RBN Energy: More Permian gas takeaway is coming. What about strong Waha prices? Link here. Archived.

Permian

wells are churning out 22 Bcf/d of residue natural gas — one-fifth of

total U.S. production — but for many producers that gas abundance is a

hindrance. A persistent shortfall in pipeline takeaway capacity has made

negative (sometimes very negative) prompt-month and cash prices at the

all-important Waha Hub an all-too-regular thing. But there’s good reason

to believe the situation will soon be changing for the much-better. A

massive tranche of new takeaway capacity will be coming online over the

next few months, ending the shortfall for at least a few years, and gas

demand from LNG exporters and power generators will be ramping up fast.

In today’s RBN blog, we begin an in-depth examination of Permian

takeaway capacity, Waha prices, and the potentially far-reaching impact

of solidly positive gas prices on producers’ development strategies.

The

Permian’s expansion into the world’s largest, most productive crude oil

play over the past 15 years came with a market-changing side effect: an

equally impressive expansion in the production of associated gas

(natural gas + NGLs). Producers’ primary focus was (and still is) on

crude — to quote bank robber Willie Sutton, “That’s where the money is” —

and their #1 priority has been supporting the development of the

pipelines, storage and other infrastructure needed to produce it and get

it to market. At the same time, however, they and their midstream

partners had no choice but to deal with the vast and fast-increasing

volumes of associated gas emerging from Permian wells with high-value

oil.

Massive sums have been invested in building out

gas gathering systems, processing plants and takeaway pipelines, not

just for natural gas but for NGLs. But it’s almost always been a game of

catch-up. Producers didn’t want to make long-term pipeline-capacity

commitments, and that reluctance ultimately crushed the spread that

justified the pipeline to begin with. That led to a game of chicken,

where ultimately the biggest producers had no choice but to pony up to

get the pipelines built and smaller producers suffered when their

interruptible gas was sold at negative prices. (We coined it “the midstream conundrum.”)

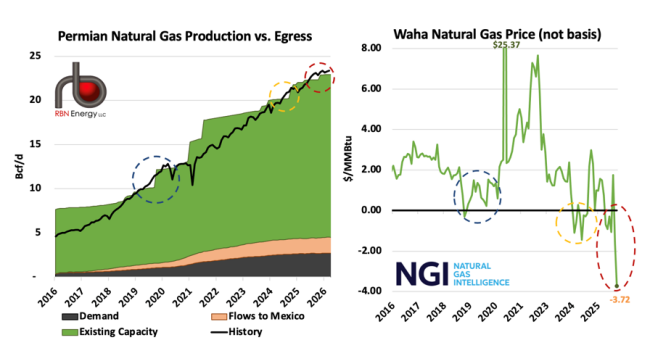

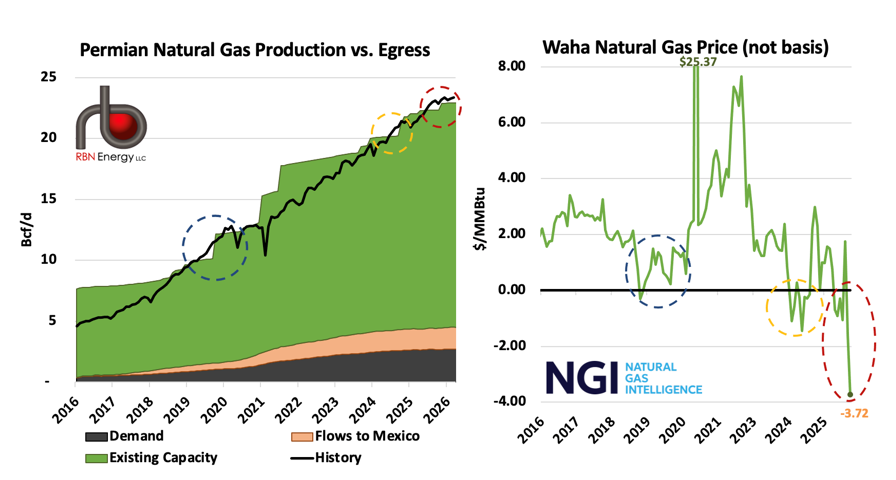

Constraints

in Permian gas takeaway, often exacerbated by pipeline maintenance that

temporarily took some capacity offline, had consequences, primarily in

the prompt-month and cash prices that shippers without sufficient

pipeline space were offered for their gas at the Waha Hub in West

Texas’s Pecos County. The left graph in Figure 1 below shows natural gas

production in the Permian (black line), gas consumption within the

basin (“Demand”; dark-brown layer), flows to Mexico (beige layer),

pipeline capacity out of the region (green layer), and periods when

takeaway constraints frequently caused Waha prices to turn negative

(dashed circles). [Note that most producers are not selling their gas at

Waha prices. A lot of them have capacity on pipelines that can get

their gas to downstream markets.]

Figure 1. Permian Gas Production, Takeaway Capacity and Waha Cash Prices. Sources: RBN, NGI