Locator: 50656NACHO.

Iran: President Trump's most recent tweet suggests a "one-two punch" coming. Watch the pizza deliveries this weekend.

Iran: no one will admit it, but had this been a unified global effort when Israel and the US decided to end Iran's nuclear ambitions two months ago, this conflict would have ended long ago. Probably in the first month, maybe sooner.

Hezbollah: Israel continues to attrit the Hezbollah leadership in Lebanon.

Total Energies: link here. The WSJ. Increases dividend 6%. Will resume share repurchases. Earnings windfall. I love that word. Windfall. As long as it's not followed by "profits tax." Big gain: not in the actual commodity but in trading. Simply working smarter, not harder. New profit doubled q/q: $5.81 billion and that beat the $5.21 estimate. Don't often see that in stodgy oil companies.

Facilities representing around 15% of TotalEnergies’ total oil and gas production are shut down due to the conflict in the Middle East. It has halted production in Qatar, Iraq and offshore the United Arab Emirates as energy infrastructure in the region has come under attack.

*******************************

Back to the Bakken

WTI: $103.30; up 3.37%; up $3.37.

Later: WTI up almost $4.00. No one seems worried. Business page headlines hardly mention it. The Fed gets the most attention. Wow.

Later; ahhhh .... there it is -- over $4.00 -- 8:55 a.m. ET -- April 29, 2026 --

New wells reporting:

- Thursday, April 30, 2026: 100 for the month, 100 for the quarter, 257 for the year,

- None.

- Wednesday, April 29, 2026: 100 for the month, 100 for the quarter, 257 for the year,

- 42080, conf, XTO, GBU Hera 33X-7F,

- 42079, conf, XTO, GBU Hera 33X-7A,

- 41734, conf, Hess, EN-Hilleren-157-94-1336H-2,

- 41614, conf, BR, Sivertson 6I,

- 41360, conf, Devon Energy, Marvin 27-34 3H,

RBN Energy: with speed to market the #1 priority, data center developers put the pedal tot he metal. Link here. Archived.

Nearly every energy-related discussion these days, regardless of the particular topic, eventually turns to data centers and AI, where speed to market has emerged as the major focus. As one panelist noted during March’s CERAWeek energy conference in Houston, of a data center developer’s top priorities, the first three are now speed, speed and speed, with cost and other factors coming next. In today’s RBN blog, we look at how developers must solve the issues around permitting, siting, offtake agreements and — most importantly — power generation in the race to get their data centers online as soon as possible. We’ll also preview our newest Drill Down Report on the data center buildout.

The substantial growth in data center capacity has been driven largely by the increasing demand for AI and what are generally classified as AI-powered tasks, such as speech recognition, image recognition, predictive analytics, personalized diagnostics/treatments, logistics/mapping applications, fraud detection and generative AI (see Smarter Than You). The rapid rise in generative AI is particularly noteworthy, catalyzed by the sudden success of ChatGPT and a few other AI chatbots riding that wave, including Claude, Copilot and Perplexity. The revolutionary potential of AI is hard to overstate and, correspondingly, so too is the potential money to be made. That has kicked off an all-out, no-holds-barred race to win market share. With so much competition in the market and the speed at which the machinery is advancing, developers have come to believe that getting their data center capacity online as quickly as possible is essential.

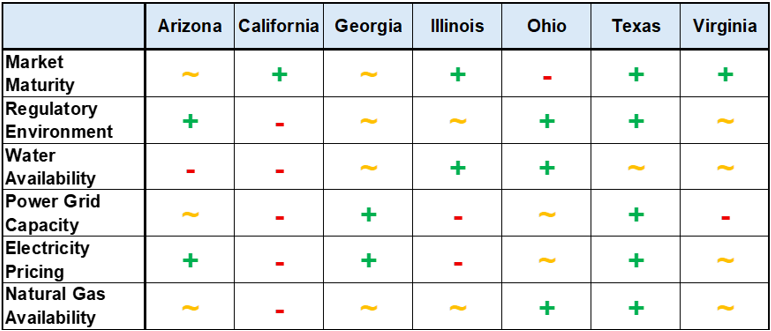

The first set of challenges around a data center’s development is fairly straightforward, if not always easy to navigate. Being able to secure the needed amount of electricity to power a site is the dominant issue (much more on that below) but there are many other factors to consider, including obtaining the available land, the ability to connect to fiber-optic networks, assessing weather and climate risks, local transportation and workforce issues, and access to water for cooling. Our new report breaks down the leading seven hubs for data center development — Arizona, California, Georgia, Illinois, Ohio, Texas and Virginia — and compares their relative strengths and weaknesses in several categories (see Figure 1 below), including market maturity, the regulatory environment and power grid capacity. (The report also does the same for four states that are emerging as hubs — Indiana, North Carolina, Ohio and Pennsylvania.)

Figure 1. Relative Strengths and Weaknesses of Key Data Center States. Source: RBN