Locator: 48576B.

RBN Energy: Sentinel's Texas GulfLink makes big strides forward in export terminal race. Archived.

In the race to build the next deepwater crude oil export terminal in the Gulf of Mexico, Sentinel Midstream’s proposed Texas GulfLink (TGL) has become one of the frontrunners. TGL’s plan gained its crucial Record of Decision (ROD) Approval from the U.S. Department of Transportation’s Maritime Administration (MARAD) on February 14, but there is still some distance to go before a final investment decision (FID) is reached. In today’s RBN blog we’ll discuss Sentinel’s TGL plan, why it might be uniquely positioned to move forward, and the other contenders still in play.

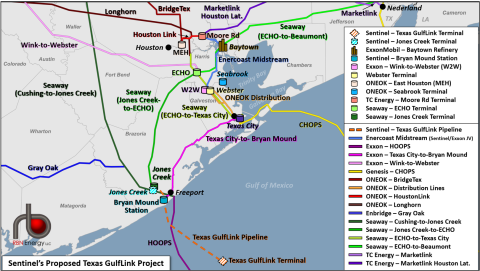

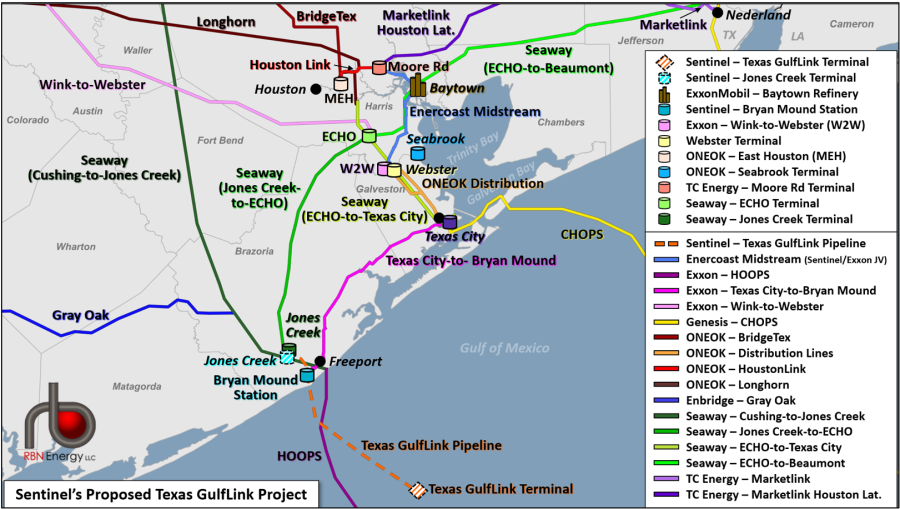

Let’s start with a refresher on the TGL project and efforts to build a deepwater export terminal in the Gulf of Mexico*. TGL, which at one point was considered a Dark Horse in the multi-year competition, would feature a deepwater platform (orange-and-white striped square in Figure 1 below) able to load a tanker at a rate of 85 Mb/hour, 2 MMb/d, which would allow it to fully load a Very Large Crude Carrier (VLCC) in one day. The platform, located nearly 30 miles offshore Freeport, TX, would be connected via the 42-inch-diameter Texas GulfLink Pipeline (dashed orange line) to an onshore storage terminal at Jones Creek (aqua-and-white-striped tank icon west of Freeport) in Brazoria County. At the onshore facility, about 9 MMbbl of above-ground tanks would be supplied from the Houston area, including the Webster Terminal (pastel-yellow tank icon), giving the project access to significant volumes of Permian originated crude oil, in addition to other grades feeding that market.

[*Yes, we know that Gulf of Mexico has been renamed Gulf of America by the Trump administration. For now, we are going to stick with Gulf of Mexico not out of protest or spite, but because that is what it is still called by the majority of the energy market.]

Figure 1. Sentinel’s Proposed Texas GulfLink Project and Other Nearby Infrastructure. Source: RBN

We’ve written a great deal in the RBN blogosphere about the fierce, multi-year competition to build a deepwater terminal (see Gulf Coast Time). U.S. crude export volumes took off in the 2010s and were expected to continue growing along with production throughout the 2020s, driving the market to seek the most efficient export options. Prior to 2018, numerous terminals were proposed along the Gulf Coast including a number of offshore single-point mooring (SPM) facilities that would be able to fully load a VLCC without reverse lightering. However, in the downturn of 2020, some of those projects were scrapped, leaving four developmental projects and the one in-service offshore facility in Louisiana.

******************************

Sentinel Midstream GulfLink

From earlier on the blog:

RBN Energy's top ten prognostications for 2025, link here:

6. No offshore SPM crude oil terminal will be sanctioned in 2025.

We really hope to be proved wrong on this one, but it just looks like this is a case where the benefits do not justify the cost. Since 2018, numerous offshore single-point mooring (SPM) terminals have been proposed along the Gulf Coast to fully load a Very Large Crude Carrier (VLCC) without reverse lightering.

Currently, only the Louisiana Offshore Oil Port (LOOP) can handle VLCCs but it is limited to two ships per month on average, far below the one per day a couple of the SPMs could manage.

The remaining projects — Energy Transfer’s Blue Marlin, Sentinel Midstream’s Texas GulfLink, Phillips 66’s Bluewater Texas, and Enterprise’s Sea Port Oil Terminal (SPOT) — have faced regulatory hurdles but made progress, with SPOT receiving its U.S. Maritime Administration (MARAD) license in April.

Yet none have reached a final investment decision (FID) after nearly seven years of development. The problem is shifting market dynamics. Initially, U.S. crude exports to Asia (15,000 nautical miles from the Gulf Coast) justified VLCC efficiencies, but Europe now takes 45% of exports compared to 40% to Asia, driven by demand shifts due to the Ukraine war and declining North Sea production. The shorter 5,000-nautical-mile trip to Europe diminishes the economic advantage of VLCCs, making shippers hesitant to commit to long-term capacity deals for the SPM terminals. Granted there are still good reasons for one or more of the SPMs to be sanctioned. But it is more difficult today to get shippers signed up than it originally looked, and that’s a situation that will likely get worse before it gets better.

Also from April 25, 2024, also on the blog:

RBN Energy: Sentinel Midstream's Texas GulfLink emerges as serious contender in export terminal race. Archived.

In the race to build the next deepwater crude oil export terminal in the Gulf of Mexico, Sentinel Midstream’s proposed Texas GulfLink (TGL) is currently in second place in the regulatory race, behind only Enterprise’s Sea Port Oil Terminal (SPOT) — and seems to be emerging as a serious contender. The plan offers some compelling attributes, including Sentinel’s status as an independent midstream player and plenty of pipeline access to crude oil volumes in the Permian and elsewhere. In today’s RBN blog, we turn our attention to TGL and what it brings to the table.

From AI: