Locator: 50649B.

See blog's disclaimer: link here.

WTI: absolutely, positively, the only thing I'm interested in today with regard to the Mideast is whether WTI can hold above $100 at the close. Anything below $96 is a debacle on so many levels; and, I'm not even thinking about my portfolio.

OPEC in disarray: UAE to leave OPEC "immediately"; to increase production; UAE sits at exit to Strait of Hormuz, opposite Iran.

News story, hardly: Trump won't consider Iran's latest proposal. DOA.

In fact, there's really nothing to negotiate, is there? There's a ceasefire in place, so no need to discuss a ceasefire. We all know what is necessary with regard to the strait. Iran does two things: a) says it won't enrich uranium (Iran doesn't have to mean it; just say it); and, b) escort vessels through the strait to avoid mines. Fairly simple.

Right now, we have a Korean truce with the strait a "no-man's land." Water in this case. And every day the strait remains closed, the more irrelevant the Mideast becomes.

The US and Iran are not negotiating Hezbollah; that's an issue for Israel and Iran, not the US.

Markets diverge:

- tech-heavy NASDAQ plunges: down 4% in pre-market; folks panic, MU up over 500% over past year; down 4% in pre-market;

- AAPL: hard to say; up slightly this morning after analyst raises price target;

- oil: up 2%

- so, overall portfolio could be a wash

- overall: buying opportunity -- probably not -- with Micron up 500% in one year, down 4% today is hardly bullish;

Trump: all indications he's in this -- Operation EPIC FURY -- for the long haul. Internal polling: majority of Americans want to see the job done. Curious how long Iran can hold out, losing $500 million / day.

What's driving tech today: one word -- FEAR

- OpenAI: reports it missed internal targets; unlikely to be able to fund all contracts

- Strait of Hormuz: Iran's latest offer -- DOA

- Germany: flipping out! Says US-Europe rift is the fault of the US;

- US oil / natural gas exports: US says it won't "ban" but just that the subject is on the table must be scaring Europe.

************************************

Back to the Bakken

WTI: $99.57 - drops back a bit after hitting $100.50.

New wells reporting:

- Wednesday, April 29, 2026: 100 for the month, 100 for the quarter, 257 for the year,

- 42080, conf, XTO, GBU Hera 33X-7F,

- 42079, conf, XTO, GBU Hera 33X-7A,

- 41734, conf, Hess, EN-Hilleren-157-94-1336H-2,

- 41614, conf, BR, Sivertson 6I,

- 41360, conf, Devon Energy, Marvin 27-34 3H,

- Tuesday, April 28, 2026: 95 for the month, 95 for the quarter, 252 for the year,

- 42081, conf, XTO, GBU Hera 33X-7B,

- 41861, conf, Devon Energy, Finn 13-25F 3H,

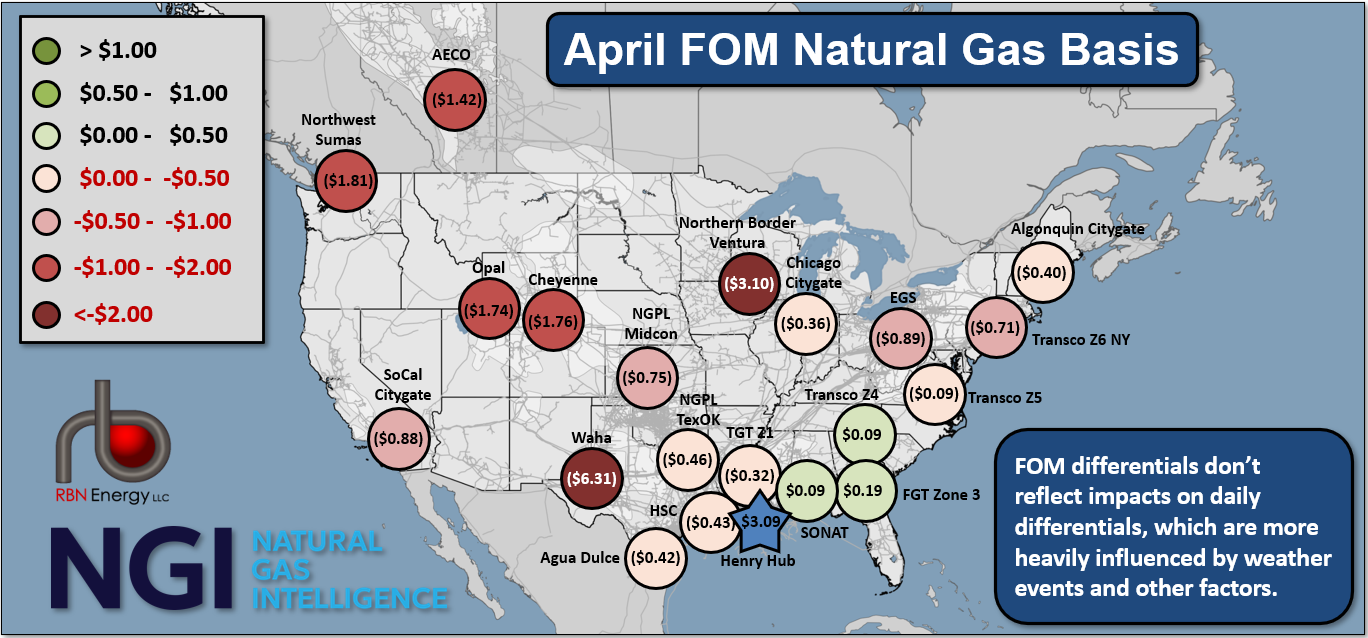

RBN Energy: rising southeast gas demand spurs pipeline projects, competition with LNG exports. Link here. Archived.

We’ve blogged about rising demand for natural gas in the southeastern U.S. and several of the pipeline projects being planned to deliver more gas to that fast-growing region. But there’s more to the story — a bigger picture — namely, that gas consumers in Florida and other states pulling gas east through Mississippi increasingly find themselves competing for supply with LNG exporters. In today’s RBN blog, we begin a two-part series on Southeast gas demand, new pipeline capacity to and through the region, and why the gas flowing there is priced higher than Henry Hub.

Ask your favorite chatbot which states are in the southeastern U.S. and you’ll get a long list — generally, everything within the huge triangle formed by the Virginias, Florida and Louisiana. The Southeastern Conference (SEC) of the NCAA includes Oklahoma, Missouri, Kentucky and two universities in Texas (one of which we like!). But for our purposes, we’re zeroing in on the southeasternmost swath: from west to east, Mississippi, Alabama, Florida, Georgia and South Carolina. While these five states account for only 0.4% (~ 400 MMcf/d) of total U.S. natural gas production, their share of U.S. gas consumption is 30X higher — about 12% or 11 Bcf/d — mostly due to their heavy (and growing) reliance on gas-fired power generation and (especially in Alabama, Georgia and Mississippi) a lot of industrial demand too.

Gas-demand growth in the region has been coming on fast and furious over the past few years, stressing the legacy gas pipeline networks there and resulting in the SONAT (Southern Natural), Florida Zone 3 and Transco Zone 4 price trading points — primary indicators of gas prices in our five-state focus area — being among the very few points where gas is priced at a premium to Henry Hub. [Figure 1 below shows April first-of-month (FOM) differentials — the green-shaded circles indicate trading points where the FOM differential is a premium to Henry.]

Figure 1. April FOM Natural Gas Basis. Source: NGI