.60.

New wells reporting:

- Friday, May 1, 2026: 6 for the month, 106 for the quarter, 263 for the year,

- 42204, conf, Silver Hill Energy, Texas E 158-92-8-20-3MBHX,

- 42104, conf, Hunt Oil, Meyer 155-90-31-30H-3,

- 42103, conf, Hunt Oil, Burke 155-90-36-25H-2,

- 41644, conf, Hess, EN-Rohde-157-94-3625H-3,

- 41613, conf, BR, Sivertson 6H,

- 40960, conf, Hess, EN-Rohde-157-94-3625H-2,

- Thursday, April 30, 2026: 100 for the month, 100 for the quarter, 257 for the year,

- None.

RBN Energy: US and European refineries thriving so far, but Asian ones suffer. Link here. Archived.

It’s been eight weeks since the steady flow of crude oil and refined product tankers out of the Persian Gulf ended, and the impacts of the still-simmering U.S.-Iran conflict on refineries and product suppliers in the U.S., Europe and the Asia-Pacific (APAC) region are becoming clearer. For many refineries on both sides of the Atlantic, their relatively minor reliance on Middle East crude and the higher prices they are now receiving for their gasoline, diesel and (especially) jet fuel put them in a great spot, at least for now. It’s much different for refineries in many Asian countries, however. Heavily dependent on Persian Gulf oil, they are drawing down their reserves, scrambling for replacements, and hoping the Strait of Hormuz is reliably reopened very soon. In today’s RBN blog, we discuss the current state of refining and refined product supply in the U.S., Europe and APAC.

We should emphasize up front that you can’t make broad generalizations about all U.S. refineries or all refineries in Europe or Asia. Sure, they can be put into categories or groups — for example, complex refineries along the U.S. Gulf Coast (USGC) or “teapots” in China — but each refinery is ultimately unique, with its own location, set of refining/processing equipment, crude slate, and approach to feedstock contracting and refined product sales, among other things. That said, many refineries in each of the three areas we’re focusing on (the U.S., Europe and Asia) are facing similar situations a couple of months into the Iran conflict. As for refined product supply, the U.S. is just fine for the foreseeable future, but Europe and Asia already are struggling and things could get far worse in the coming weeks.

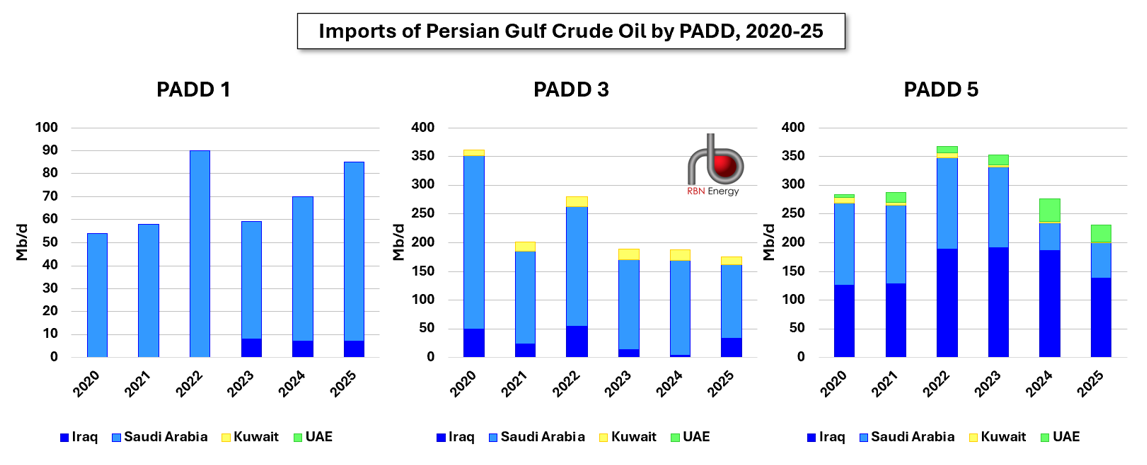

We’ll start with the U.S., whose refineries have been relying less and less on Persian Gulf crude oil in recent years. As we discussed a couple of weeks ago in How Am I Supposed to Live Without You, total oil imports from the region averaged only 491 Mb/d in 2025, down from a peak of more than 2.6 MMb/d in 2001 and the lowest level since 1985. PADD 3 (Gulf Coast; middle chart in Figure 1 below), the only U.S. region to export vast amounts of refined products, imported only 176 Mb/d of Persian Gulf crude last year, less than half of what it did in 2020. That mostly heavier, higher-sulfur oil is readily replaceable by a mix of light shale oil, medium crude from the offshore U.S. Gulf, and heavy oil from Canada or Venezuela. Of note, more than two-thirds of the PADD 3 imports in Q4 2025 were Saudi imports going to Aramco’s wholly-owned Motiva refinery in Port Arthur, TX.

Figure 1. Imports of Persian Gulf Crude Oil by PADD, 2020-25. Source: EIA