Locator: 50984B.

Josh: UNP -- this is gonna be good.

QCOM: on the move.

Longevity: the lead-up to the dot-com bust took about five (5) years (1995–2000), marked by a slow-building speculative frenzy before the market peaked and collapsed. In contrast, the current retail AI market has lasted roughly 3.5 years since the mainstream generative AI boom began in late 2022, though its momentum has been driven more heavily by corporate earnings.

Jargon: IDE -- integrated development environment.

Cursor and Anthropic's Mythos: competitors. Same outcome; different methods.

Cursor is an AI-powered code editor originally developed by Anysphere, a San Francisco-based software startup founded in 2022 by Michael Truell, Aman Sanger, Sualeh Asif, and Arvid Lunnemark;

Mythos is Anthropic's most powerful, or “frontier”, model. When first announcing the model in April, the company said it was too good at hacking to release immediately. Instead, Mythos was made available to a handful of organisations (mostly US tech corporations) to use to patch weaknesses in essential digital systems.

Cursor and Anthropic increasingly operate as competitors. While Cursor built its reputation as an AI-first IDE that routes queries to models like Claude, it has evolved into a comprehensive coding platform. It now features its own powerful, native, multi-file agentic models like Composer and has expanded its ecosyste

AI: two huge stories --

Interest rates:

- EU raises rates;

- US Fed will make no changes in the US Fed rate tomorrow ;

- consensus: US Fed rates will remain unchanged for the next year;

- CNBC: US Fed rates will drop this next year;

- CNBC: mock board -- not one change through all of 2027;

- me? for investors (not traders) the Fed is irrelevant in the face of AI;

- for investors — this is what is relevant

- AI

- memory shortage

- FOMO

- Mangos: minimal effect on decision making

- similar to the rush to drilling in the Bakken in 2007; money not an object; time was the issue;

- S&P 500 companies excluding Mangos:

- financial decisions significantly effected by US Fed rates

- dropping way faster than “expert” analysts projected

- even CNBC says retail / market is much more resilient than expected;

- of course, Trump not mentioned.

*************************************

Back to the Bakken

WTI: $77.65.

New wells reporting:

- Wednesday, June 17, 2026: 23 for the month, 179 for the quarter, 336 for the year,

- 42417, conf, Kraken, Emerson 33-28-21 4H,

- Tuesday, June 16, 2026: 22 for the month, 178 for the quarter, 335 for the year,

- 42416, conf, Kraken, Emerson LE 33-28-21 11H,

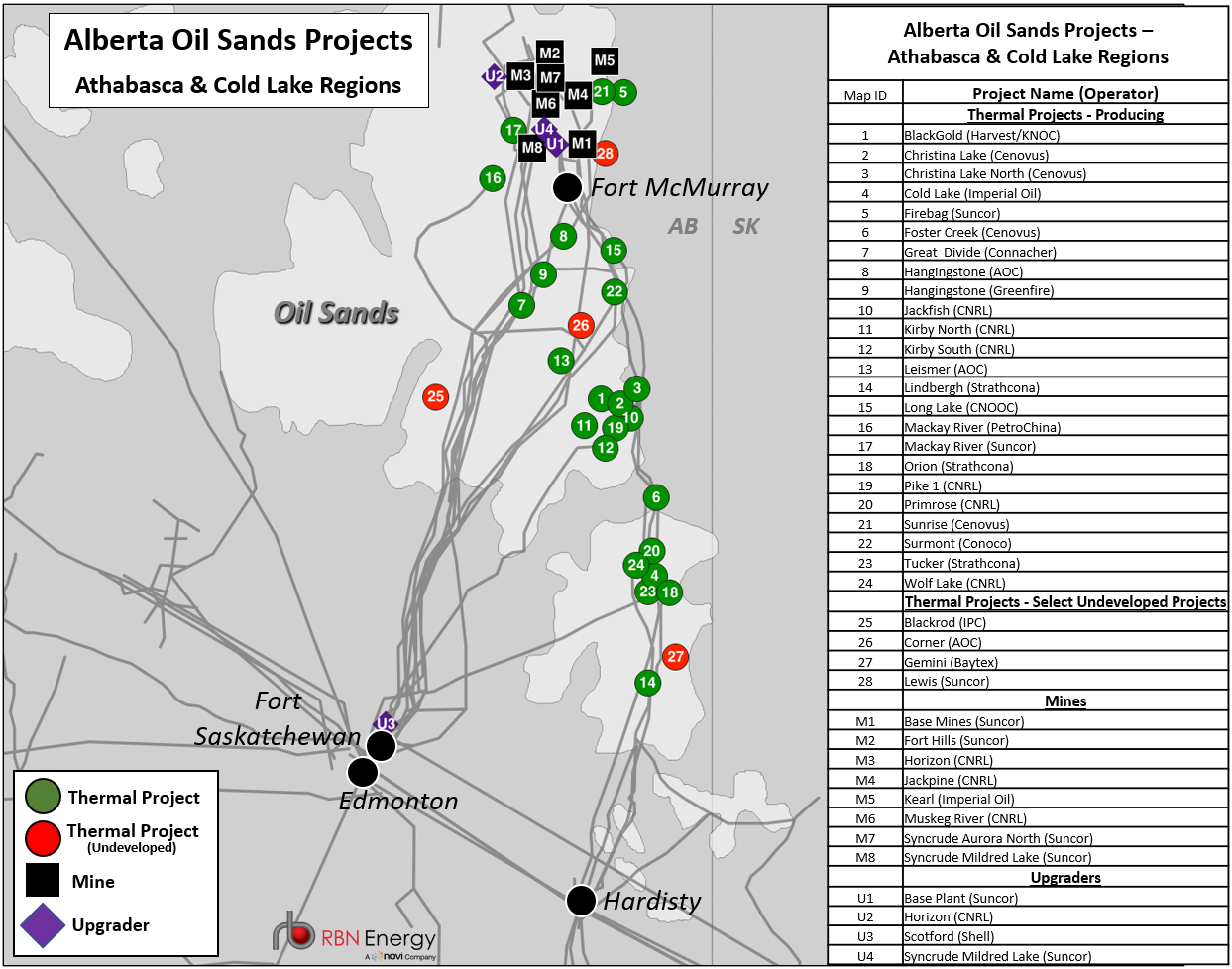

RBN Energy: Alberta's oil sands producers poised to significantly ramp up crude oil output. Link here. Archived.

With another 180 Mb/d of pipeline capacity out of the Western Canadian Sedimentary Basin (WCSB) expected online by late next year, and potentially another 1.7 MMb/d of capacity being proposed over the next several years (excluding a new pipeline to the West Coast of Canada), WCSB producers are looking to grow their crude oil production. With no shortage of resources to develop in the oil sands, in today’s RBN blog, we look at all the Alberta oil sands growth projects currently proposed over the next several years.

In Part 1 of this series, we discussed the drivers behind WCSB crude oil production nearly doubling from 2010 to 2025, as well as its seasonal trends. In Part 2, we reviewed the major pipeline projects that expanded capacity to move barrels out of the WCSB up to this point, how the timing of those projects matched up with supply growth, and current export pipeline capacity. In Part 3, we examined how WCSB crude oil price discounts are impacted by pipeline scarcity and production seasonality. In Part 4, we looked at where WCSB crude oil goes, how it gets there, and how its end markets have evolved over time. Finally, in Part 5 ,we reviewed all the projects in the works to expand crude oil pipeline capacity out of the WCSB.

Figure 1. Alberta Oil Sands Projects, Athabasca and Cold Lake Regions. Source: Novi Labs