The price of WTI clawed its way back to $50/bbl and settled around $49.75.

Refiners along the Texas/Louisiana coast are still working to get their operations up and running, and back to normal after Hurricane Harvey, and Florida is cleaning up after Hurricane Irma.

The US stock market has been on a tear with the three major indices all hitting new highs. Most newsworthy: today the S&P 500 closed above 2,500 for the first time ever.

Operations

The Red Queen is still on her treadmill; North Dakota crude oil production remains over one million bopd; production increased month-over-month

Random look at two Oasis Forland wells

A new operator in the Bakken: Freedom Energy has a permit to target the Lodgepole southwest of Dickinson

Bakken Economy

Legacy Fund breaks through $4 billion in deposits

$5 million Buck Scheele animal shelter could be completed by next spring

Commercial flights at Williston airport remain at capacity; local officials hope more flights will be added next spring

Lynn Helms opines on the $125 billion oil companies have invested in the Bakken

Miscellaneous

North Dakota has state's first ever Miss America

Friday, September 15, 2017

XTO With Permits For A 5-Well Pad In Siverston Oil Field -- September 15, 2017

Active rigs:

Six new permits:

Producing well:

| $49.83→ | 9/15/2017 | 09/15/2016 | 09/15/2015 | 09/15/2014 | 09/15/2013 |

|---|---|---|---|---|---|

| Active Rigs | 56 | 34 | 71 | 199 | 178 |

Six new permits:

- Operator: XTO

- Field: Siverston (McKenzie), Bear Creek (Dunn)

- Comments: XTO has permits for a 5-well Serrahn pad in 5-150-97, Siverston oil field (300 feet from the north line and 800 - 1000 feet from the west line) -- see below

*****************************

Producing well:

- 21682, 968, XTO, Lund 44-8NH, Siverston, 22 stages, 2.8 million lbs, t7/12; cum 168K 7/17; off-line right now; work being done on pad;

The Energy And Market Page, Part 2, T+238; S&P Closes Over 2,500 For First Time Ever -- September 15, 2017

Pundits: didn't "they" say September was historically a difficult month for investors? The month is not over and things could change, but right now the Dow is on track to have its best week since April. The S&P 500 crosses 2,500 for the first time ever. The Trump rally continues. September 15th. You were around to see it. Enjoy the weekend.

Records:

EVs. Investor's Business Daily says one bottleneck could "block" EVs. I haven't seen the article yet, just the headline. Bottlenecks: a) batteries; b) charging stations; c) neighborhood transformers. So, let's see what the article says: a shortage of a key battery component could throw a wrench into their vision for a future of electrified cars. Yup, that was my first guess -- batteries. Now let's see what that rare earth metal (or is it lithium) that will be the issue? Yup, it's lithium.

From The Williston Wire:

Records:

- another record day for the Dow

- another record day for the S&P 500

- another record for the Nasdaq? nope, but close

- close to, or setting, a new record for volume of shares traded

- new highs, 101, including: Boeing, CAT, Statoil, Valero

- new lows, 6

EVs. Investor's Business Daily says one bottleneck could "block" EVs. I haven't seen the article yet, just the headline. Bottlenecks: a) batteries; b) charging stations; c) neighborhood transformers. So, let's see what the article says: a shortage of a key battery component could throw a wrench into their vision for a future of electrified cars. Yup, that was my first guess -- batteries. Now let's see what that rare earth metal (or is it lithium) that will be the issue? Yup, it's lithium.

**************************

Bakken Economy

From The Williston Wire:

Enplanements at the Williston Airport continue to be about the same as last year. In August 2017 there were only 88 fewer passengers compared to the same time in 2016.

Currently, commercial flights at Sloulin Field International Airport are at capacity; making growth difficult.

Airport officials hope more commercial flights will be added in the spring.

Just How Big Is The Bakken? Pretty Big -- September 15, 2017

Staggering: With 60,000 wells in the Bakken, using current technology and current completion strategies the oil companies will extract one-tenth of all the original-oil-in-place (OOIP) -- Lynn Helms.

How many producing wells right now? About 14,000. At the height of the boom, oil companies completed about 2,000 wells/year. Now, with the slump in oil prices, about 600 wells will be completed this year.

At 1,000 wells / year, to add another 40,000 wells, 40 years of drilling activity. And that will get us 10% of the OOIP.

Link here.

Graphic here:

To date: amount oil companies have invested in drilling wells, completing wells, and laying pipeline to transport Bakken oil -- $125 billion. About $2 million / every North Dakota resident (adults and children).

As long as we're having fun, let's work this backwards:

... and a little bit of humor, I can't resist reminding readers of Art Berman's column earlier this year:

Bakken production remains over one million bopd. Bakken crude oil production rose 1.4% month-over-month in most recent report and that was despite the fact that a) WTI is still not priced in Bakken's favor; b) the number of producing wells has remained about constant; c) there are about 1,500 wells shut in for various reasons; and, d) there are about 800 DUCs that can be brought on line in days, not months.

How many producing wells right now? About 14,000. At the height of the boom, oil companies completed about 2,000 wells/year. Now, with the slump in oil prices, about 600 wells will be completed this year.

At 1,000 wells / year, to add another 40,000 wells, 40 years of drilling activity. And that will get us 10% of the OOIP.

Link here.

Graphic here:

To date: amount oil companies have invested in drilling wells, completing wells, and laying pipeline to transport Bakken oil -- $125 billion. About $2 million / every North Dakota resident (adults and children).

As long as we're having fun, let's work this backwards:

- assume each well in primary production eventually produces 1 million bbls / oil (over 30 years of production)

- 60,000 wells x 1 million bbls = 60,000 million or 60 billion bbls of oil

- 60 billion bbls of oil is one-tenth of OOIP which means the OOIP reservoir is 600 billion bbls

- Leigh Price suggested 500 billion bbls OOIP

*******************************

For A Contrarian View ....

... and a little bit of humor, I can't resist reminding readers of Art Berman's column earlier this year:

It’s the beginning of the end for the Bakken Shale play.

The decline in Bakken oil production that started in January 2015 is probably not reversible. New well performance has deteriorated, gas-oil ratios have increased and water cuts are rising. Much of the reservoir energy from gas expansion is depleted and decline rates should accelerate. More drilling may increase daily output for awhile but won’t resolve the underlying problem of poorer well performance and declining per-well reserves.

December 2016 production fell 92,000 barrels per day (b/d)–a whopping 9% single-month drop (Figure 1). Over the past two years, output has fallen 285,000 b/d (23%). This was despite an increase in the number of producing wells that reached an all-time high of 13,520 in November. That number fell by 183 wells in December.What a doofus.

Bakken production remains over one million bopd. Bakken crude oil production rose 1.4% month-over-month in most recent report and that was despite the fact that a) WTI is still not priced in Bakken's favor; b) the number of producing wells has remained about constant; c) there are about 1,500 wells shut in for various reasons; and, d) there are about 800 DUCs that can be brought on line in days, not months.

July, 2017, Data Is Posted -- Director's Cut -- Total North Dakota Crude Oil Production Increases Over 1% Month-Over-Month

Director's Cut for July, 2017, data.

Link here.

Story over at The Bismarck Tribune.

Oil production

Link here.

Story over at The Bismarck Tribune.

- the state has 56 drilling rigs operating, compared with 34 at this time last year and 71 at this time two years ago

- natural gas production increased 1.35 percent to an average of nearly 1.88 billion cubic feet per day, according to the preliminary figures

- flaring: 12%; unchanged month-over-month

- total oil production increased a bit month-over-month

- the number of DUCs also increased month-over-month

- the number of inactive also increased month-over-month

Oil production

- July, 2017:1,047,526

- June, 2017: 1,032,873 bopd (9.6% more than in December, 2016)

- Delta: 14,653 bbl/day increase; +1.4%

- July, 2017:13,981

- June, 2017: 13,926 (395 more than in December, 2016)

- Delta: an increase of 55; 0.4%

- July, 2017: 101

- June, 2017: 109

- today: $39.75

- August: $37.93

- July: $35.83

- June: $34.72

- today: 56

- August: 56

- July: 58

- June: 55

- waiting on completion: pending; 889; up 34 from the end of June to the end of July

- estimated inactive well count: 1,478; up 20 from the end of June to the end of July

- July data: including CBR to coastal refineries is more than adequate

- June data: including CBR to coastal refineries is more than adequate

- May data: including CBR to coastal refineries is more than adequate (major change in verbiage)

- statewide: 88%

- FBIR: 82%

- goal: 88% through October 31, 2020; then 91%

- comment: the trend continues -- large amount of flaring on BLM land

The Political Page, T+238 -- September 15, 2017 -- National Double Cheeseburger Day

The biggest political story of the day: Harvard dis-invites convicted fellow. So far The LA Times is not reporting it (unless the story is really buried); The NY Times reports it but, again, well-buried. Top story over at Fox News.

On CNBC, this morning:

Why does this not surprise me? Baltimore shuts down bicycle-share program because of too many thefts.

This will solve the problem: Schumer hands the Equifax issue to Maxine. I can't make this stuff up. From the most trusted name in news, Time:

Last night while driving to water polo practice, I happened to mention to our oldest granddaughter, who knows something about everything, that I came across the origin of the phrase "10-gallon hat" while reading a book on the English language.

Yes, she knew the origin of the word/phrase. Think Stetson.

On another note, and I have no idea how we got onto the subject -- oh, that's right -- we were talking about best hash browns in the world (McDonald's) and she said their double cheeseburgers were okay, too.

For those who may have missed it: today is National Double Cheeseburger Day.

I haven't been to In 'N Out in a long, long time. Maybe today would be a good day to go. I'm surprised In 'N Out apparently has no specials today, but -- drum roll --

On CNBC, this morning:

Why does this not surprise me? Baltimore shuts down bicycle-share program because of too many thefts.

This will solve the problem: Schumer hands the Equifax issue to Maxine. I can't make this stuff up. From the most trusted name in news, Time:

A proposal to impose sweeping reforms on Equifax and its two main peers, TransUnion and Experian, also has been drawn up by Rep. Maxine Waters, D-California.

************************************

A Note To The Granddaughters

Last night while driving to water polo practice, I happened to mention to our oldest granddaughter, who knows something about everything, that I came across the origin of the phrase "10-gallon hat" while reading a book on the English language.

Yes, she knew the origin of the word/phrase. Think Stetson.

On another note, and I have no idea how we got onto the subject -- oh, that's right -- we were talking about best hash browns in the world (McDonald's) and she said their double cheeseburgers were okay, too.

For those who may have missed it: today is National Double Cheeseburger Day.

I haven't been to In 'N Out in a long, long time. Maybe today would be a good day to go. I'm surprised In 'N Out apparently has no specials today, but -- drum roll --

McDonald's

Select McDonald's locations around the country, including many in Connecticut, western Massachusetts, upstate New York, and Vermont are selling cheeseburgers at the special price of 69¢ on Friday.

The Market And Energy Page, T+238 -- September 15, 2017

Updates

September 15, 2017: pre-orders for all hardware announced earlier this week begin today except for the iPhone X. Early reports, in the form of comments over at Macrumors, suggest that pre-orders for the iPhone 8 and 8 Plus may be doing much better than expected. AAPL shares are up over $2.00 -- surprising to see this interest so soon; usually it takes a few weeks or months. The difference this time? It looks like Apple has adequate supply of the iPhone 8. This will be the phone that parents buy for their older children, and these same parents will hold out for the iPhone X for themselves. I would be surprised if the iPhone X is not constrained (demand will outstrip supply). By having enough iPhone 8's in their inventory to meet demand will really, really have a positive effect on the July - Sept quarter, and that's what is likely driving AAPL shares today. By the way, there are very few negative comments over at Macrumors regarding any of the new Apple products which is also a good omen. It looks the Apple Watch Series 3 is going to be the star of the show.

Disclaimer: this is not an investment site. Do not make any investment, financial, travel, job, or relationship decisions based on anything you read here or think you may have read here.

Original Post

Dow futures: up 9 points following another NK launch.

Minor note: if you are looking for the new Baker Hughes GE company, the ticker symbol is BHGE but on some browsers that will bring you to "Bear Newco." Confused? I was at first. It turns out that "Bear Newco" is a spaceholder name for the new company which will be renamed "Baker Hughes, a GE Company."

Economic data:

- US retail sales fell unexpectedly in August (Hurricane Harvey hit landfall August 25): data points --

- fell 0.2 percent; biggest decline in 6 months; forecast, up 0.1% (actual vs forecast hardly noteworthy?)

- motor vehicle sales tumbled 1.6%, the biggest drop since January (many cars bought at end of month when salesmen trying to meet quotas (did I mention that Hurricane Harvey hit landfall August 25?)

- In a separate report, the Federal Reserve said industrial production declined 0.9 percent in August. That was the biggest drop since May 2009 and followed six straight monthly gains.

EVs?

China oil. New China Energy star, CEFC China Energy Co, still hungry after $9 billion Rosneft deal. Bloomberg here:

- one of the world's largest oil companies

- one week after striking $9 billion deal with Rosneft has been "pegged" as a possible investor in a Russian metals and power business and a free-trade zone in Georgia's Black Sea port of Poti

Zacks on PLUG: link here.

Disclaimer: this is not an investment site. Do not make any investment, financial, job, travel, or relationship decisions based on what you read here or think you may have read here.

*******************************************

Saudi IPO May Be Delayed

On July 11, 2017, I wrote:

By the way, about a year ago I know I wrote on the blog that I doubted we would ever see a Saudi Aramco IPO launch. I just know I wrote that. But I'll never find it. But I will spend the day looking for that post. LOL. Apparently there's a rumor out there (somewhat sketchy, I will admit) that the IPO may not happen. When I saw that, this is what I wrote in an e-mail (not ready for prime time):Now, today, from Bloomberg, prepare for IPO to be delayed.

With regard to the Arab IPO: I know I posted on the blog a year ago that I doubted we would ever see the IPO -- not because of price of oil, but because the KING would never go along with selling part of his kingdom AND the KING would never go along with the transparency required. I will now spend the rest of the day looking for that post. LOL. I'll never find it.

Job Watch

Note: I no longer plan to update "Job Watch." -- May 24, 2018

Trump vs Obama: pending.

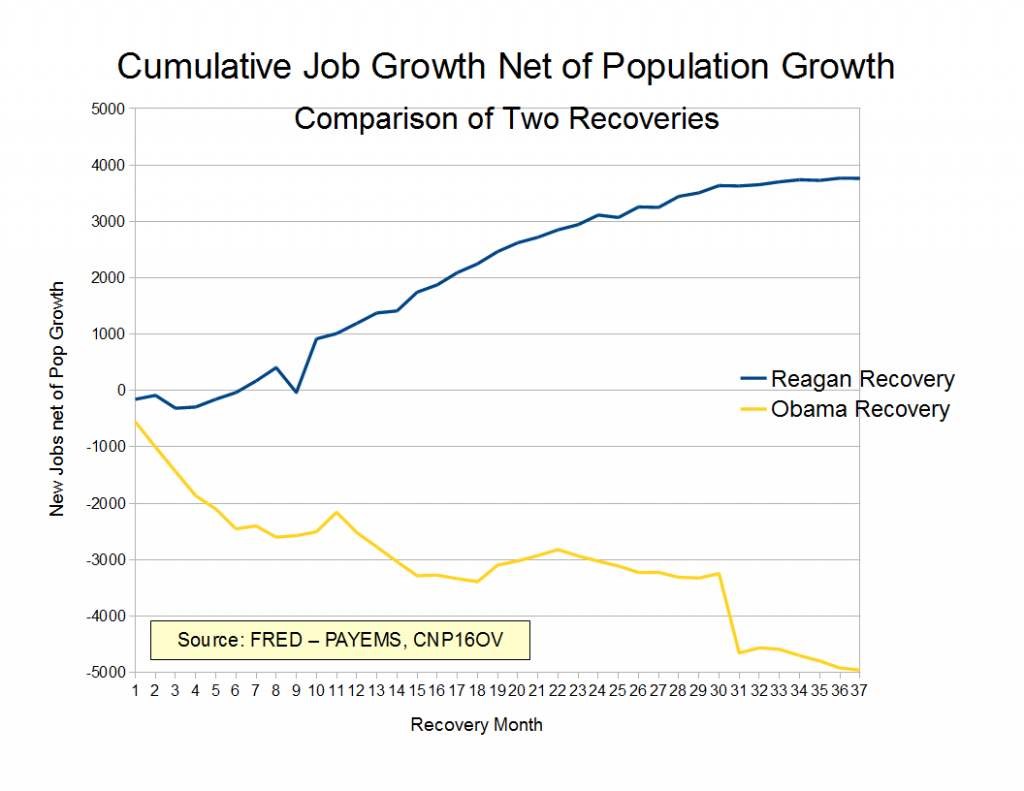

Reagan vs Obama: job recovering following a recession. Reuters and Bloomberg keep telling us job growth is strong, but never seem to really back up that assertion.

The Magic Numbers (change with Trump administration -- see earlier pages for previous "magic numbers")

For "new jobs," 125,000 will be the new "base." The final number under the Obama administration, was 156,000. Even though 156,000 was described as "tepid" by The New York Times, it was associated with economic growth. Now, June 2, 2017, Steve Liesman (and others) suggest that 121,000 is a fine number.

With both these numbers, the Fed under Janet Yellen felt comfortable raising "rates" for the first time in quite some time. [Update: January, 2018: Yellen out, Jay Powell in.]

After about the first two years of posting these updates, it had become clear/obvious that the figures were often suspect, if not outright falsified. On November 18, 2013, it was reported that, indeed, unemployment figures have been falsified.

December 7, 2018: jobs data suggests early signs of economic stagnation, and the Fed is still on a path to raise rates.

June 21, 2018: I will no longer follow "jobs" on a regular basis. Updates will only be provided when something remarkable happens. The Trump administrations is making America great again.

May 24, 2018: new claims far surpass forecast -- 234,000 vs 220,000 forecast.

May 10, 2018: unchanged from previous week, at 211,000 (less than the 220,000 forecast).

May 3, 2018: jobless claims -- essentially flat despite 24,000 decline last week.

May 2, 2018: ADP numbers leave CNBC analyst (an Obama apologist) speechless.

April 19, 2018: flat, down 1,000.

April 12, 2018: at 233,000.

April 6, 2018: bad reports all around. First, yesterday's first time unemployment claims surge 24,000, well more than forecast. Today, jobs added in March fall well short of forecast. Unemployment remains unchanged at 4.1%

March 29, 2018: lowest in 45 years; lowest since January, 1973.

March 22, 2018: unremarkable; 229,000 vs 226,000 forecast.

March 15, 2018: jobs report unremarkable; 226K first time unemployment claims

March 9, 2018: huge report -- jobs report for February:

February 2, 2018: a very, very solid jobs report for January, 2018. Forecast: 177,000 jobs added; actual, 200,000 jobs added. "Very, very solid" -- CNBC.

February 1, 2018: a "healthy" 238,000 jobs added in January -- ADP.

January 25, 2018: rebound from last week, but still beat forecasts.

January 18, 2018: record plunge in first time claims. Claims drop 4x greater than forecast.

January 11, 2018: unexpected surge; now up to 261,000; up 11,000 (or 9,000); harsh winter conditions blamed;

January 4, 2018: up 3,000 to 250,000; previous week revised slightly;

December 20, 2017: rise more than expected.

December 8, 2017: incredible jobs report.

November 30, 2017: essentially unchanged; at 238,000. (I assume the gap from November 16 report was due to Thanksgiving.)

November 16, 2017: claims surge; more than expected; up 10,000 to 239,000.

November 9, 2017: one week claims surge by 10,000; a bit more than forecast; but look at this -- four-week average: declined 1,250 to 231,250, the lowest point for the average since 227,750 in the March 31, 1973 week

November 3, 2017: unemployment at lowest rate since December, 2000 -- 4.1%.

October 26, 2017: increased less than expected (good news); rose 10,000 to 233,000;

October 19, 2017: US unemployment claims fall to 222,000, lowest in 44 years.

October 4, 2017: hurricane effect; ADP dropped to a paltry 135,000 but "the market" is looking past these figures.

September 28, 2017: first time claims up 12,000. The four-week average surged by 9,000, to 277,750, the highest level since February, 2016.

September 21, 2017: huge, unexpected drop. The forecast was for first time claims to actually increase from 284,000 to 303,00 -- an increase of almost 20,000 first time claims. In fact, the number dropped. And it did not drop by an insignificant amount. The drop was huge. The number of first time unemployment claims dropped 23,000. If one adds the 20,000 forecast to the 23,000 decrease, the analysts were a) off in the direction of the move; and, b) off by more than 40,000 claims.

This is Page7

Trump vs Obama: pending.

Reagan vs Obama: job recovering following a recession. Reuters and Bloomberg keep telling us job growth is strong, but never seem to really back up that assertion.

{kind=link}

The Magic Numbers (change with Trump administration -- see earlier pages for previous "magic numbers")

First time claims, unemployment benefits: 275,000 (> 250,000: economic stagnation)New jobs: 150,000 (< 150,000 new jobs: economic stagnation)

Economists estimate the labor market needs to create about 125,000 jobs a month to keep the unemployment rate steady, though estimates vary -- Reuters.For "first time claims," the mainstream media was consistently happy with first time claims ~ 275,000 under President Obama. In hindsight, the previous number of 400,000 seemed incredibly high.

For "new jobs," 125,000 will be the new "base." The final number under the Obama administration, was 156,000. Even though 156,000 was described as "tepid" by The New York Times, it was associated with economic growth. Now, June 2, 2017, Steve Liesman (and others) suggest that 121,000 is a fine number.

With both these numbers, the Fed under Janet Yellen felt comfortable raising "rates" for the first time in quite some time. [Update: January, 2018: Yellen out, Jay Powell in.]

After about the first two years of posting these updates, it had become clear/obvious that the figures were often suspect, if not outright falsified. On November 18, 2013, it was reported that, indeed, unemployment figures have been falsified.

In the home stretch of the 2012 presidential campaign, from August to September, the unemployment rate fell sharply — raising eyebrows from Wall Street to Washington.Take the numbers for what they are worth, I guess. Not much. Rick Santelli, CNBC, January 6, 2017, also suggested the numbers were suspect when the December jobs report, at 156,000, was incredibly bad, and yet unemployment number (4.7%) did not change.

The decline — from 8.1 percent in August to 7.8 percent in September — might not have been all it seemed. The numbers, according to a reliable source, were manipulated.

And the Census Bureau, which does the unemployment survey, knew it.

Updates

December 7, 2018: jobs data suggests early signs of economic stagnation, and the Fed is still on a path to raise rates.

June 21, 2018: I will no longer follow "jobs" on a regular basis. Updates will only be provided when something remarkable happens. The Trump administrations is making America great again.

May 24, 2018: new claims far surpass forecast -- 234,000 vs 220,000 forecast.

May 10, 2018: unchanged from previous week, at 211,000 (less than the 220,000 forecast).

May 3, 2018: jobless claims -- essentially flat despite 24,000 decline last week.

May 2, 2018: ADP numbers leave CNBC analyst (an Obama apologist) speechless.

April 19, 2018: flat, down 1,000.

April 12, 2018: at 233,000.

April 6, 2018: bad reports all around. First, yesterday's first time unemployment claims surge 24,000, well more than forecast. Today, jobs added in March fall well short of forecast. Unemployment remains unchanged at 4.1%

March 29, 2018: lowest in 45 years; lowest since January, 1973.

March 22, 2018: unremarkable; 229,000 vs 226,000 forecast.

March 15, 2018: jobs report unremarkable; 226K first time unemployment claims

March 9, 2018: huge report -- jobs report for February:

- forecast: 200,000

- actual: an incredible 313,000

February 2, 2018: a very, very solid jobs report for January, 2018. Forecast: 177,000 jobs added; actual, 200,000 jobs added. "Very, very solid" -- CNBC.

February 1, 2018: a "healthy" 238,000 jobs added in January -- ADP.

January 25, 2018: rebound from last week, but still beat forecasts.

January 18, 2018: record plunge in first time claims. Claims drop 4x greater than forecast.

January 11, 2018: unexpected surge; now up to 261,000; up 11,000 (or 9,000); harsh winter conditions blamed;

January 4, 2018: up 3,000 to 250,000; previous week revised slightly;

December 20, 2017: rise more than expected.

December 8, 2017: incredible jobs report.

November 30, 2017: essentially unchanged; at 238,000. (I assume the gap from November 16 report was due to Thanksgiving.)

November 16, 2017: claims surge; more than expected; up 10,000 to 239,000.

November 9, 2017: one week claims surge by 10,000; a bit more than forecast; but look at this -- four-week average: declined 1,250 to 231,250, the lowest point for the average since 227,750 in the March 31, 1973 week

November 3, 2017: unemployment at lowest rate since December, 2000 -- 4.1%.

October 26, 2017: increased less than expected (good news); rose 10,000 to 233,000;

October 19, 2017: US unemployment claims fall to 222,000, lowest in 44 years.

October 4, 2017: hurricane effect; ADP dropped to a paltry 135,000 but "the market" is looking past these figures.

September 28, 2017: first time claims up 12,000. The four-week average surged by 9,000, to 277,750, the highest level since February, 2016.

September 21, 2017: huge, unexpected drop. The forecast was for first time claims to actually increase from 284,000 to 303,00 -- an increase of almost 20,000 first time claims. In fact, the number dropped. And it did not drop by an insignificant amount. The drop was huge. The number of first time unemployment claims dropped 23,000. If one adds the 20,000 forecast to the 23,000 decrease, the analysts were a) off in the direction of the move; and, b) off by more than 40,000 claims.

More Natural Gas To Hit The Market; Companies Buying Oil From SPR For Trading / Profit --September 15, 2017

Updates

September 22, 2017: see RBN Energy note below regarding the Nexus pipeline. Argus Media is reporting that the pipeline has received a key water permit from the Ohio EPA.

The $2.1 billion Nexus pipeline project, jointly owned by Enbridge and Michigan utility DTE Energy, will transport Appalachian shale gas to Ohio, Michigan, and Ontario, Canada. One can assume this would not have happened had Hillary been elected president.

Original Post

Active rigs:| $49.92→ | 9/15/2017 | 09/15/2016 | 09/15/2015 | 09/15/2014 | 09/15/2013 |

|---|---|---|---|---|---|

| Active Rigs | 56 | 34 | 71 | 199 | 178 |

RBN Energy: ETP's Rover pipeline sends more Marcellus / Utica shale gas west.

In another key milestone for Northeast pipeline takeaway capacity expansions, Energy Transfer Partners’ beleaguered Rover Pipeline project began partial service on its Phase 1A portion on gas day September 1. The 3.25-Bcf/d project, which is due for completion in early 2018, is expected to provide relief for constrained Northeast producers while exacerbating oversupply conditions and gas-on-gas competition in the Dawn, Ontario, storage and demand market area and surrounding region.

Within days of initial start-up, flows on Rover ramped up to 700 MMcf/d, and both Ohio and overall Northeast production already have posted record highs since then as a result. Today, we take a look at the project, including initial flows and the expected timing of full completion.

It’s been a long, tumultuous road for ETP’s Rover Pipeline project so far. From its inception, the project was competing head-to-head for shipper commitments and investment dollars against the DTE Energy Co./Enbridge 1.5-Bcf/d NEXUS Gas Transmission project which would begin in the same general gas-supply area (eastern Ohio) and serve the same general markets (southeastern Michigan and Ontario).

Then, in late 2016/early 2017, ETP found itself racing against the clock to secure its final certificate of approval and finish clearing trees along the project route before some endangered bats — yes, bats — came to roost . The developer managed to beat the clock on that, with the Federal Energy Regulatory Commission (FERC) issuing the certificate in early February 2017, just one day before the departure of Commissioner Norman Bay broke the quorum needed to get that final approval.

With the certificate in hand, Rover construction proceeded at break-neck speed, and for a while the project seemed unshakable — that is, until disaster struck in May 2017 in the form of a two-million gallon spill of fluid containing diesel in a protected wetland area near the Tuscarawas River in Stark County, OH, which prompted FERC to issue an order halting any new Rover-related drilling activity pending a third-party review.Can't turn it off! Canada gas set to strike back against US shale as glut eases.

Canadian natural gas, locked in a fierce battle for market share with U.S. shale, may stage a modest recovery as output from some longtime producers wanes and pipeline maintenance ends.

While Canadian gas will almost always trade for less than U.S. gas -- due mostly to the cost of moving the fuel to markets in Texas and the American Midwest -- the discount recently widened to the most since 2005. The culprits are prolific new wells that are hard to shut off, along with outages on a network of pipelines that move gas around Alberta.

But with the pipeline repairs that caused those disruptions mostly completed and producers like Royal Dutch Shell Plc and Petroliam Nasional Bhd's Canadian unit dialing back on output in British Columbia, the glut of Canadian gas may ease. Higher prices would be a boon for Canadian producers that have been forced to cut costs and seek new outlets in the face of escalating competition from the U.S. shale gas boom.

Canadian gas, which is tracked using benchmark Alberta Energy Company prices -- AECO for short -- traded at $2.70 per million British thermal units less than the U.S. benchmark Henry Hub gas price on Tuesday, the steepest discount since December 2005. It narrowed to $1.33 on Wednesday.

That project, which is nearing completion, will increase the capacity of the northwest portion by about 700 million cubic feet a day, the Calgary-based company said in an emailed statement. Many sections are completed and operating again, and others will be back in service this month.

The work hurt Canadian prices because many producers weren't able to stop output. For some, the cost of shutting down and reactivating fields would have been more burdensome than taking a short-term hit. For other wells, a complex ownership structure and varying types of contracts with pipeline companies kept them producing even if one partner would have preferred to stop.Buy low, sell high. Six companies buy oil from SPR. Data points:

- 14 million bbls sold/bought

- the six companies:

- BP Oil Supply

- Exxon Mobil

- Phillips 66

- Shell Trading

- Valero Marketing and Supply

- Macquarie Commodities

- bought: range from $46.91 to $47.91/bbl; slightly below current futures price of about $49.70

Job watch, link here:

- dropped: 14,000

- at 284,000

- affected by hurricanes

- better than the forecast of 300,000