Locator: 50938B.

I may be busy tomorrow morning so I will post what I can tonight and then update tomorrow as time permits.

Apple's 2026 WWDC: begins Monday, June 8, 2026, in less than 24 hours. Tim Cook's last major conference as CEO?

The screwworm: fascinating story. Link here. A costly but manageable problem.

************************************

Back to the Bakken

WTI: rising quickly Sunday night, as Iran fires ballistic missiles toward Israel and Israel targets military sites in Iran.

In the last few hours (around 10 p.m. CT Sunday night), WTI has risen 3.43%; has risen $3.11 / barrel; and, is now trading at $93.65.

I believe WTI has been as high as $107 during this current skirmish (during the last 100 days).

Later, 3:39 a.m. CT, Monday morning, June 8: up $4.02; up 4.44% (no typo); and, trading at $94.61. CVX up $2.69 / share, up 2.7%, futures; COP, up 2%.

Analysis: I assume analysts will be able to explain what is going on in the Mideast. If it's obvious to me, I assume it's obvious to The New York Times.

New oil wells reporting:

- Wednesday, June 10, 2026: 10 for the month, 166 for the quarter, 323 for the year,

- 41758, conf, KODA Resources, Stout 1336-8BH,

- 36281, conf, Enerplus, Elephant 148-94-03A-10H,

- Tuesday, June 9, 2026: 8 for the month, 164 for the quarter, 321 for the year,

- None.

- Monday, June 8, 2026: 8 for the month, 164 for the quarter, 321 for the year,

- 42169, conf, Formentera Operations, FTH-22-34-BND S518HF,

- 36277, conf, Enerplus, Gazelle 148-94-03A-10H-TF,

- Sunday, June 7, 2026: 6 for the month, 162 for the quarter, 319 for the year,

- 42170, conf, Formentera Operations, Maverick 22-10-BND N618H,

- 42006, conf, Slawson, Cannonball Federal 4-27-34H,

- Saturday, June 6, 2026: 4 for the month, 160 for the quarter, 317 for the year,

- 42005, conf, Slawson, Sauger Federal 5-22UH,

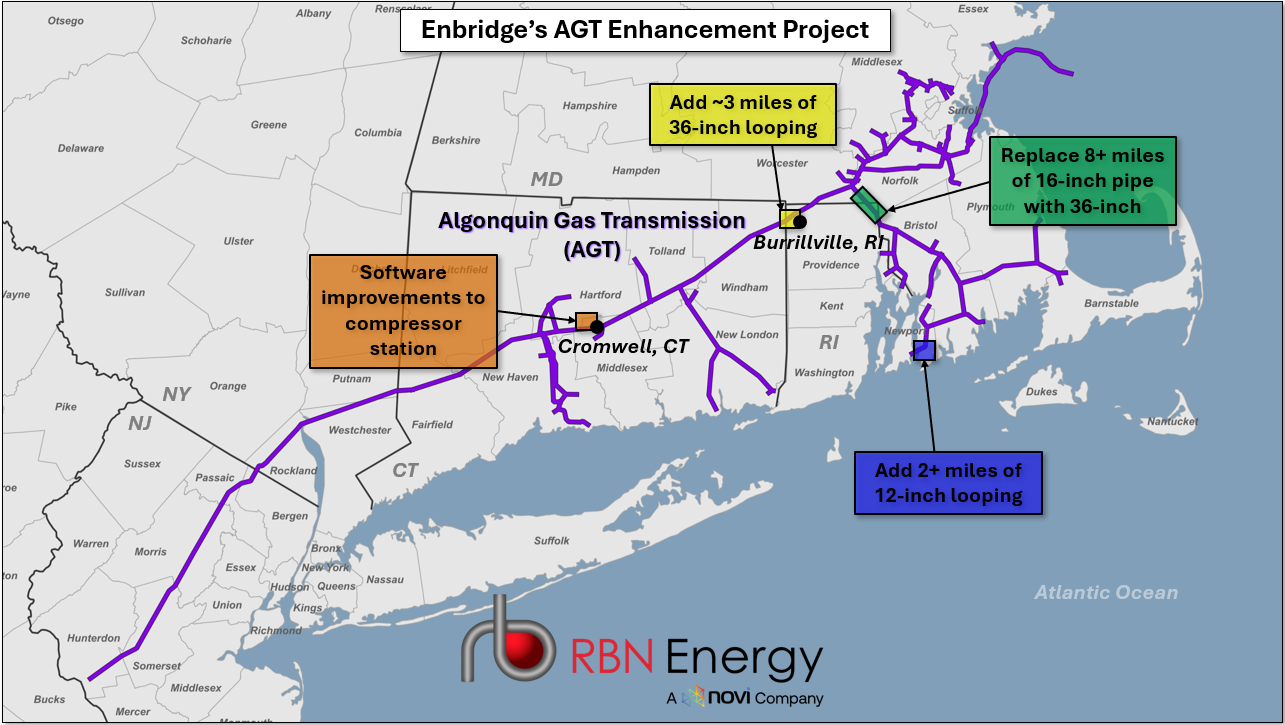

RBN Energy: the pipeline projects that will move more natural gas through (and out of) the northeast. Link here.

The Marcellus/Utica still has vast amounts of economically recoverable natural gas to supply the ongoing surge in demand from power generators and LNG exporters. But there’s a catch: A significant step-up in Appalachian production can only occur if new pipeline infrastructure is built to transport that incremental gas to where it’s needed. In today’s RBN blog, the third in a series about Northeast gas market dynamics, we begin an analysis of the new pipelines and pipeline expansions being planned to move more gas within — and out of — the U.S.’s largest gas production region.

As we said in Part 1 (published 5/12/2026. link here), while the dramatic changes happening in Texas and Louisiana have garnered most of the gas market’s attention the past year or two, the Northeast has been quietly evolving in ways that will not only shift flow patterns within the region but also affect flows to the Gulf Coast. New pipeline development is, well, no longer a pipe dream, and, as we detailed in Part 2 (published 5/29/2026, link here), gas demand within the Northeast is getting a big boost from the power-generation sector as coal retirements continue and new data centers expect to rely heavily on gas-fired power.

Today, we get down to specifics regarding the new pipeline capacity that is being planned to (1) deliver incremental volumes of gas to customers in the Northeast and (2) move increasing amounts of gas to customers outside the region.

We’ll start with a look at the pipeline projects aimed at markets in New England, New York and New Jersey, then shift to projects that will transport more gas within the Marcellus/Utica itself, down the Eastern Seaboard and, finally, to the Midwest.

We should note up front that there’s some overlap — for example, at least a couple of projects involve moving gas west into Ohio and then down into the Southeast.

For years, it has been a largely unfulfilled dream of Marcellus/Utica producers and midstream companies to send more gas into New England. Time and again, proposals to significantly expand pipeline infrastructure into and within the six-state region hit a wall of resistance higher than the Green Monster at Fenway. But elected officials and regulators there have become more open to the idea of brownfield expansions to the existing pipeline grid, if only to reduce the need for diesel-fired power during peak winter demand periods and help replace the output of offshore wind projects being delayed or canceled due to opposition from the Trump administration.

Figure 1. Enbridge’s AGT Enhancement Project. Source: Novi Labs