These days, there are three main factors affecting the propane market: export economics, export dock space and storage levels. The war with Iran has dramatically shifted export economics and filled dock space, yet storage remains at all-time highs. In this two-part blog series, we will look closer at all three factors and provide our outlook for what’s in store for the remainder of 2026. In today’s RBN blog, we will review how we got here and discuss the upcoming changes in the supply/demand balance.

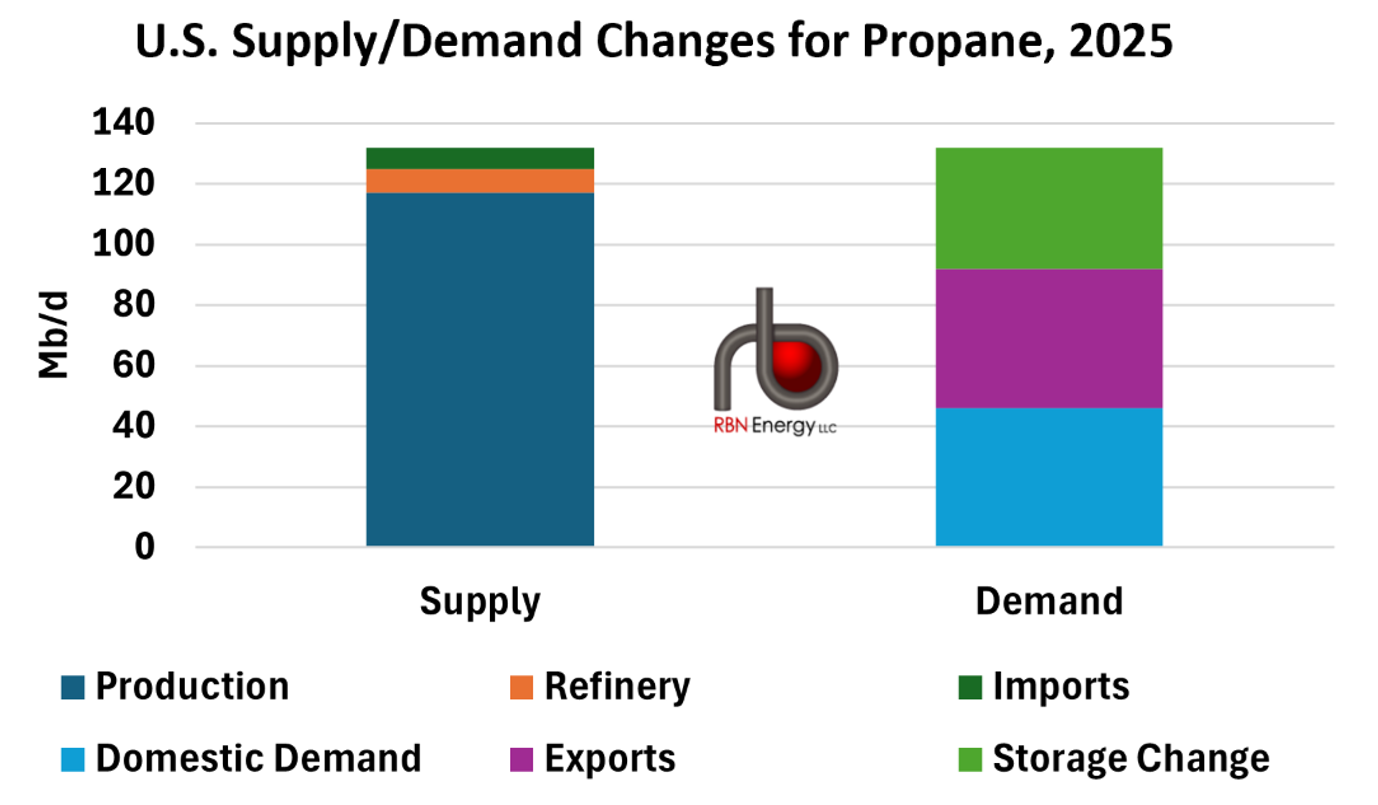

Propane inventories as of April 17 were 80 MMbbl — more than 23% higher than they have ever been this time of year. How did propane storage get so high? The math is simple. Figure 1 below illustrates the changes in both supply and demand. In 2025, total gas plant production (dark-blue bar segment at left) increased by 117 Mb/d, supply from refineries (orange segment) increased by 8 Mb/d and supply from imports (dark-green bar segment) increased by 7 Mb/d. At the same time, total domestic (non-export) demand (light-blue bar segment at right) increased by 46 Mb/d, with export demand (purple bar segment) rising by the same amount. This resulted in a total supply increase of 132 Mb/d and a total demand increase of 92 Mb/d. The balance is growth in storage of 40 Mb/d (light-green bar segment). That may not seem like a lot in a 2.7-MMb/d market, but multiply that figure by 365 days in the year and you end up with a 15-MMbbl storage surge.

Friday, April 24, 2026

Alison's Quick Connects -- April 24, 2026

Locator: 50615B.

Alison's quick connects:

One New Permit -- April 24, 2026

Locator: 50614B.

NVDA: $5 trillion market cap. I don't know about you but I find that simply amazing. Think about that .... Jensen Huang --- started out in his thirties (?) -- within the last ten years (?) and grows a company to $5 trillion market cap. I find that just amazing.

*******************************

Back to the Bakken

WTI: $94.40.

Active rigs: 23.

One new permit --

- 42860, loc, Hess, GO-Daniel-156-98-0322H-3, Wheelock, lot 2, section 3-156-98, to be sited 469 FNL and 1981 FEL, three-section spacing; section 3 / 10 / 15 -156 - 98.

Apple Sells Of Friday Afternoon -- On No News? April 24, 2026

Locator: 50612AAPL.

Before we get to AAPL, look at AMD today: up $41 today!

********************************

Now AAPL / Apple

Apple / AAPL: The New York Times story posted two hours ago was no doubt the reason for the sell-off. Nothing new in the article. But as an investment, AAPL worries me also; the products are great but the risks are huge for an investor. I said I would never add to my AAPL position, I'm so overweighted in the stock but when it gets to $164 / share it's hard not to add to my position.

Apple: reports Thursday, April 30, 2026. And, no, Tim Cook will not have stepped down by then.

Meanwhile:

See disclaimer: this is not an investment site.

Today:

One month:

My Favorite Chart: MMF -- The Book Page -- Pauline's Trials And Tribulations -- April 24, 2026

Locator: 50611MMF.

Tag: MMFS.

My favorite chart: MMFs. Link here. After a record outflow last week, the outflow continues this week, albeit at a trivial pace.

***********************

The Book Page

The Jewish Annotated New Testament, NRSV, Second Edition, Oxford, c. 2010. Notes at this post plus elsewhere.

Felix, Festus, and King Agrippa II.

BRKB Is Down Again Today -- This Barron's Story Isn't Helping -- April 24, 2026

Locator: 50610BRKB.

Locator: 50610DEBACLE.

My hunch: no more annual meetings like the ones we were used to seeing with Munger / Buffett.

How bad is it? BRKB is getting beaten badly by MDU.

Ticker:

This is one of the longest stories I've ever seen in Barron's. This is not a good news story. Story in Barron's generally get no comments. This story had around 40 the last time I looked.

Berkshire Hathaway CEO Greg Abel isn’t following the original script when it comes to running the company’s $300 billion equity portfolio.

Warren Buffett originally envisioned that Ted Weschler and Todd Combs would run the portfolio when he stepped down as CEO.

“Todd and Ted—possibly aided by one additional manager—will have responsibility for the entire equity and debt portfolio of Berkshire, subject to overall direction by the then-CEO and Board of Directors,” the company said in a press release when Weschler was hired in 2011.

While Buffett was CEO, Combs and Weschler each had been running about 5% of the portfolio with Buffett handling the rest.

Abel succeeded Buffett as CEO at the end of last year and appears to be running 94% of it himself, while giving Weschler, a veteran Berkshire investment manager, authority over 6%. The 6% figure was cited in Abel’s inaugural shareholder letter in February, when he wrote that Weschler would get additional authority for some holdings run by Combs.

Combs left Berkshire in December for an investment job at JPMorgan Chase and won’t be replaced, according to The Wall Street Journal. Abel also decided to sell the stock that Combs had accumulated for Berkshire, the WSJ said. Barron’s wrote those holdings could total $15 billion.

Part of Abel’s strategy is to essentially freeze about two-thirds of Berkshire’s portfolio. He wrote in his annual letter that Apple, American Express, Coca-Cola, and Moody’s were core investments, with “limited activity in these holdings” likely.

The same approach applies for the five Japanese trading companies totaling about $40 billion that Buffett has accumulated since 2019, he wrote. These holdings total about $200 billion now.

There could be limited major additions to the portfolio anytime soon. Abel is a part-time manager, Weschler has limited authority, and Buffett sees little that excites him in the stock market.

Buffett told CNBC on March 31 that he wasn’t “finding things” in the stock market except for what he described as a tiny purchase. Asked about the then-5% year-to-date drop in the S&P 500, he said “this is nothing,” noting the index has been down 50% three times during his tenure as CEO.

The reported sale of the Combs-run stocks do follow a pattern. Berkshire sold many stocks held by former investment manager Simpson when he retired about 15 years ago, and it unloaded most of the $3 billion of stocks held by Alleghany after it bought the insurer in 2022.

Still, it seems rash to sell the Combs stocks simply because he departed. Combs bought blue-chip stocks, and selling them will probably will incur a tax bill and boost Berkshire’s cash toward $400 billion. Berkshire likely is sitting on too much cash already.

Canada Approves Enbridge's $4 Billion Natural Gas Pipeline Expansion -- April 24, 2026

Locator: 50609ENB.

Each day the war drags on, the Mideast (oil -- Saudi Arabia; natural gas -- Qatar) grows more irrelevant.

CVX, others are chomping at the bit to get to Venezuela's heavy oil.

But look at this -- not enough to share with Asia.

META Strikes Deal With Amazon's Cloud Unit To Use Its CPUs -- April 24, 2026

Locator: 50608AMAZON.

Story over at Reuters; story will soon be everywhere. This is a huge development for those following along. Bodes well for Apple.

The Intel story explains everything. But this is really, really cool. Was the Intel quarter a one-off? The question is whether to sell, buy, or hold now. Next question: is INTC a meme stock?

Lots of data over at this post. This is where I will track Intel's 1Q26.

APP ECONOMY: INTC, TSLA, and TSM. One is an outlier.

TSMC: link here.

TSLA: link here.

INTC: link here.

Phelan, Hegseth, Tulsi, Noem, And All That Jazz -- Dinner Plans -- April 24, 2026

Locator: 50606DINNER.

For the archives:

April 24, 2026: this is huge. If you're a political junkie. I'm not but still the same, this is fascinating.

Hegseth fired Trump's #1 friend -- John C. Phelan as US Secretary of the Navy. Phelan campaigned hard to save his job. Didn't succeed. Phelan and Trump are literally next-door neighbors, living in almost exactly same-looking houses in Florida. A year ago, Hegseth was a Tier 2 player in the administration; clearly Hegseth is a Tier 1 player now, along with Rubio and Burgum. Surprisingly Tusli Gabbard still holds her job. So, to date only two big names removed, Noem and Bondi, and apparently Noem has a very, very nice new position and still living in the house that is supposed to belong to the Commandant, US Coast Guard. Bondi is transitioning to the private sector.

My hunch: Phelan and Trump still get along, and we may see Phelan show up again, somewhere in the administration, perhaps working with Howard Lutnick in some capacity -- except there would not be enough room in the commerce building for two such egos.

Dinner: the Ellisons are hosting a dinner for the Trumps this weekend. I guess it's tonight. The White House Correspondents' Dinner is tomorrow night, Saturday, April 25, 2026. Trump is attending this year. I assume with limited seating Kristi Noem won't be attending.

Anticipation: SLB Earnings Out Before This Morning's Open -- Beat On Both Top Lines, But Not By Much -- April 24, 2026

Locator: 50605SLB.

Pre-market trading:

- NASDAQ: up 350 points

- Dow: continues to improve; now down less than 40 points.

- when Obama was president, he would give a speech about now, and the market would tank

TSM: holy mackerel -- jump to record high. Up 4% in pre-market trading. Up $15.

AMD: up 12%; up $36 in pre-market trading.

MU: up over 2.5%; up $12 in pre-market trading.

CAT: after surging $26 yesterday, up another $5 in pre-market trading.

PG: beats. Shares up 4% in pre-market.

SLB: if buyers are in a bad mood today, SLB will SLMP. Earnings are out: SLB beat on both top lines but not by much. Shares are down huge -- down $4 / share; down 2%. Ouch. Having said that, SLB is trading at a 52-week high. Pays 2%. Raised dividend in February, 2026, but has significantly slowed is increase in dividends over the years.

Friday, April 24, 2026

Locator: 50604B.

The $64,000 question: if push came to shove, how fast could South American / Latin American oil replace Middle East oil. My hunch: faster than most folks think.

SLB earnings out this morning: before the opening.

Wow, wow, wow. Peter Zeihan touched on it again today -- the challenge of America's light crude oil (shale).

Canceling the Keystone XL was the single biggest energy mistake made in recent history. Like in the past 100 years. That may be the real reason we're seeing high gasoline prices in the US. We have an excess of oil; unfortunately for our consumers and the refiners, it's the wrong kind of oil. That's a very simplistic but sometimes simple is good.

Jones Act: by the way, which type of oil was the first to be loaded upon announcement of the Jones Act wavier? Yup Bakken. This is the link if you need it.

Nscale's Monarch: CAT and BESS. Link here. This story simply gets bigger and bigger. CAT up 3.3% ($26 yesterday) and will hold that gain today. Do you know that a year ago one could have bought CAT at $300? Today? $835. And CAT pays a dividend. Comparing INTC vs CAT:

- one day: CAT

- five day: CAT

- one month: INTC

- six months: INTC but close

- one year: INTC but close

- five year: CAT by a landslide

- and, oh, did I mention, CAT pays a dividend? Albeit not much but that's probably due to the astronomic rise in share price.

Oil prices: $95 is the new baseline.

We've had three shocks to the system -- the OPEC embargo back in the 80s; Covid, 2020; and now the war. This time around, the numbers don't make sense and it seems analysts are more hopeful than realistic. Seriously, do you think we're back to $60 oil by summer? Airlines can't catch a break.

Iran: two huge developments --

- Trump's order to "shoot and kill" the fast boats; and,

- Kharg Island storage tanks should be full by the beginning of next week; if so, Iran will need to start shutting in its wells.

Intel's numbers: they don't add up. But the story/myth/hope is bigger than reality. Is there a possibility that Intel has become a meme stock?

Nvidia is scrambling. It's all about the CPU / GPU ratio and AMD is on the winning side right now.

MSFT: stumbling? Co-Pilot just the tip of the iceberg? But, wow, it's very, very difficult for MSFT to do this (cut jobs); absolutely did not want to do this. Not exactly a Hobson choice, I suppose, but that's what comes to mind. Others also trimming: META and Amazon. LDCs are costing them a bundle.

MSFT will cut employees by 7% -- first time in history that MSFT has cut employees? It's even a huge story in The New York Times. Link here. First time in its history? Yes, that's true: As of April 2026, Microsoft is taking a historic step in its 51-year history by offering voluntary retirement buyouts to U.S. employees for the first time. This move is aimed at restructuring the workforce, rather than a traditional involuntary layoff, and targets long-serving staff. Dead wood.

Insane: all of a sudden the energy crisis is all about Pakistan. Seriously?

For heaven's sake, it's a developing nation: as of early 2026, Pakistan’s economy ranks roughly 42nd–45th globally by nominal GDP (approx. $376 – 408 billion), placing it among developing nations. While its GDP per capita is quite low (around $1,600), ranking near 162nd, its large population supports a high PPP rank (23rd–27th). PPP: purchasing power parity.

Rail vs trucking: with investing, I learned during the Bakken revolution that at the end of the day, US transportation competition at the broadest level is "rail vs trucking."

The size of the transportation pie is pretty much stable; the slice of your piece of pie varies based on relative support for one or the other, rail or truck. Top discriminator? Price of diesel. Trains are so much more fuel efficient; trucks are so much more flexible, but incredibly expensive for the customer. This explains UNP's recent share price surge, I would suppose.

By the way, how is "stuff" being shipped to all these new LDC sites? I don't see a lot of heavy machinery moving cross country on trucks.

UNP at a 52-week high; who would have guessed. PEG on the high side, 2.5 to 3.5. Anything over 1.0 is "expensive" but I'm sure seeing a lot of great legacy companies, value companies, withe a PEG 2x to 3x that "1.0."

52-week high and look at that dividend: UNP will likely increase it's dividend in August, 2026, lifting it to $1.42. Could raise it as early as May, 2026. If it hits $1.42, that would be a 33% increase in its dividend since 2021. Has your salary increased by 33% in the past five years? In 1990, UNP paid 20 cents / share, or 7%. Just saying.

*******************************

Back to the Bakken

WTI: $97.77, going into the weekend. Pre-market.

New wells reporting:

- Saturday, April 25, 2026: 83 for the month, 83 for the quarter, 240 for the year,

42085, conf, XTO, GBU Hera 33X-7C,

- 41097, conf, Enerplus, Lind 145-97-2-11-6H,

- 41096, conf, Enerplus, Lind 145-97-2-11-5H,

- Friday, April 24, 2026: 80 for the month, 80 for the quarter, 237 for the year,

- 42184, conf, BR, Omlid 6-8-7 MBH,

- 41862, conf, Devon Energy, Finn 13-25F 4H,

- 41362, conf, Devon Enegy, Marvin 27-34 5H,

- 41361, conf, Devon Energy, Marvin 27-34 4H,

- 41095, conf, Enerplus, Lind 145-97-2-11-4H,

- 41094, conf, Enerplus, Lind 145-97-2-11-3H,

- 41093, conf, Enerplus, Lind 145-97-2-11-2H-WLL,

RBN Energy: propane exports to increase i 2026 as war with Iran shifts market dynamics. Link here.

Figure 1. U.S. Supply/Demand Changes for Propane, 2025. Source: EIA