Physical crude oil, global: supply surged to record highs. Repeat: global physical curde oil has surged to record high. And yet, prices have surged to recent record highs. What's driving the paradox.

At least 12 million barrels per day of supply—roughly 12% of global

output—remains effectively shut in due to the disruption around the

Strait of Hormuz. That has forced refiners in Europe and Asia to bid

aggressively for replacement barrels from the North Sea, Africa, and the

Atlantic Basin.

For now, the market remains defined by access to prompt barrels.

RBN Energy: US E&Ps stay cautious on 2026 CAPEX amidst market volatility. Link here. Archived.

The

roiling of global energy markets by war in the Middle East has, at

least temporarily, magnified the importance of domestic oil output and

dramatically heightened interest in production trends. As lower prices

continued to erode returns for oil producers in 2025 and into early

2026, it’s no surprise that E&Ps accentuated a cautious,

discipline-first approach in their initial 2026 capex and production

guidance, which targets generally lower investment and flattens

production growth. In today’s RBN blog, we’ll take a detailed look at

the 2026 forecasts by peer group and offer some far-too-early

speculation about the potential industry response to the recent surge in

oil prices.

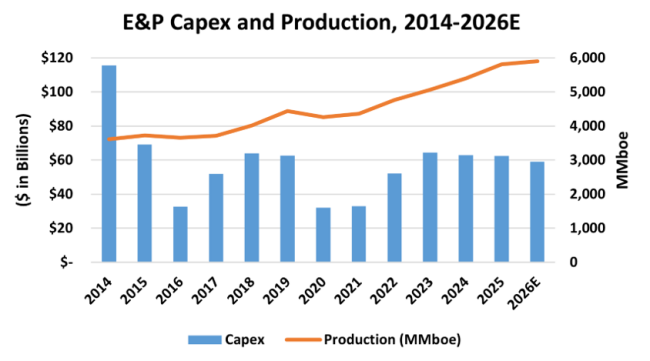

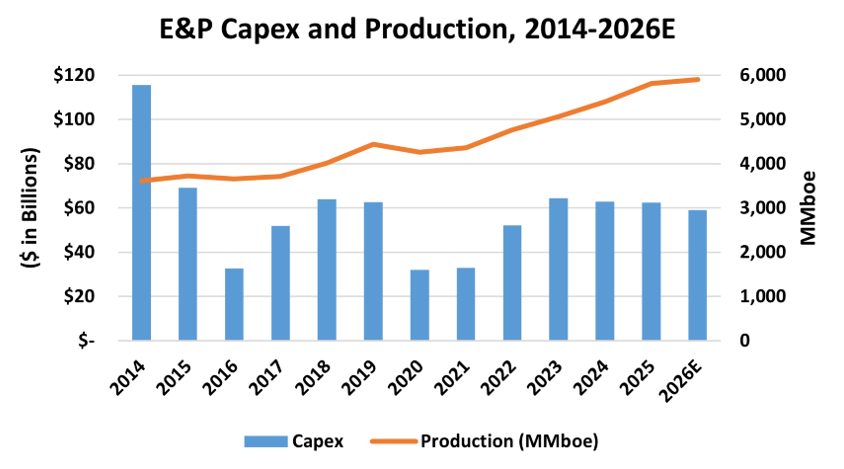

As shown in Figure 1 below, the 36

companies we follow have set 2026 capital investment of $59.1 billion

(far-right blue bar and left axis), down 5% from $62.5 billion in 2025

and continuing a moderation from the recent peak in 2023. The commodity

price collapse at the onset of the pandemic threatened the financial

stability of a chronically overspending E&P industry that had lost

the investment community's confidence. The response was drastic cuts to

capital spending in 2020 and 2021, as producers strategically shifted

their investment focus to maximizing shareholder returns over reserve

and production growth (see Where Has All The Capex Gone?).

Sustained high commodity prices allowed producers to increase drilling

to offset steep shale decline rates, leading to substantial quarterly

increases in investment and a total 2022 capex of $52.1 billion, up 58%

over 2021 and the largest growth rate in over a decade. Inflation as

well as increased organic capital outlays related to acquisition

activity led to another 24% increase in 2023 investment to $64.5

billion, similar to amounts spent in pre-pandemic 2018. The restored

investment over two years resulted in a 14% production gain.

Figure 1. E&P Capex and Production, 2014-2026E. Source: Oil & Gas Financial Analytics LLC