Locator: 50655ARCHIVES.

Locator: 50654EPICFURY.

Wow, wow, wow.

The following was posted at 8:12 a.m. early this morning. Link here.

Everything suggested to me that Trump had decided the best course of action was an extended blockade. We'll come back to that later -- the point for now is that at 8:00 a.m. this morning I suggested that Trump was in this for the long haul -- an extended blockade.

Now, this evening, The WSJ is reporting exactly that. Link here. This is the lead story in the print edition.

It will be fascinating to watch this play out. I think there's more to the story that has not been told. Absolutely brilliant.

This is not just about Iran.

This is key:

Every day the strait is closed, the more irrelevant Qatar (natural gas) and Saudi Arabia (oil) become.

MAGA.

Monroe Doctrine.

Western Hemisphere.

*****************************

Movie Night

Dial M for Murder. TCM tonight.

I bet I've seen this film a dozen times. One of the absolute best movies ever. Pure entertainment.

On a different level than Casablanca, The Third Man, Citizen Kane but in its genre, Dial M For Murder might be the best!

I can watch it every few months. Wow.

I simply love this movie.

In addition to everything else, Hitchcock's filmography is absolutely superb. And so Hitchcockian.

Locator: 50653B.

Three pipelines to buy in April, link here:

GM earnings:

Windmills Of Your Mind: link here.

Talk about a gorgeous day -- poolside.

Yesterday we went swimming for the first time this season, but today the water is a bit too cold to get into. But still, it's 87° on the deck. Overcast. Tornado warnings for next six hours or so. It was supposed to thunderstorm, but it didn't.

What amazes me and should amaze everyone: it's not the fact that there is water on this earth but that there is so much water! That's what is amazing; not that there is water on the earth but that there's so much water on the earth.

Later, at 7:00 p.m. CT, after the storm that wasn't, I returned to the deck. I think the thermometer said 79° but can't remember for sure. Regardless, it is/was a beautiful night.

Poolside reading:

OpenAI to partner with AWS? Link here.

*****************************

Back to the Bakken

WTI: $99.93. Dropped back from $100.50 earlier in the day.

Active rigs: 23.

Five new permits, #42875 - #42879, inclusive:

Five permits renewed:

Nine producing wells (DUCs) reported as completed:

Locator: 50652IRAN.

Conflicting Opinions

April 29, 2026: all of a sudden, after the story below was published, a gazillion outlets said, "hey, not so fast." This is not big deal. Link here.

This will be fascinating to watch. One drone hit on one Qatar facility, and the country pretty much shuts down LNG exports, and Iran was hit for a month by US military, and now a blockade, and a gazillion media outlets said Iran will do just fine. Okay.

The interesting thing, until Trump got into the sanctions business, the UN and the EU thrived on sanctions as the go-to policy to change behavior. I guess now that Trump is doing it, the UN and the EU are arguing it won't work. LOL. Hey, that reminds me, take a look at this link: https://x.com/BjornLomborg/status/2049446147282846069.

Original Post

Sent to me by a reader. Thank you so much. This is amazing. It explains "everything." Well, maybe not everything, but certainly a lot. This starts to provide a timeline.

Trump, unfortunately uses so much hyperbole, we never know what's really going on. But even his hyperbole can point us in the right direction.

Some data points:

Trump says he received a memo from Iran overnight suggesting their country is in collapse. One would doubt Iran leaders would say that but perhaps based on what they said, Trump was able to read between the lines and surmise that, yes, the Iranians were admitting their country was "in collapse."

Take all those data points and then connect them with the story that a reader sent me earlier today. It all starts to make sense. The dots connect.

Again, the link. Archived here.

Locator: 50651INVESTING.

See blog's disclaimer: link here.

SBUX: earnings out today. Huge. Shares up 7%; shares up $7. Trading at $104.

VISA: earning out today. Nice numbers. Shares up 2%; shares up almost $7. Trading at $315.

STX (Seagate): after earnings -- shares up 10%; shares up almost $60. Trading at $635. But the big story is margin: 47%.

AAPL: link here. Reports later this week.

Hope springs eternal. It's all about the guidance. OpenAI's guidance.

Locator: 50650IRAN.

Updates

Later, 8:06 p.m. CT, poolside: link here. While the Middle East rebuilds, a new energy bloc rises under US direction. Simon Watkins.

Original Post

Every day the strait is closed, the more irrelevant Qatar (natural gas) and Saudi Arabia (oil) become.

There's a bigger story here. This is simply a single piece of a much larger mosaic.

More proof, link here, Venezuela:

Libya, link here: CVX inks agreement with Libya.

Germany, link here: in talks with Poland.

Locator: 50649B.

See blog's disclaimer: link here.

WTI: absolutely, positively, the only thing I'm interested in today with regard to the Mideast is whether WTI can hold above $100 at the close. Anything below $96 is a debacle on so many levels; and, I'm not even thinking about my portfolio.

OPEC in disarray: UAE to leave OPEC "immediately"; to increase production; UAE sits at exit to Strait of Hormuz, opposite Iran.

News story, hardly: Trump won't consider Iran's latest proposal. DOA.

In fact, there's really nothing to negotiate, is there? There's a ceasefire in place, so no need to discuss a ceasefire. We all know what is necessary with regard to the strait. Iran does two things: a) says it won't enrich uranium (Iran doesn't have to mean it; just say it); and, b) escort vessels through the strait to avoid mines. Fairly simple.

Right now, we have a Korean truce with the strait a "no-man's land." Water in this case. And every day the strait remains closed, the more irrelevant the Mideast becomes.

The US and Iran are not negotiating Hezbollah; that's an issue for Israel and Iran, not the US.

Markets diverge:

Trump: all indications he's in this -- Operation EPIC FURY -- for the long haul. Internal polling: majority of Americans want to see the job done. Curious how long Iran can hold out, losing $500 million / day.

What's driving tech today: one word -- FEAR

************************************

Back to the Bakken

WTI: $99.57 - drops back a bit after hitting $100.50.

New wells reporting:

RBN Energy: rising southeast gas demand spurs pipeline projects, competition with LNG exports. Link here. Archived.

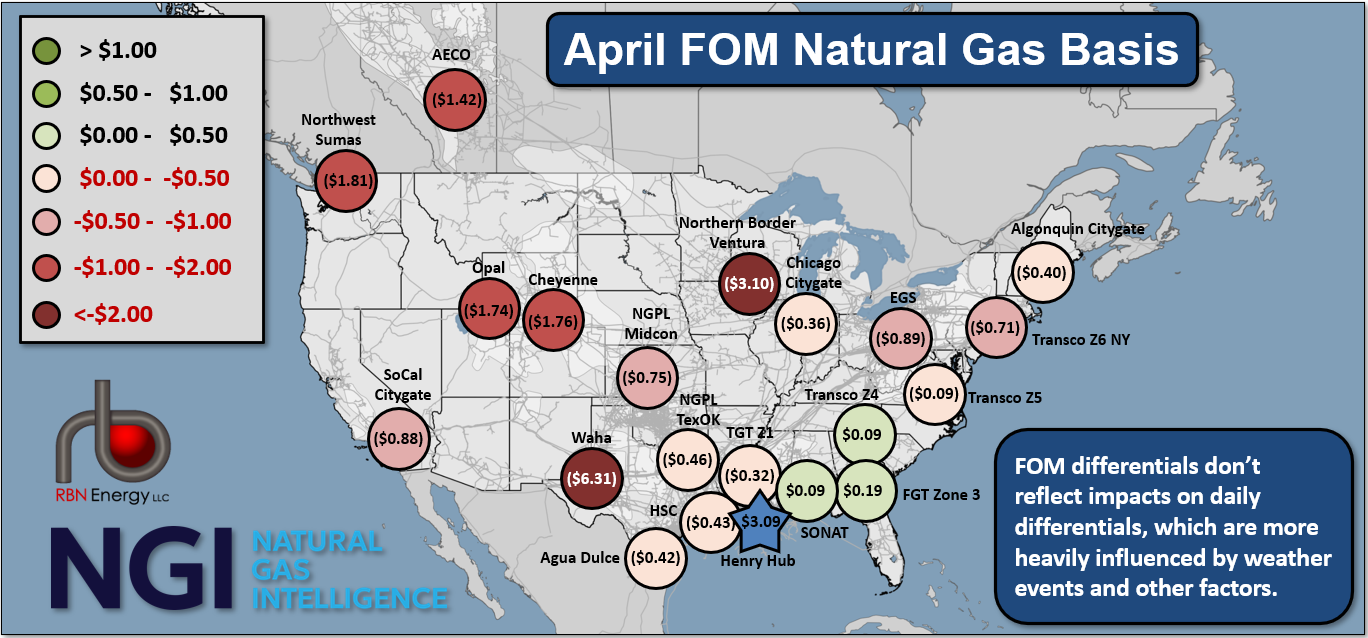

We’ve blogged about rising demand for natural gas in the southeastern U.S. and several of the pipeline projects being planned to deliver more gas to that fast-growing region. But there’s more to the story — a bigger picture — namely, that gas consumers in Florida and other states pulling gas east through Mississippi increasingly find themselves competing for supply with LNG exporters. In today’s RBN blog, we begin a two-part series on Southeast gas demand, new pipeline capacity to and through the region, and why the gas flowing there is priced higher than Henry Hub.

Ask your favorite chatbot which states are in the southeastern U.S. and you’ll get a long list — generally, everything within the huge triangle formed by the Virginias, Florida and Louisiana. The Southeastern Conference (SEC) of the NCAA includes Oklahoma, Missouri, Kentucky and two universities in Texas (one of which we like!). But for our purposes, we’re zeroing in on the southeasternmost swath: from west to east, Mississippi, Alabama, Florida, Georgia and South Carolina. While these five states account for only 0.4% (~ 400 MMcf/d) of total U.S. natural gas production, their share of U.S. gas consumption is 30X higher — about 12% or 11 Bcf/d — mostly due to their heavy (and growing) reliance on gas-fired power generation and (especially in Alabama, Georgia and Mississippi) a lot of industrial demand too.

Gas-demand growth in the region has been coming on fast and furious over the past few years, stressing the legacy gas pipeline networks there and resulting in the SONAT (Southern Natural), Florida Zone 3 and Transco Zone 4 price trading points — primary indicators of gas prices in our five-state focus area — being among the very few points where gas is priced at a premium to Henry Hub. [Figure 1 below shows April first-of-month (FOM) differentials — the green-shaded circles indicate trading points where the FOM differential is a premium to Henry.]

Figure 1. April FOM Natural Gas Basis. Source: NGI

Locator: 50648DOCKETS.

Hearing dockets are found here at the NDIC.

Wednesday, May 27, 2026

Link here.

18 pages.

The cases, again, these are cases, not permits:

Thursday, May 28, 2026

Link here.

18 pages.

The cases, again, these are cases, not permits: